Personal Wealth Management / Market Analysis

A Mid-September Economic Roundup

As we enter autumn, here is an end-of-summer economic data roundup.

As the latest surveys revealed, folks are feeling dour stateside and overseas. The bleakness is understandable given this year’s myriad negative stories. Yet many forecast worse times ahead as the global economy contends with high prices and the prospect of recession. That is possible. But a roundup of the latest data out of the world’s largest economies continue showing a mixed picture—worth keeping in mind when comparing reality to such dark expectations and sentiment.

Reviewing the Latest Out of China

China released several widely watched data series for August last Friday, and they beat expectations. Industrial production rose 4.2% y/y, ahead of expectations of 3.9%, while retail sales were up 5.4%, 2 percentage points better than consensus estimates.[i] Fixed asset investment’s 5.8% growth on a year to date, year-over-year basis was also a few ticks higher than expectations of 5.5%.[ii]

Now, August’s stronger-than-projected figures may not imply broad-based strength, as reality is more nuanced. For example, retail sales’ growth, the quickest in six months, was partially tied to the base effect—the Delta COVID wave weighed on August 2021 economic activity, depressing the denominator for the year-over-year comparison this year. China’s heatwave led to a spike in electricity production, which boosted industrial production. The auto industry boosted both measures, too: Subsidies for electric vehicles buoyed car sales, and heightened demand led to a surge in output of new electric vehicles. As for fixed-asset investment, some analysts credited the pickup to government stimulus efforts (e.g., extending credit to infrastructure spending) bearing some fruit.

Interestingly, most coverage we read highlighted these sensible caveats to the data—yet also argued headwinds tied to the government’s zero-COVID policy and ongoing property weakness implied the economy was weaker than appreciated. In our view, this is yet another example of the pessimism of disbelief at work. To be clear, we aren’t dismissing China’s weak spots. Zero-COVID policy in particular weighs on both domestic and external demand. Growth will probably be slower than in past years regardless of the government’s actions.

But slow growth is just fine for stocks. While many presume fast Chinese growth is a needed engine for the world—a throwback to sentiment after the financial crisis—we think this is both overstated and unrealistic. China is the world’s second-largest economy, which means it is expanding from a huge base. Expecting it to grow at high-single or even double-digit rates into perpetuity is asking a lot. Besides, even at slower growth rates, China is still adding a lot to global economic activity that is already better than so many appreciate.

US Industry Is a Mixed Bag

Along with retail sales—which we already covered—US industrial production (IP) hit newswires last week. August’s reading dipped -0.2% m/m, as a weather-related slump weighed on the Utilities industry (-2.3% m/m), though some anticipate a big September rebound tied to the West Coast’s recent hot spell. Positively, manufacturing—the largest industry group and representative of about 12% of US GDP—ticked up 0.1%, its second-straight positive month. Another notable development: Oil & gas drilling rose 2.7%, its 11th straight monthly rise and a sign, in our view, of market forces at work. Consider: High energy costs, including gasoline and natural gas (tied to strong air conditioning demand), have dominated headlines and weighed on moods this year. Yet ongoing production in the oil & gas industry suggests producers are responding to price signals and bringing on supply to meet demand—which argues against perpetually rising prices.

Overall, August IP was a mixed bag, as production rose in machinery, aerospace equipment, and computers and electronics but fell in autos and consumer goods. The picture was similarly muddled at a regional level. The New York Fed’s Empire State purchasing managers’ index registered a -1.5 reading in September—contractionary, but a big improvement from August’s -31.3—as respondents reported higher new orders and a deceleration in price increases. However, the Philadelphia Fed’s regional manufacturing survey worsened from 6.2 in August to -9.9 in September, its third negative reading in the past four months. Respondents here also reported decelerating prices, though new orders worsened. September’s reading also reverses August’s pattern, showing no clear trend. While the lack of clarity can be frustrating, these manufacturing readings are a microcosm of the mixed economic data in both the US and abroad recently.

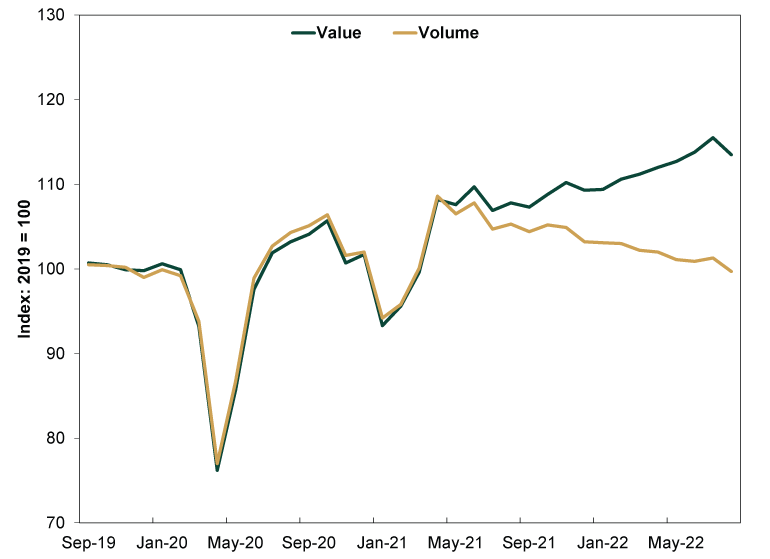

On the UK’s (Unsurprisingly) Poor Retail Sales Report

UK August retail sales fell -1.6% m/m, continuing a downward trend since last summer, as all major sectors contracted.[iii] Moreover, this is on a volume—inflation-adjusted—basis, so the contraction suggests high prices are weighing on consumer spending to an extent. Households are saying as much, too. Per an ONS survey conducted from August 31 – September 11, about 87% of adults reported a higher cost of living over the past month, a jump from 62% in November 2021 (when the survey question was first asked). Unsurprisingly, about half of respondents noted difficulty in paying their energy bills.

This isn’t good, of course, as more households face hardships due to rising prices. But for stocks, this trend isn’t new, as retail sales values and volumes have been diverging since early 2021. (Exhibit 1)

Exhibit 1: Divergence in UK Retail Sales’ Values and Volumes

Source: Office for National Statistics, as of 9/19/2022.

While we don’t dismiss the negative impact on retail businesses, stocks don’t need strong growth to climb. Markets don’t view news in the traditional “good” or “bad” sense as most people understand it. Rather, they are callous—and ruthlessly efficient—discounters of widely known information, focused most on the economic and political factors that impact corporate profits over the next 3 – 30 months. In our view, stocks have long priced in and moved on from past UK retail weakness—and they are looking ahead.

Moreover, considering how low expectations are in the UK—see myriad recession forecasts—weak-but-still-positive data have the ability to surprise to the upside. Another potential sentiment fillip: Chancellor Kwasi Kwarteng is planning to announce a small relief package this week. Mind you, we don’t think government spending is necessary or even all that effective in boosting a private-sector dominant economy. But the news could help investors feel like the issue has been addressed, allowing them to start moving on.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

-

Expert Commentary This Week in Review | Energy Markets, Fed Meeting, Earnings Reporting

2026-03-20

2026-03-20 -

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today