Personal Wealth Management / Economics

A Peek at Allegedly ‘Peaking’ Eurozone Growth

Wobbles in monthly data often don’t mean much.

Among the many things preoccupying investors during the latest spate of volatility were three little letters: P, M and I. Last week, flash Purchasing Managers’ Indexes—better known as PMIs—for the eurozone hit their lowest level in 15 months, sparking fears of a fizzling expansion. A couple days later, fresh ECB data showed loan growth easing a tad in February. Combine the two, and you get fears growth is “peaking.” But the eurozone’s 19-quarters-and-running economic expansion doesn’t appear to be in danger, in our view, and one or two months’ slowdown doesn’t automatically imply further slow growth ahead. Monthly wobbles are normal, especially when you consider that a freak Siberian storm known as the “Beast from the East” likely played a role. On the bright side, resurgent skepticism creates plenty of room for positive surprise—bullish for eurozone stocks.

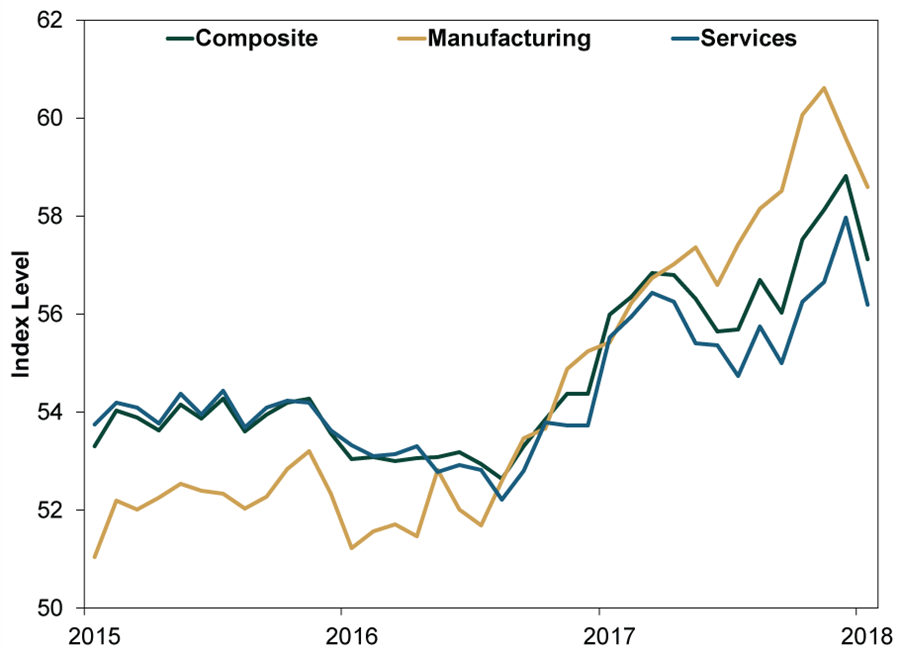

From the tenor of last week’s coverage, you would be forgiven for thinking the PMI readings signaled an actual downturn. As it happens, they didn’t—rather, they just pointed to perhaps slower growth. March’s composite flash PMI—which include about 85% to 90% of the final survey’s respondents—declined for the second straight month to 55.3 from February’s 57.1 and January’s seven-year high of 58.8.[i] (Exhibit 1) But readings over 50 generally signal expansion. Moreover, PMIs loosely measure what percentage of firms grew—not by how much. They are also surveys, so they aren’t ironclad, and trying to read into wobbles is often fruitless. Hence, PMIs occasionally diverge from actual output measures. Even a contracting PMI, under 50, sometimes doesn’t mean a whole lot. Plus, the latest PMIs are still well above levels seen in 2015 and 2016, when the eurozone was growing just fine, making it difficult for us to see what all the fuss is about.

Exhibit 1: Eurozone PMIs Indicate Expansion

Source: FactSet, as of 3/28/2018. IHS Markit Composite, Manufacturing and Services purchasing managers’ indexes, February 2015 – March 2018.

It is also important to assess why a PMI might have swooned. Growth in new orders eased to its slowest rate in 14 months, but that is still growth—and today’s orders mean tomorrow’s production. Other categories point positively, too. Order backlogs picked up, while delivery times neared their longest read in 18 years. Germany’s supply chain delays are at their most widespread in its 22-year history. While difficulty meeting customer demand isn’t great, we would broadly classify it as a “good problem” to have. Rare is the recession that began against a backdrop of buzzing demand and bustling activity. Firms will likely have to ramp up production to satisfy the orders that have piled up.

The weather backdrop during March underscores this point. The Beast from the East was one of the mightiest, most disruptive winter storms to hit Europe in recent memory. Also dubbed the “Siberian bear” and the “snow cannon,” it brought Arctic temperatures all the way to the Mediterranean, even bringing snowfall to normally tropical islands like Corsica and Capri. The winter beast froze transportation routes across Europe, closing roads, cancelling flights and crimping business in the process. We wouldn’t be shocked to see it impact data in Denmark and the UK as well as the eurozone.

Although we will probably see the Beast from the East impact other data for February and March in the coming weeks, don’t let a backward-looking glimpse at weather’s impact sway your forward-looking assessment. Europe’s economic outlook still appears quite positive. The Conference Board’s February eurozone LEI rose 0.6% m/m—its 18th straight monthly rise. All but two of its eight underlying components positively contributed—the detractors being stocks and residential construction permits. The latter aren’t terribly forward-looking. Stocks are, but they are also volatile, and global stocks happen to be in the middle of a correction. Meanwhile, the yield spread—LEI’s most telling component—steepened, which should support continued loan growth despite widespread fears of a tiny deceleration in February eurozone loan growth. Monthly data are volatile, and one month’s slowdown isn’t so telling.

We think the fundamental disconnect between solid ongoing growth and prevalent skepticism towards it is bullish for eurozone stocks. Many fear slower growth and cite varied reasons for it—including a strong euro hitting exports, ECB tightening, inflation (too low or too high) and a brewing trade war with the US, ignoring that the eurozone economy has already proven it can do just fine with a stronger euro and crawling inflation (e.g., last year). Neither is an inherent economic risk. Meanwhile, ending quantitative easing would likely let the yield curve steepen further, a positive, and President Trump quashed European trade war chatter by exempting the EU from the steel and aluminum tariffs. But these worries, as well as loan growth jitters, signal widespread skepticism, which should create plenty of room for bullish positive surprise.

[i] Source: IHS Markit, as of 3/26/2018.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The Golden Paradox2026-03-24

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today