Personal Wealth Management / Market Analysis

A Surprise From the Land of the Rising Sun?

Reviewing the latest-and what to look out for-from Japan.

Four months into 2017, most eyes are fixated on the West-particularly European elections and the new US administration. However, it's a big world, and it's easy to overlook one of the globe's biggest economies: Japan. The Land of the Rising Sun has struggled economically throughout the broader expansion, and many pundits are growing dour about Japan's economy and stocks-particularly because of allegedly tense trade relations. While we agree Japan's economy likely continues to struggle, sentiment is catching up with this weak reality. Stocks move most on the gap between sentiment and reality, and these lowered expectations increase the risk Japanese data and/or reform efforts positively surprise.

A lackluster economy isn't a new development: see Japan's Lost Decade(s) for more. Since the current global expansion began, Japan suffered recessions in 2011, 2012 and 2014.[i] One-off events like the Great Tohoku Earthquake of 2011 played a role, but weak domestic demand has been the persistent issue. In late 2012, present Prime Minister Shinzo Abe took office and promised to revitalize the economy via his three-part "Abenomics" program: extraordinary monetary easing, fiscal stimulus and economic and structural reform. The first targeted long-running deflation, the second would kick start growth and the third aimed to liberalize the economy in the longer term.

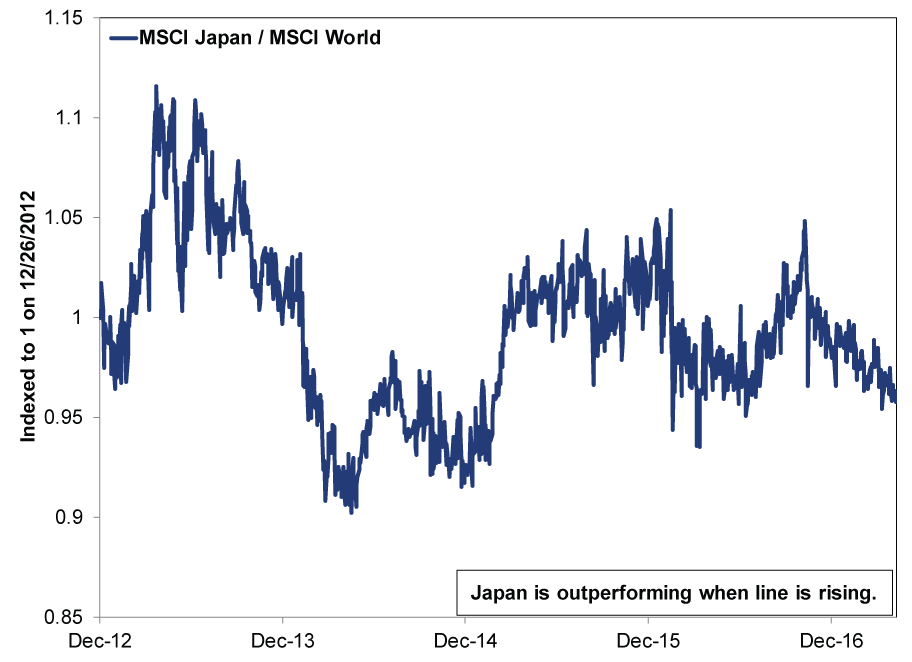

Abenomics' potential excited foreign observers and raised expectations-which also set up disappointment if the program fell short. Hence, Japanese stocks outperformed substantially right after Abe was elected. But this hasn't lasted: Japan has overall underperformed developed world stocks since Abe took office December 26, 2012.

Exhibit 1: Japanese vs. Global Stocks Since Abe Took Office

Source: FactSet, as of 5/5/2017. MSCI Japan and MSCI World, Total Return Index Levels, in USD, from 12/26/2012 - 5/4/2017. Indexed to 1 on 12/26/2012.

Today sentiment is more aligned with reality. While Abe delivered monetary easing and fiscal stimulus, folks now recognize these measures alone haven't spurred growth. The Abe administration passed some reforms (e.g., corporate governance and labor), but they haven't been as deep and impactful as hoped. Despite the hype, reinvigorated domestic demand remains absent, and trade has been the primary growth driver. Thus, given recent talk of protectionist trade policies-specifically from leaders of major trading partners-some observers fear the country's already tepid growth will be snuffed out.

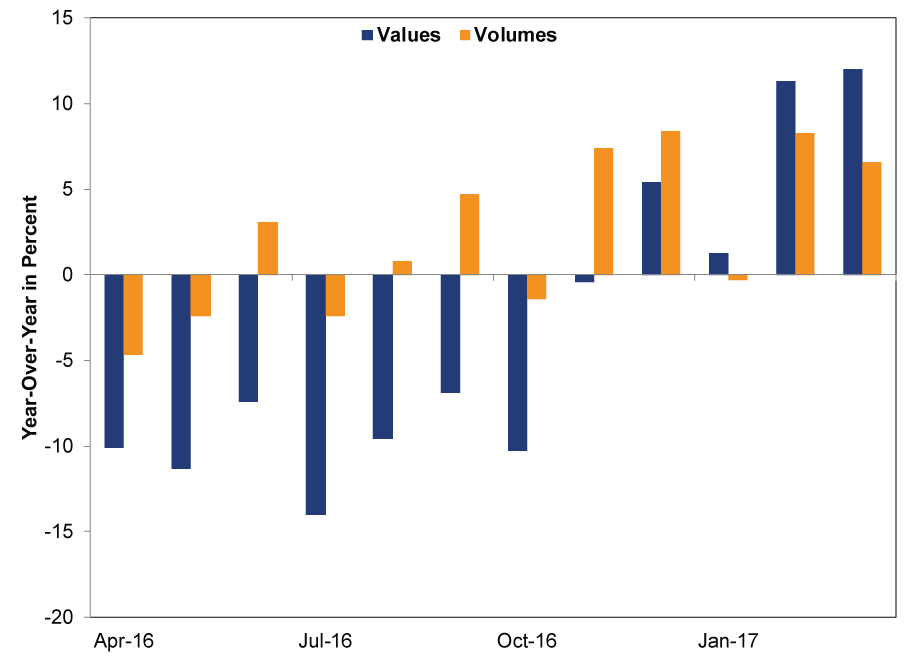

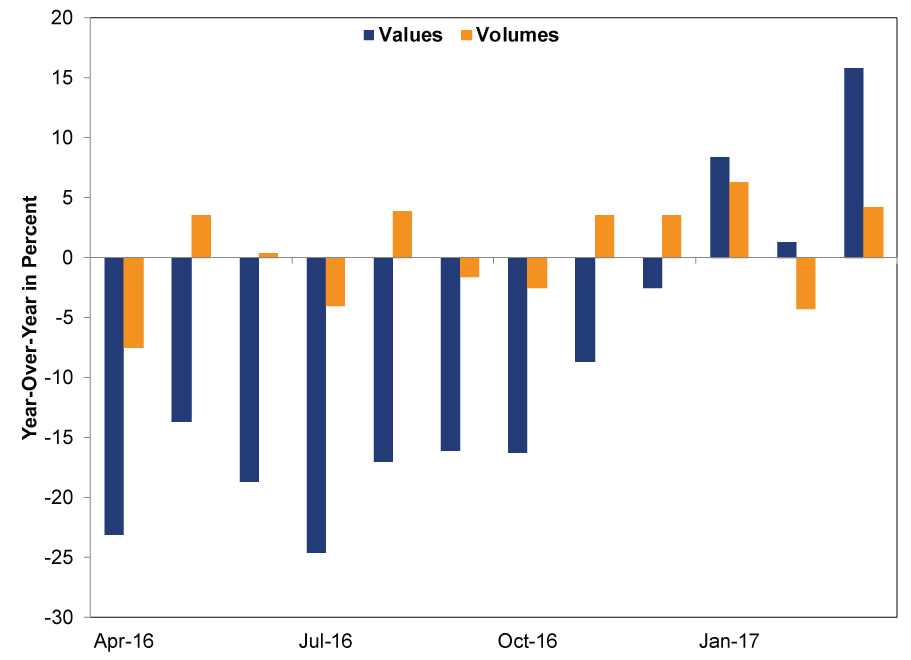

However, the data don't paint that dire a picture. Japan has enjoyed global trade's recent rebound. March export values were up 12.0% y/y while import values rose 15.8%. While this sounds good, values figures aren't all-telling due to currency impact[ii]-trade volumes say more. On this front, March exports (6.6% y/y) and imports (4.2% y/y) have been on an uptrend. (Exhibits 2-3) If the global trade rebound continues and protectionist talk doesn't amount to action, there is the potential for upside surprise here.

Exhibit 2: Export Values and Volumes Since April 2016

Source: Japan Ministry of Finance, as of 5/4/2017.

Exhibit 3: Import Values and Volumes Since April 2016

Source: Japan Ministry of Finance, as of 5/4/2017.

Other data show moderate improvement, too. In April, Japan's services (52.2) and manufacturing (52.7) PMIs were above 50-indicating expansion-for the sixth straight month-a sign more firms are growing than not.[iii] Meanwhile, preliminary March retail sales picked up from February's 0.2% y/y to 2.1%. However, reality still isn't rosy. Consumption is still weak, as consumer spending slipped -1.3% y/y in March-its 13th straight negative reading. Though business investment rose 8.4% annualized in Q4-the strongest reading since Q1 2014-the gauge has vacillated frequently and has yet to show a sustained uptrend. Overall, the largely lackluster[iv] expectations toward Japan seem appropriate. The development to watch is whether the data meaningfully pick up or if expectations fall lower from here-potentially widening the gap between perception and reality.

As for politics, Abe has seemingly eased his effort to revise Article 9-the anti-war clause-of Japan's Constitution. Abe has pursued this lifelong ambition since his tenure's start. However, change requires significant political capital, and Abe's efforts have met stiff resistance, causing him to moderate considerably. Whereas pundits wondered before if he would scrap Article 9 altogether, today Abe is focused on a Special Defense Forces provision-basically keeping everything else. This theoretically frees up political capital to deploy elsewhere, and if Abe does end up using it towards reform-even incremental ones-that could result in a positive surprise.

That said, this status quo isn't overall positive. Japan's long-running issues are likely to keep running: a stagnant economy restrained by entrenched special interests, a byzantine labor code and an overall protectionist trade policy, among other issues. Growth will likely remain tepid, weighed down by weak domestic demand. But stocks move most on the gap between sentiment and reality. With sentiment plunging and global trade picking up, there is an increasing risk of Japan positively surprising with reform and/or economically. If sentiment declines further, this risk becomes more acute.

[i] Source: FactSet, as of 5/4/2017. "Technical recession" defined as two or more consecutive quarterly contractions.

[ii] As an aside, this was one of the rationales behind the BoJ's extraordinary easing policy-to weaken the yen. By doing so, the goal was to help boost exporters, which would ostensibly set off a cycle of growth. While export values did get a boost, it missed the other side of the equation: imports became more expensive. Considering Japan imports most of its fuel, this affected all firms, negating the macroeconomic benefit to exports.

[iii] We don't know the magnitude, but it likely isn't gangbusters.

[iv] Or "meh" if you prefer.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Q2 Market Recap, June US Jobs, Trade Deal Update

2026-07-03

2026-07-03 -

Market Analysis Declaring Fed Independence Fears False2026-07-01

-

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-01

-

Market Analysis Reader Mailbag: June 20262026-06-30

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today