Personal Wealth Management / Market Analysis

Abenomics’ Glowing Tofu Problem

From energy to tofu, Japan’s weakening yen is causing more than a scene these days.

Waves crash against rocks in front of one of Japan’s nuclear reactors. Source: Getty Images.

What do tofu and energy have in common? Ordinarily, not much. But in Japan, they’re the latest indications a weak yen hasn’t yet been a net benefit for the economy—one big reason we’re skeptical of Japanese stocks’ longer-term progress despite the country’s nascent economic recovery.

The weak yen is a byproduct of Japan’s “aggressive monetary easing,” the first arrow of Abenomics (arrows two and three being fiscal stimulus and economic reform). The first arrow had two main objectives: Ending deflation and, via the weaker yen, boosting exports.

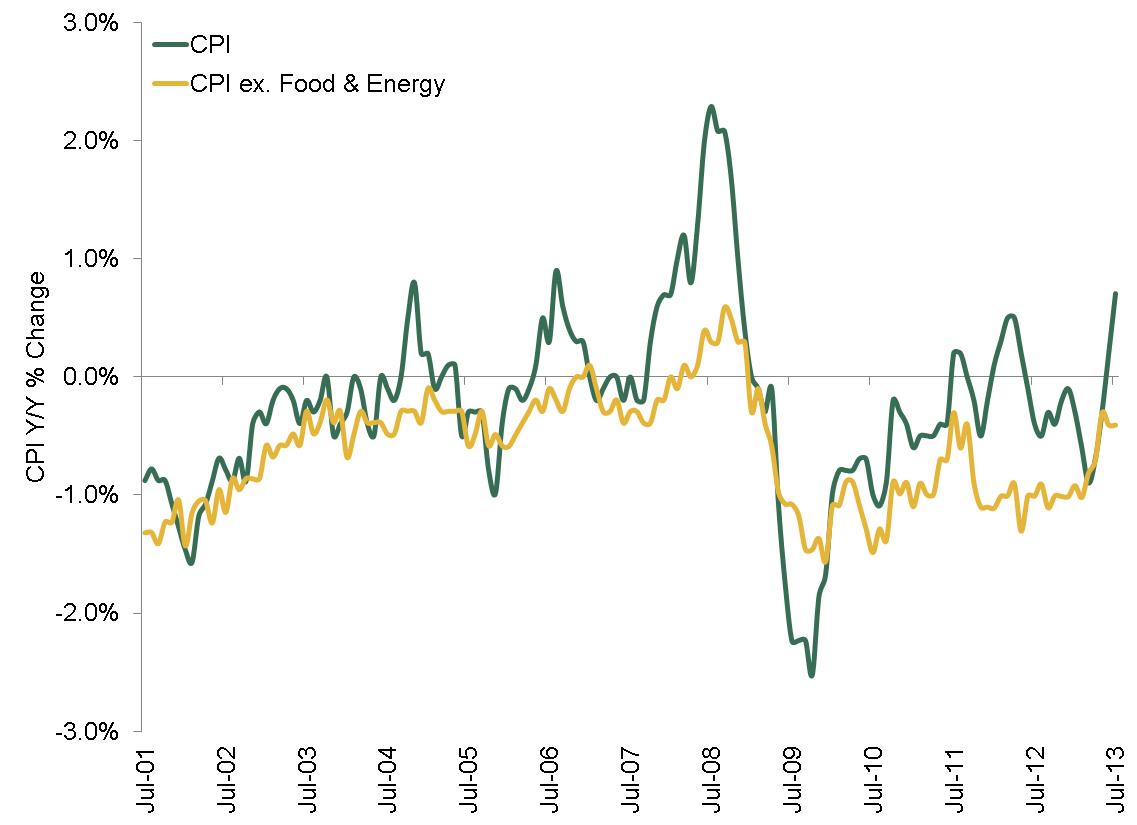

Since then, export values are up, and headline CPI has turned positive. Some officials say this means the policy is working. Yet a deeper look at the data suggests otherwise. Export values may be at three-year highs, but volumes are anemic—July’s 1.8% y/y increase was the first rise in over a year. As for inflation, well, the rising money supply isn’t pushing prices higher broadly. Excluding food and energy, prices are still falling (Exhibit 1).

Exhibit 1: CPI vs. CPI (Excluding Food & Energy)

Source: Thomson Reuters

So what’s the deal with food and energy? In a word, imports. Japan imports a ton: Retailers import finished goods, and manufacturers import raw materials and intermediate components—and as the yen weakens, import prices rise, which weighs on profits. For example, consider Japanese tofu production. Japanese tofu producers import soybeans, which have become pricier as the yen has weakened. Hence, the overall production cost of tofu has risen significantly—and tofu makers plan to hike prices by 20% in order to keep their margins intact.

This is the opposite of what was supposed to happen. The weaker yen was supposed to boost firms’ profits, enabling them to hike wages and invest more. Sure, this is happening anecdotally—otherwise capex wouldn’t have turned positive in Q2. But so far, we aren’t seeing a universally positive impact.

It’s a similar story with energy—another key import post-Fukushima. At its peak, nuclear provided 30% of Japan’s electrical supply with over 50 nuclear reactors. Now there are none—the last remaining plant went offline for maintenance over the weekend, and it isn’t clear when (or if) it will reopen. Power companies have had to import more and more fossil fuels to fill the shortfall. As the yen weakens, already pricy natural gas gets more and more expensive. This further increases businesses’ costs, placing additional pressure on profits. It also whacks household energy bills, likely weighing on spending.

This is also the opposite of what officials want. Rising inflation, in theory, is supposed to goad consumers into spending more—if folks think prices will rise tomorrow, they’ll buy today. But since energy costs are what’s rising, they have to scrimp and save more in other areas—especially without material wage/salary increases.

Hence why a weak yen alone isn’t a panacea for Japan. Without structural reform to address the roadblocks to business investment (e.g., antiquated labor code and the world’s second-highest corporate tax rate), Japanese firms likely won’t achieve the sustainable profit growth necessary for wages and salaries to rise across the board. However, these don’t appear to be in the cards. A nuclear restart would help, too, and Abe has said it is on the agenda. But with public sentiment toward nuclear deteriorating as more fallout from Fukushima comes to light, plans have seemingly cooled. As has most third arrow talk in recent weeks, despite Abe’s earlier pledges to announce another round of reforms in September. Unless this changes and Abe delivers, Japan will have trouble matching investors’ heady long-term economic growth expectations.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Quick Hit: What to Make of Jobs Data’s Persistent Swings2026-04-07

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 30 - April 32026-04-06

-

Expert Commentary US Inflation, Fed Minutes, Consumer Sentiment | 3 Things You Need to Know This Week

2026-04-06

2026-04-06 -

Expert Commentary This Week in Review | Q1 Recap, Earnings Guidance, Elections

2026-04-03

2026-04-03

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today