Personal Wealth Management / Market Analysis

All George Strait’s Exes Live in Texas, but America’s Jobs Don’t

The oil & gas industry is in a rough patch, but job layoffs there aren't a threat to the bull market or US expansion.

For months, headlines have warned falling oil prices will destroy oil industry jobs, threatening overall employment, consumption and growth. Some warn Texas-specifically, Texan oil-is the primary driver of national employment growth, and if those jobs go the rest of America might not make up for them. Yet here we are, after weeks of oil-industry layoffs, and February job growth trounced expectations. While employment lags markets, this is strong evidence America's expansion doesn't rest on the shale boom, and our economic reality is better than most believe.

Oil's impact was evident in February's employment report, but barely. Total nonfarm payrolls rose by 295,000, shattering expectations for 235,000, despite a small drop in oil-related employment. Job losses in oil and gas extraction totaled 1,100, compounding January's drop of 1,800. Oil probably explains most of the 7,400 jobs lost in mining support, too. But growth in construction (+29,000), manufacturing (+8,000) and services (+259,000) offset that by several light years.

Look, we're fans of the shale boom. It has done wonders for household energy bills, businesses' costs and heartland employment. Boomtowns in Texas, North Dakota, Colorado and elsewhere are great testaments to innovation, capitalism and America's economic might. And they are a fantastically compelling story. But shale isn't our whole economy. It is a slice of the mining sector, representing just 1.3% of total US output as of 2013. Before the layoffs began this year, oil and gas was 0.1% of total US payrolls, and total mining was 0.6%. So, you know, really cool! But also kinda small-the real impact came from lower energy prices, a secondary effect (albeit a smashing one).

Depending on how you view jobs data, this might be hard to see. For example, since labor markets began recovering in January 2010, job growth looks like this:

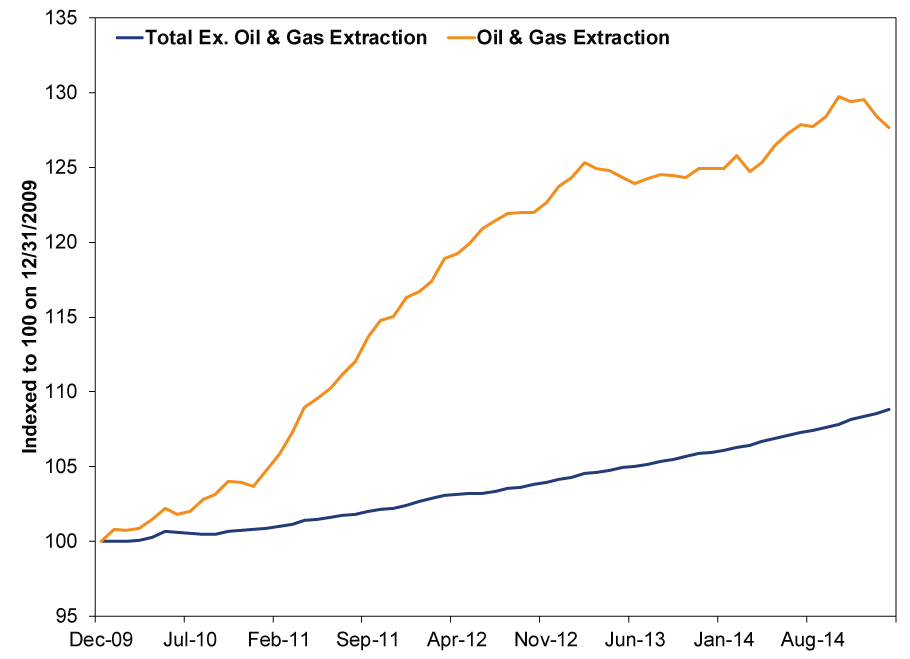

Exhibit 1: Oil & Gas Job Growth Vs. Total Job Growth

Source: Federal Reserve Bank of St. Louis, as of 3/6/2015. Cumulative job growth in oil & gas extraction and total nonfarm ex. oil & gas extraction, 12/31/2009 - 2/28/2015.

That's 8.8% cumulative jobs growth outside oil and gas, and 27.7% for oil and gas alone. One of those numbers is a lot bigger than the other, which would imply, in a vacuum, that the higher number drove growth. But that is sort of a tortured way to view this. Growth rates are handy, but scale matters, too. If you look at total jobs and total jobs excluding oil patch employment, the picture looks like this:

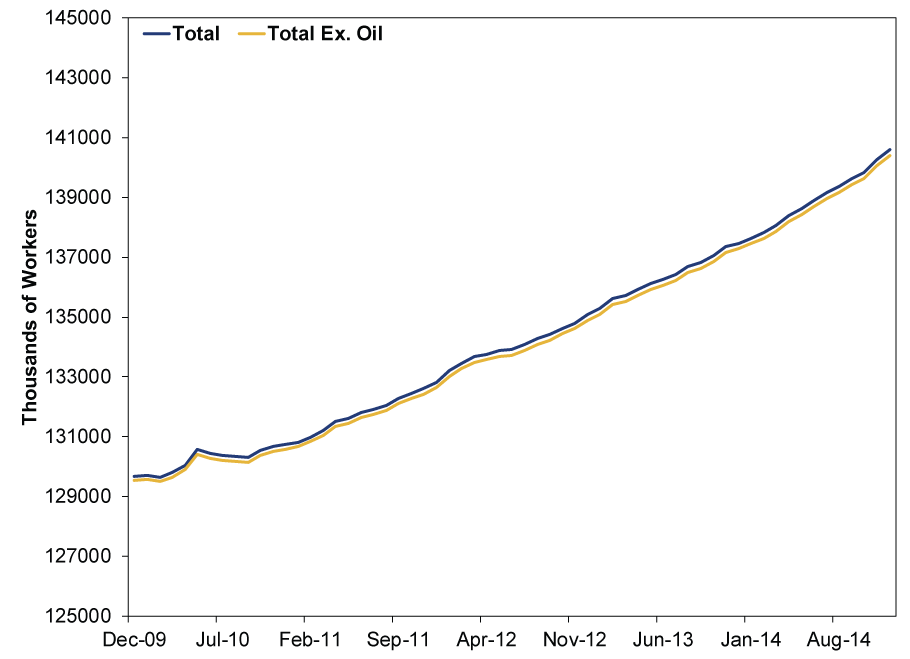

Exhibit 2: Total Payrolls With and Without Oil

Source: Federal Reserve Bank of St. Louis, as of 3/6/2015. Total nonfarm payrolls and total ex. oil & gas extraction, 12/31/2009 - 2/28/2015.

Yes, there are two lines there. One is blue. The other is yellow. They are basically right on top of each other, because there are only about 193,000 oil & gas employees, compared to over 141 million total jobs. Job growth does not depend on the oil patch.

Granted, this doesn't include all the service-sector jobs created in shale boomtowns. Fair point! But you can estimate that impact by comparing national employment with state employment in shale-heavy areas, like Texas and North Dakota. Let's start with Texas.

Exhibit 3: Job Growth in Texas Vs. the Rest of America

Source: Federal Reserve Bank of St. Louis, as of 3/6/2015. Cumulative job growth in Texas and the rest of the country, 12/31/2009 - 12/31/2014.

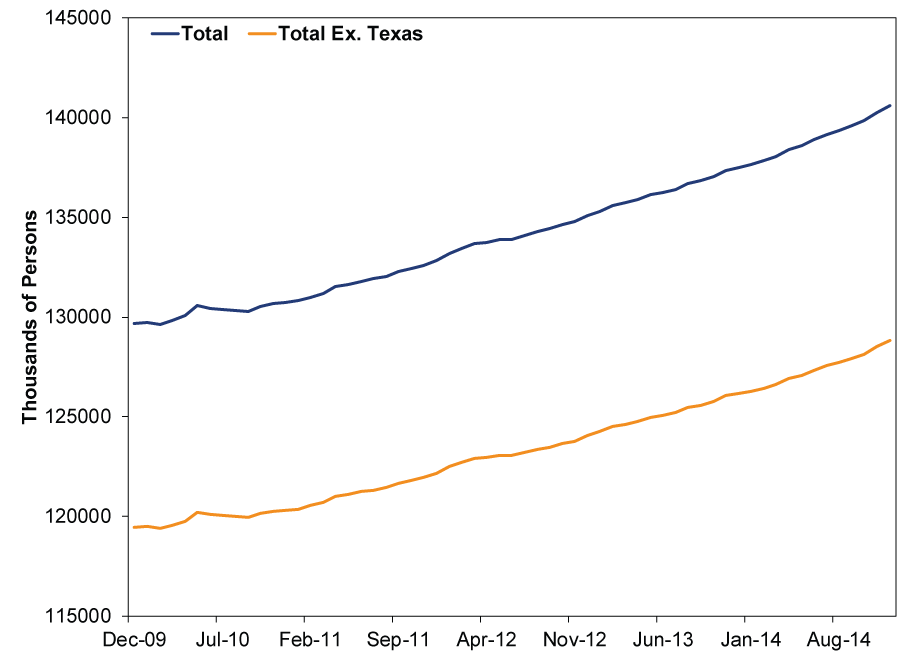

Yep, everything's bigger in Texas, including job growth! But, if you look at total payrolls, it's clear the US actually doesn't depend on Texas. There are a lot of jobs there! Of the 10.91 million jobs created from 2010 through 2014, 1.58 million came from Texas. But the Texas-sized gap between the Lone Star State and the rest of America hasn't really widened during this expansion. This isn't a two-speed jobs recovery.

Exhibit 4: Total Payrolls With and Without Texas

Source: Federal Reserve Bank of St. Louis, as of 3/6/2015. Total nonfarm payrolls and total ex. Texas[i], 12/31/2009 - 2/28/2015.

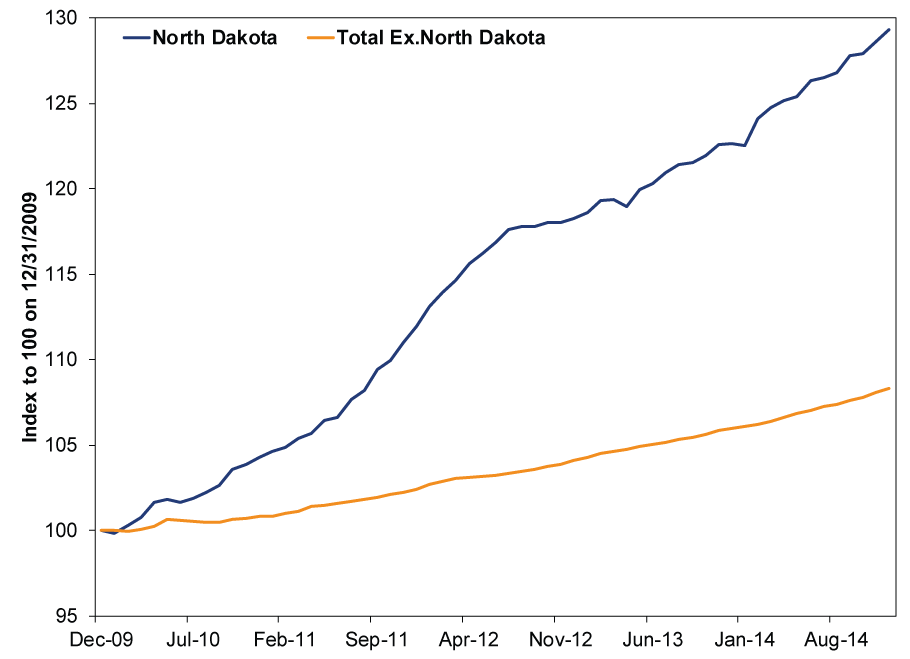

North Dakota? Same song, second verse.

Exhibit 5: Job Growth in North Dakota Vs. the Rest of America

Source: Federal Reserve Bank of St. Louis, as of 3/6/2015. Cumulative job growth in North Dakota and the rest of the country, 12/31/2009 - 12/31/2014.

Exhibit 6: Total Payrolls With and Without North Dakota

Source: Federal Reserve Bank of St. Louis, as of 3/6/2015. Total nonfarm payrolls and total ex. North Dakota, 12/31/2009 - 2/28/2015.

Cool as those shale boomtowns are, they simply aren't why US employment and output are at all-time highs and rising.

Again, all of these data are backward-looking. Employment doesn't predict stocks. But markets move most on the gap between reality and sentiment, and when it comes to oil and jobs, sentiment is far behind reality. That's a sign expectations are too low, a bullish backdrop for stocks.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i]Here is a YouTube link you probably knew was coming.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News In Orbit? On Tech Sentiment and IPOs2026-05-22

-

Market Analysis Global Bond Calamity Calls for Calm Perspective2026-05-22

-

Expert Commentary This Week in Review | UK Politics, Fed Developments, IPOs

2026-05-22

2026-05-22 -

Market Analysis CPI Sheds Light on Britain’s Price ‘Cap’ Conundrum2026-05-20

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today