Personal Wealth Management / Market Analysis

Around the World in Coronavirus 'Stimulus'

The US isn’t the only country loosening its purse strings to combat COVID-19 economic fallout.

While the US’s $2 trillion stimulus bill is hogging headlines stateside, governments around the world are rolling out their own sweeping rescue packages in an effort to mitigate the economic consequences of COVID-19 containment efforts. Here is a look at some of the major responses we have seen from North America and Europe thus far. This isn’t everything worldwide, and many more provisions may emerge or shift in the coming days. But it should give you a sense of how the globe is responding and what investors should reasonably expect from it.

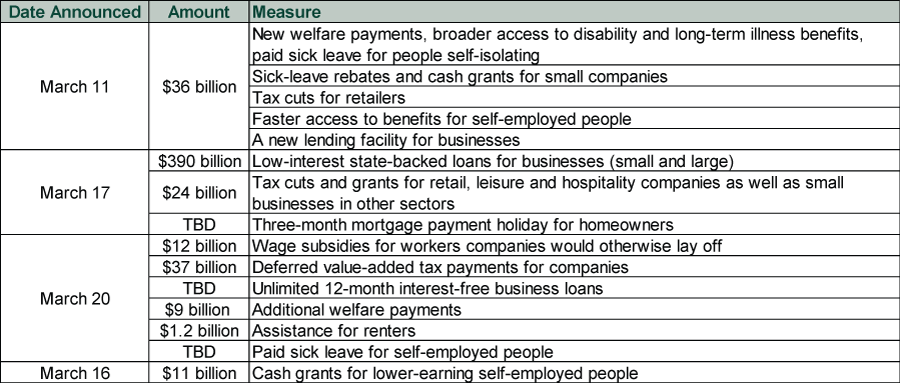

UK

Britain’s government has rolled out a sequence of measures.

Sources: Bloomberg and The Guardian, as of 3/26/2020.

As with the US stimulus plans, we are sure these provisions (and all those that follow) will spur lots of debate about the wisdom of the capital allocation, whether the funds could be spent better elsewhere and more. We won’t wade into that here—as with all such plans, eventually the money will leak into the hands of someone who spends it efficiently.

The key to these: timing. VAT cuts are immediate but don’t actually add liquidity when the issue is business closures. The other measures—like increased welfare, sick leave and grants—may help in the short run, but we doubt any can really offset the impact of interruptions to daily life. Most of them would actually hit at a lag, suggesting they mostly boost the eventual recovery rather than spur it.

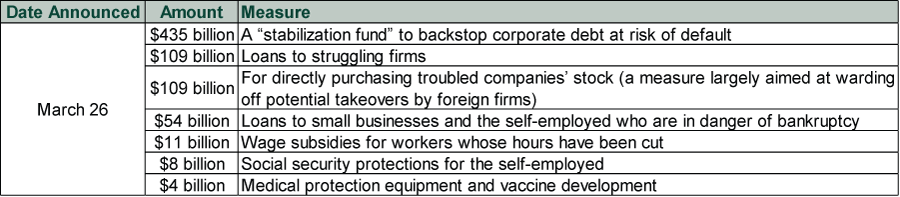

Germany

Even fiscally stalwart Germany—long considered a bastion of austerity—is getting in on the stimulus act. Thursday, the country unveiled a supplemental budget amounting to more than $800 billion designed to counter the crisis’s effects. Major provisions include:

Sources: Deutsche Welle and Reuters, as of 3/27/2020.

This plan isn’t a done deal yet—as we type, it is slated for a vote in the upper house of parliament on Friday. But, like all these measures, timing is key—and the German plan offers few details on that front thus far.

France

France is also reconsidering its plans in light of the coronavirus’s impact. In mid-March, the country announced it was scrapping its planned budget and near-totally rethinking its priorities. In the new budget:

- President Emmanuel Macron’s long-touted and controversial pension reforms—that would have amounted to benefit cuts—are out.

- On March 20, the country enacted $327 billion in business loan guarantees designed to ensure banks won’t lose out on loans made between March 16, 2020 and yearend—an effort to keep capital flowing to businesses.

- It also enacted $50 billion in delayed (and potentially canceled) tax payments, unemployment benefits and transfers to certain struggling businesses and individuals, including forestalling evictions and postponing utility bills.

The government’s loan guarantees are an interesting measure that could help businesses that need to roll over credit lines. However, whether bank will be willing to go along with the measure remains to be seen—a fact that hinges as much on the ECB and accounting principles as it does the government’s maneuvering.

Canada

Canada, like the others, has enacted a multifaceted approach aiming to ensure continued credit flow to businesses as well as increase the social safety net. Initially, the government pushed for a bill that would empower the cabinet to tax and spend without Parliamentary approval through 2021, but opposition lawmakers shot it down, and the resulting legislation was a compromise across the board.

- The key credit move: The government announced it would buy up to USD $107 billion in mortgages from banks, a move aiming to infuse them with fresh capital to lend to business and individuals.

- Separately, the government announced a financial aid package that includes a six-month delay in student loan repayments, expanded unemployment benefits for four months for workers affected by the crisis, wage assistance for small businesses, tax credits and more.

These measures, which would hit over a period of months beginning in April, are only likely to matter much if the interruptions to business prove lasting—and in that case, they are likely insufficient. In the other scenario—a quick end to the crisis—they may never be used at all.

Ultimately, and as we wrote recently, while fiscal stimulus can help money circulate some during recessions, it can’t end them. Nothing here changes our view on that. However, it is clear that, whenever disruptions to business end, fiscal policy should be a powerful tailwind for growth across much of the developed world.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today