Personal Wealth Management / Market Analysis

Behind Global Bond Yield Gyrations

Amid rising rates globally, recently elevated Spanish and Italian yields Thursday might not mean what many folks think.

Despite some folks’ seemingly day-to-day consternation over interest rate moves in the eurozone’s troubled periphery, reflecting on the last year reveals bond yields have actually fallen rather sharply. For example, Ireland’s benchmark 10-year yield topped 13% last July, but currently carries a yield of about 6.8%. Likewise, Portugal has seen marked improvement—rates fell from a 2011 peak of over 16% to roughly 12.4% now. However, it should be noted Ireland and Portugal were bailed out in 2010 and still haven’t returned to debt markets. But these secondary market rates could be seen as an indication of credit markets’ perception of their relative creditworthiness. Not-bailed-out Italy and Spain have seen rates decline off highs from last fall but still tick up in recent months. Since February's close, 10-year rates have inched up all of ... five basis points. Spanish rates are up somewhat higher (around 60 basis points) since an early March government announcement they’d increase their budget deficit target (which was later negotiated down by eurozone officials). (See Exhibit 1.)

- Benchmark yields in the US were briefly pushed higher last week.

- German 10-year bund yields likewise rose briefly this week, touching 2.07% midday Wednesday.

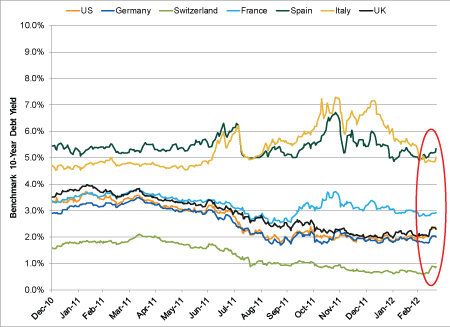

- And as Exhibit 2 shows, the US and Germany aren't alone—rates in France and the UK have also increased marginally of late.

Source: Thomson Reuters, as of 3/22/2012.

Seen in this light, it seems fathomable while the Spanish budget may have contributed to their rising rates, debt and deficit concerns likely aren’t the full story. Maybe some of the uptick is because investors are growing more confident in a global economy that’s seemingly removed the possibility of economic Armageddon this year. For example, in the US, the Leading Economic Indicator index continues to push higher. February LEI results surprised to the upside, showing progress on jobs, output and income. Falling jobless claims—which typically point to businesses anticipating increased demand down the road—also paint a picture of a growing economy. But these positive figures aren’t exclusive to the US—Japanese trade data Thursday show a pretty strong rebound, not only from last month’s disappointing data, but also from last year’s natural disasters. The list goes on—certainly not without the occasional disappointment, but nor is it all doom and gloom as some would make out. And much of the negative data should have been quite unsurprising.

Another possibility explaining perhaps part of rates’ gyrations is diminished expectations for additional central bank quantitative easing—of the Fed QE and ECB LTRO varieties, that is. Maybe increased Fed confidence in the US economy is helping ease investors’ concerns some, too. The list of possible reasons rates have, in many cases, ticked up of late globally goes on—but that just highlights interest rates’ inherent volatility in normal markets. Point is, in our view, taking just one country’s short-term rate fluctuations and drawing any broader conclusion is overly short-sighted—opening the door to missing the broader global reality.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Don’t Doubt the Old World2026-07-16

-

Market Analysis Business Friendly Bureaucracy or No, Britain is Growing2026-07-16

-

Market Analysis On the June Inflation Cooldown2026-07-14

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, China GDP, US Retail Sales

2026-07-13

2026-07-13

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today