Personal Wealth Management / Market Analysis

Behind the Baltic Drop

A widely watched gauge of global shipping costs hit a record low Monday. Here is some quick-hitting perspective.

Costs to book freighters like this one are way down lately. Photo by Ian Forsyth/Getty Images.

A low-cost Baltic isn't just for Monopoly anymore.

The Baltic Dry Index, a widely watched global gauge of shipping costs, closed at a record-low 293 on Monday, February 8. The index measures the costs to charter large freighters, and many watch it closely, believing it is an accurate gauge of global economic health-with rising costs signifying rising demand, and vice versa. Hence, to them the current drop signifies weak global demand. However, this gauge may not reveal as much about global economic health as is often presumed.

In the last economic expansion (2002 - 2007), using the Baltic Dry as a gauge of economic health was valid analysis-commodities-based industries and countries were at the forefront of the global expansion, as chronic underinvestment in mines and oil projects met strong Emerging Markets infrastructure-related demand, driving vast price increases. Shipyards responded to these price signals and constructed a huge fleet of new ships. But before most of those ships ever hit the high seas, the financial crisis struck and demand cratered.

After growth resumed, China's massive infrastructure-led stimulus from 2008 - 2010 boosted shipping prices anew. But the supply of vessels was up markedly, too-hence, costs never rebounded anywhere near their records.

When the initial bounce off the recession's trough cooled, increased vessel supply overwhelmed demand, driving down prices. The Baltic Dry Index has been weak throughout this cycle as a result, an important point to consider when weighing headlines claiming the gauge shows weak global demand.

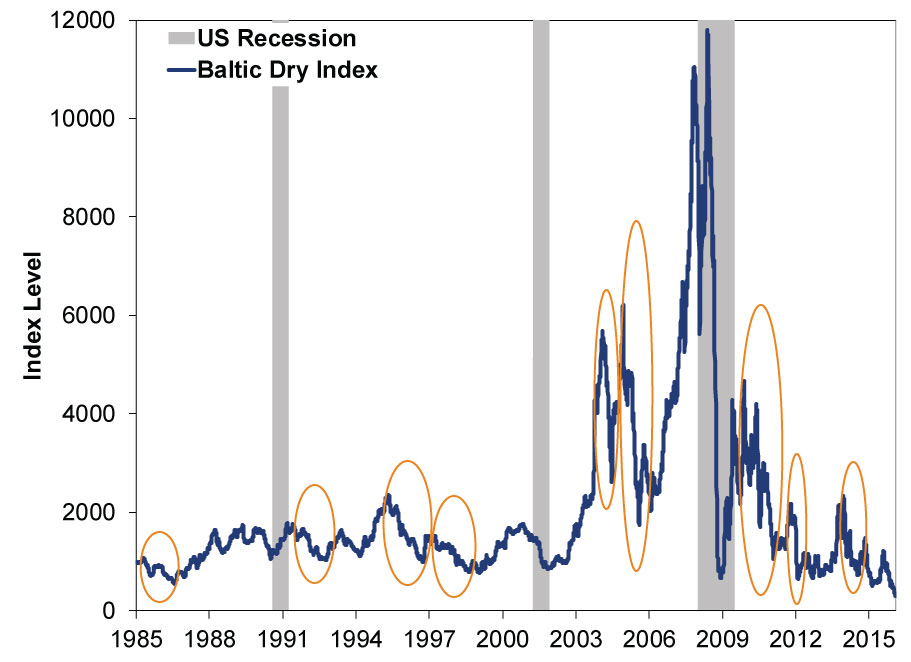

We also think it is pertinent to note that this index has only existed in its present form since 1984. In that time, it appears to have been very useful in identifying cycles only once. Exhibit 1 show the full history, with false drops (-40% or greater, and unconnected to a recession) circled.

Exhibit 1: The Baltic Dry Index and US Recessions, 1984 - Present

Source: FactSet, as of 2/8/2016.

Further, demand for commodities isn't faltering. It is really much more that supply growth has easily outstripped demand growth, leading many producers to engage in a fight for market share. Consider Australia and Brazil, the two biggest iron ore exporting countries in the world. Both Australia and Brazil saw iron ore export volumes (not prices) to China rise double digits in 2015. Iron ore exports from the third and fourth biggest Chinese suppliers-South Africa and Ukraine-grew 4% y/y and 9% y/y, respectively. Australia's Port Hedland-the world's largest commodity export terminal-sent 32.2 million tons of iron ore to China in December 2015-a 5% y/y gain. While Port Hedland's exports dipped in January 2016, this seems tied to weather disruptions. Supporting the view this is a weather-related dip, note that Brazil's January iron ore exports to China rose. Similarly, Chinese oil imports are up in volume terms, but down sharply in price terms. Demand is fine.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The Politics and Practicalities of the Social Security Trust Fund2026-06-16

-

Market Analysis Gold Fails the Safe Haven Test Again2026-06-16

-

Market Analysis A Market Perspective on Iran Truce Whisperings2026-06-15

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—June 8 - June 122026-06-15

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today