Personal Wealth Management / Politics

Closing the Books on 2022’s Midterms

Gridlock is the big winner.

Editors’ Note: MarketMinderfavors no politician nor any political party, assessing developments solely for their potential market and economic effects.

With Tuesday’s Georgia Senate runoff in the books, the midterms are over. Following Democratic incumbent Raphael Warnock’s victory over Republican challenger Herschel Walker, the Democrats will have a 51 – 49 edge, increasing their majority by 1 seat. Their edge is a whisker smaller than the Republicans’ House majority, which is officially 221 – 213, with Colorado’s third district still uncalled pending a state-mandated recount (Republican Lauren Boebert led the first tally and Democrat Adam Frisch has already conceded). Thus it is official: Traditional partisan gridlock is coming to the Beltway, creating the backdrop we call the Midterm Miracle—stocks’ tendency to rally from the midterm quarter through the following two.

Interestingly, there wasn’t much chatter about gridlock Wednesday morning. Most coverage centered on the Democrats’ slightly bigger Senate edge, which makes it impossible for just one Senator to force changes to legislation. That is a change from the prior two years, when centrist Democrats Kyrsten Sinema (AZ) and Joe Manchin (WV) had de facto veto power, leading the party’s flagship legislation to be watered down. That extra seat may help with confirmations for regulatory and other high-level positions, which is getting a ton of ink Wednesday. Yet functionally, the likelihood of contentious or partisan legislation passing Congress as a whole will be much lower in the next Congress, since bills must also pass the House. With the Republicans having a workable majority there, partisan bills that clear the Senate stand little chance. They may not even get a vote, since the House Speaker controls which bills go to the floor.

This doesn’t mean no legislation will pass. Rather, it means that whatever does pass will have to be bipartisan and, probably, milquetoast. This should be good enough for stocks, which mainly care that legislation creates minimal winners and losers and doesn’t ratchet up uncertainty over property rights, regulations and any other items that could affect the long-term return on a business investment. Typically, bills that squeak through split Congresses sand down both parties’ initial visions, losing the more radical provisions in the process. This is generally good enough to reduce legislative risk and give stocks a friendly backdrop.

Note, though: “Friendly” doesn’t mean “quiet.” Split Congresses tend to squabble. A lot. We suspect this is because politicians have to make a name for themselves, and that is harder to do in an environment where you can’t pass much to tout on the campaign trail later. Raising a ruckus in debates is an unfortunate means of compensating, and it can make things look a whole lot more contentious and dire than they really are. We point this out because it will soon be time for lawmakers to address government funding and the debt ceiling, and the phrase “government shutdown” is already getting bandied about. Prepare now to get chronic migraines from all the fearmongering about defaults and furloughed workers.

On the bright side, we guess this squabbling has a silver lining: It makes gridlock’s power stealthier, helping preserve it as a stock market tailwind. Usually, things that are regularly bullish tend to get priced in. Gridlock seems to have avoided this, probably in part because it can be hard to recognize amid all the shouting and angst that emanate from the Capitol when it reigns. Then, when the debt ceiling, budget and other seemingly mission-critical bills land on the docket, pundits couch gridlock as a massive negative for stocks and the economy. When reality beats expectations and stocks do well anyway, articles tend to call it an in spite of, not because of. In our view, this enables gridlock to quietly work its magic without folks crediting it.

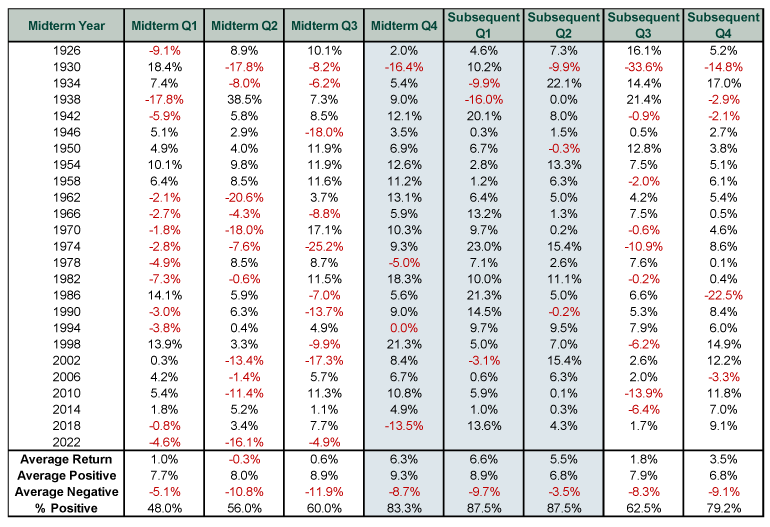

Whatever the reason, the history here is powerful, as Exhibit 1 shows. The midterm year’s fourth quarter and the following two quarters comprise the strongest stretch for stocks on the political calendar. It isn’t just that average returns are nice, but that the frequency of positivity is sky-high. We don’t think it is correct to extrapolate the S&P 500’s 10.3% quarter-to-date return forward in straight-line fashion, but it is still worth noting that it fits with stocks’ typical midterm behavior.1

With that said, volatility in either direction wouldn’t surprise from here, as there is still a bit of lingering uncertainty over things like committee chair positions. The House Speaker position remains a question mark despite Kevin McCarthy’s re-election as House GOP leader, and a tussle over the speakership could stoke some uncertainty. Perhaps these forces muddle the Miracle a bit. But they all still point to bullish gridlock over the next two years, and this—the legislative backdrop, not personalities—is what matters most for stocks, in our view.

Exhibit 1: The Midterm Miracle

Source: Global Financial Data, Inc., as of 10/7/2022. S&P 500 total returns in calendar quarters, Q1 1926 – Q3 2022.

1Source: FactSet, as of 12/7/2022. S&P 500 total return, 9/30/2022 – 12/6/2022.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

See Our Investment Guides

The world of investing can seem like a giant maze. Fisher Investments has developed several informational and educational guides tackling a variety of investing topics.

Related Resources

-

Expert Commentary This Week in Review | Breakevenitis, US-China Negotiations, ECB Policy Meeting (June 6, 2025)6/6/2025 12:00:00 AM

-

Economics Inflation Is Back to Normal6/5/2025 12:00:00 AM

-

Behavioral Finance Deep Dive: Break the Urge to Sell at Breakeven6/5/2025 12:00:00 AM

-

Market Analysis Does the Dollar’s Decline Spell Doom for Stocks?6/4/2025 12:00:00 AM

Learn More

Learn why 175,000 clients* trust us to manage their money and how we may be able to help you achieve your financial goals.

*As of 3/31/2025

New to Fisher? Call Us.

Contact Us Today