Personal Wealth Management / Market Analysis

Don’t Be Afraid of Rating Agency Downgrades

Credit rating agencies' moves reflect what markets already know.

Credit-ratings agency analysts have been a busy bunch lately. And not with upgrades. Last year, Standard & Poor's downgraded more issuers than they have in six years. Separately, Moody's placed 120 oil and gas firms and dozens of mining companies on review for possible downgrades. Fitch-the third major rating agency-has been relatively quiet thus far, but given the three agencies tend to move in lockstep, it wouldn't surprise us if they joined the party. But while these moves took headlines recently, with many quoting Moody's statement that this is a huge "fundamental shift" for commodities firms, these downgrades really aren't even news. They only confirm what markets have long known: The global commodities slump has pressured many indebted resource producers. Which is par for the course for credit-rating agencies' decisions. They have a rich history of forecasting what just finished happening, and that appears to be the case here. Investors should categorize their blanket commodities industry downgrades as noise, not news.

Credit-rating agencies base their decisions on recent and current events and other widely known information. They adjust an issuer's credit rating only when it's apparent fundamental conditions have actually changed-e.g., when oil prices fall far, it's fairly clear Energy firms' profits will drop, but the raters wait to actually get that report. Markets, however are forward-looking. If things start looking dicey, they usually begin discounting it right away. If certain developments make it likely a firm won't be able to service its debt in the foreseeable future, yields don't wait for some formal announcement to start rising. They move first.

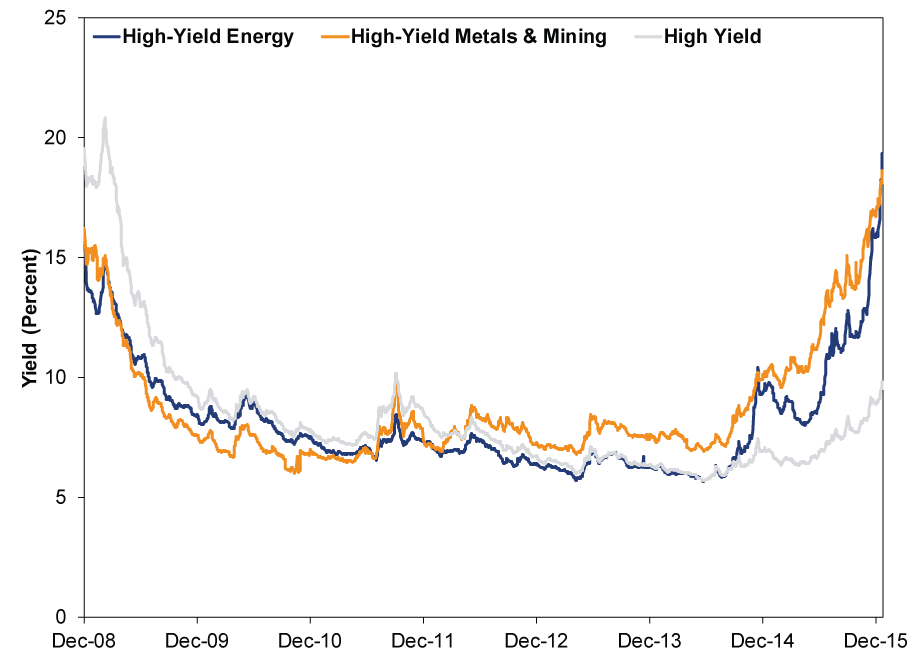

Credit markets began discounting Energy firms' troubles long ago. Energy junk bond yields first spiked in late 2014. They recovered some in early 2015, while oil prices dead-cat-bounced, then soared-far outstripping broader high-yield bond yields. Ditto for the metals & mining industry's junk bond yields. This was a sign markets knew oil and commodities' sharp declines spelled trouble for many resource firms.

Exhibit 1: High-Yield Energy and Materials Yields

Source: FactSet, as of 1/27/2016. Bank of America Merrill Lynch US High Yield Energy - Yield to Maturity, Bank of America Merrill Lynch US High Yield Metals & Mining - Yield to Maturity, and Bank of America Merrill Lynch High Yield - Yield to Maturity, 12/31/2008 - 1/22/2016.

Small cap stocks, which tend to be less creditworthy, have also been hit hard. The Russell 2000 Index is down 22% since June 23, doubling the S&P 500's drop over the same period. Small cap Energy and Materials companies are down even more. The Russell 2000 Energy and Materials sectors are down 53.0% and 25.3%, respectively, in the 12 months through Wednesday.[i]

This isn't the first time rating agencies issued downgrades after trouble was widely known. In late 2009, rating agencies began downgrading Greek debt after Greece admitted its deficit would reach 12.5% of GDP in 2010, significantly higher than previously estimated. Greece made that fateful announcement on October 20. Fitch lowered its rating from A to A- on October 22, and then to BBB+ on December 8. Standard & Poors downgraded on December 16 and Moody's followed seven days later. By then, Greek 10-year yields had already climbed from about 4.25% in October to 5.6% in December.[ii] But ratings remained safely in investment grade territory. It wasn't until Greece requested an international bailout in April 2010-the government publicly declaring the country's finances were in huge trouble-that rating agencies began lowering Greek debt to junk. By then, yields had risen to 7.8%.

In 2008 all three major credit rating agencies maintained at least A ratings on Lehman Brothers' debt until days before the investment bank declared bankruptcy. Even though Bear Stearns' failure had long since fueled rumors Lehman would be the next shoe to drop, cratering its stock price and sending credit default swaps soaring. Raters did downgrade Lehman in June 2008, but retained its investment grade. It wasn't until days before Lehman shut its doors that agencies finally cut deeply. While rating agencies began downgrading Enron's debt in October 2001, they maintained investment grade ratings until days before it collapsed in December. Meanwhile, Enron's stock and debt plunged throughout the year. A string of senior executives resigned, including then-CEO Jeffrey Skilling, who quit after only six months on the job. Meanwhile, talk of accounting issues was so common The New York Times noted it a month before ratings agencies ever downgraded.

Sometimes rating agencies' downgrades didn't even signal trouble at all. In August 2011 S&P downgraded US federal debt from AAA to AA+, the first downgrade in history. Their rationale was that the US's debt-to-GDP trajectory was unsustainable and political brinkmanship surrounding budget negotiations showed politicians were unable to make the tough choices needed to fix it.[iii] But fundamental measures of the US's creditworthiness never actually deteriorated. Interest costs steadily fell as a percentage of tax revenue. Markets also disagreed with the raters, as yields fell following S&P's announcement-typical of how sovereign issuers' yields react to a downgrade.

Moody's 2013 downgrade of UK debt-from Aaa to Aa1-tells a similar story. Moody's suggested sluggish growth may impair the UK's fiscal condition, but between fiscal 2010/11 and 2013/14, interest payments share of tax revenue fell from 8.3% to 7.8%. It dropped again in fiscal 2014/15 to 7.0%.[iv] Meanwhile, the yield on UK 10-year government bonds fell from 4% in 2010 to under 2% in 2013, and remains below 2% now. The market doesn't seem to think the UK's ability to service its debt deteriorated at all.

There may be a wave of energy and materials bankruptcies ahead, but this likely won't derail the global expansion or bull market. Resource sectors' current funk doesn't mean all firms will go under, just the most distressed, which tend to be smaller companies. Their debt represents a tiny slice of the overall $8 trillion corporate bond market. Banks have lent directly to many of these firms, too, but Energy loans are a fraction of total loans outstanding. Some junk bond funds-especially those concentrated in Energy debt-may fall sharply, but institutional and retail investors hold these funds, not banks. In short, this shouldn't imperil broader credit markets. Besides, corporate bankruptcies have not historically triggered economic downturns but instead were symptoms of them. GM filed for chapter 11 bankruptcy in June 2009 but that's precisely when the recession ended, and stocks began rising that March. Moreover, surprises move markets, not what everyone already knows. Troubled oil and commodity companies, and specifically their debt, have been widely discussed for months.

[i] Source: FactSet, Russell 2000 Energy and Materials & Processing sectors including dividends, 1/27/2015 - 1/27/2016.

[ii] Source: FactSet, 10-year Greek government bonds yields, 10/1/2009 and 12/31/ 2009.

[iii] Not only is this rationale dubious, the calculations overstated US 2021 debt by $2 trillion. When the Congressional Budget Office and White House pointed this out to S&P, it said something like, "Yeah, but actual projected debt was still large enough to merit a downgrade."

[iv] UK Office for National Statistics, as of 1/28/2016.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today