Personal Wealth Management / Market Analysis

Don’t Jump to Conclusions on Brexit’s Impact

Recent UK economic data are insufficient to draw any conclusion about the impact of June 23's vote to leave the EU.

Photo by Westend61/Getty Images

Economic data touching on Brexit's impact are starting to trickle in, prompting a slew of headlines. Thursday, falling June retail sales volumes led many to suggest Brexit's drag is underway. Friday, Markit/CIPS's very special July UK Flash Composite PMI[i] tumbled into contractionary territory, leading many more to suggest Brexit was triggering a recession. To that, we suggest staying cool. It will likely be a month or more before we have reliable, broad-based data that show how the UK economy is faring in the wake of the Brexit referendum. And, either way, it isn't likely to ding stocks much globally.

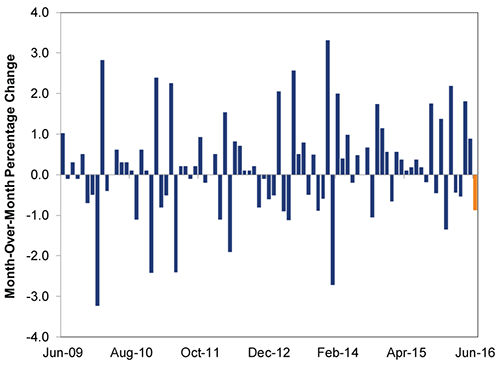

Thursday's UK retail sales report showed a -0.9% m/m drop in June, but we are skeptical this is directly attributable to Brexit. Only nine days of the period covered was post-Brexit vote.[ii]

Moreover, this is a volatile data series. Many bigger monthly drops have occurred during this expansion without signaling a materially weakening economy. Sales fell for two straight months earlier this year, and economic doom didn't follow.

Exhibit 1: UK Monthly Retail Sales Are Highly Variable

Source: FactSet, as of 7/21/2016. UK retail sales volumes including fuel, June 2009 - June 2016.

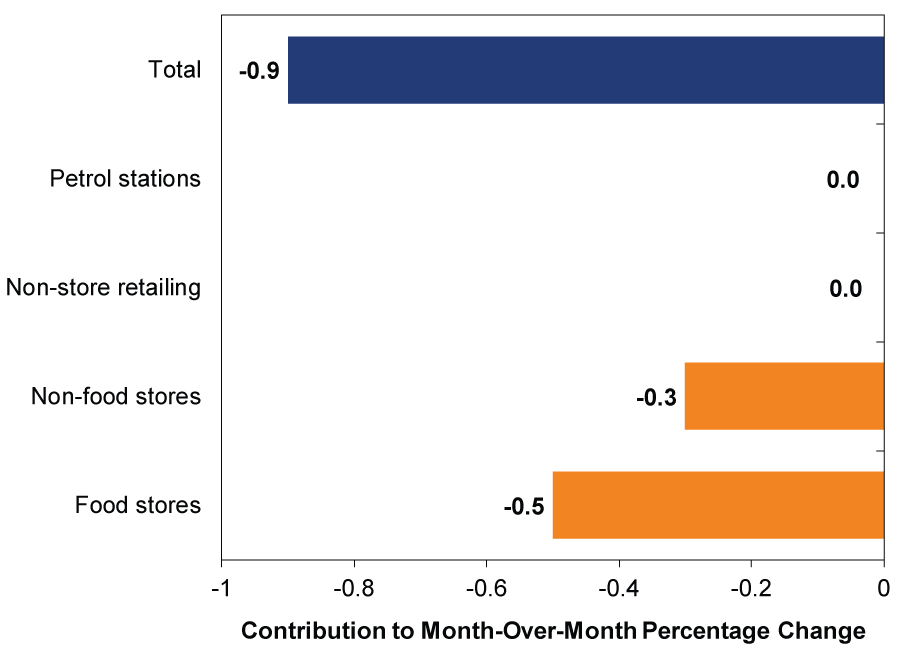

The details of the report cast even more doubt that this was Brexit-driven. Clothing and footwear sales materially detracted, falling -1.8% m/m. But according to the UK's Office of National Statistics, the British Retail Consortium and the Bank of England, this seems mostly tied to unseasonably wet weather during the late spring and early summer-and inclement weather has hit clothing sales in most of 2016. Unless you think the Leave vote was the equivalent of a successful rain dance, it's very unlikely to have played a considerable role in clothing sales' drop. Furthermore, the biggest detraction was food store sales, which most also ascribe to poor weather.

Exhibit 2: Contributions to Month-Over-Month Retail Sales, June 2016

Source: Office for National Statistics, as of 7/22/2016. Contributions to percentage change in month-over-month retail sales volumes, June 2016.

Of course, it's possible June's sales drop will begin a longer-term retail downturn, but June's reading alone won't tell you this. It's one data point.

So is the Bank of England's latest monthly business survey, which observed few signs Brexit caused a material economic slowdown, though it acknowledged some slowing demand before the vote. The July Agents' Summary of Business Conditions showed a majority of UK firms said they did not expect to alter their investment or hiring plans due to the vote. It also concluded the vote had little impact on consumer spending and didn't prompt many businesses to plan to leave the UK. Additionally, "Early evidence indicated that banks' appetite to lend had been maintained following the referendum decision." If this holds true, it would make recession unlikely, as credit fuels growth, but it's early. Everything in this report sounds great, but it's a survey and therefore squishy. It isn't predictive or necessarily even fully accurate. Credit, trade and other economic conditions could deteriorate in the months to come, but this will only be apparent as time passes.

The same holds for that special Flash July UK Composite Purchasing Manager's Index-a survey measuring the percentage of firms reporting growth. This preliminary reading, using data collected from July 12-21, fell to 47.7 from June's 52.4 (readings over 50 indicate expansion). The Services PMI dropped from June's 52.3 to 47.4, and Manufacturing clocked in at 49.1, down from 52.9 in June. Steep drops, and all implying contraction. Predictably, media seized upon this for more recession fear-based headlines, yet the results don't necessarily point to a contracting UK economy. Part of the survey is a sentiment gauge, and in the immediate aftermath of the Brexit vote, fear surged. Sentiment was the biggest detractor. While new orders and output also fell, fear could easily have played a role here, too. It isn't unusual for businesses to pause briefly while swallowing a major change, then pick right back up again. Like retail sales, this is one reading. One! Drawing big conclusions from one reading (one!) is a process error. You see, it is entirely possible business slowed in early July due to the temporary uncertainty burst tied to Brexit. But does it last? Will it carry into August or reverse? You don't get a recession from one weak month in a survey measuring the breadth of growth. You get a recession from broad-based economic weakness that persists over a meaningful period.

Hence, to reliably assess how much (if at all) Brexit is impacting the economy, you will need data covering at least several months of the post-June 23 landscape. One month is too noisy, as industrial production, international trade, consumer spending and other metrics often fall in isolated months within longer-term uptrends. Moreover, a sustained period of economic decline usually requires fundamental drivers, and presently, those are lacking. The Leave vote changed the political landscape. It may eventually change the economic relationship between the UK and EU. But that is "may" and "eventually." Presently, the UK remains in the EU and its single market. Trade with non-EU nations will likely proceed as normal and, should Brits and the EU work out a continued free-trade arrangement during their multiyear negotiations, Brexit's long-term economic impact may end up being zilch.

Either way, the likely impact on global stocks is pretty small. For one, the fact negotiations will likely take years should limit the impact on stocks. Glacial changes allow markets to slowly digest opinions, forecasts and reality, and asset prices adjust accordingly. For globally diversified investors, a UK recession (should one actually materialize) doesn't mean the global bull market is doomed. The UK is big, but its share of global GDP and stocks is about the same as Japan's. We've seen three Japanese recessions since 2009 and no global bears. Finally, whatever the data ultimately show about the UK's economy post-Brexit, it is worth remembering that markets price in widely known factors like this in advance. They are a leading economic indicator. They aren't waiting for some survey to show reality. Rising world and UK stocks suggest economic doom isn't approaching.

[i] Markit/CIPS doesn't usually publish a Flash PMI gauge for Britain-this is being done as a Brexit special. For the record, Flash PMIs are preliminary estimates using an incomplete data set that are revised or confirmed after month end.

[ii] It covered May 29 - July 2. The post-vote period began June 24.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics The Tenth Question Facing Alberta2026-08-06

-

Market Analysis Western Oil and Gas Producers Are Ramping Up2026-08-06

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today