Personal Wealth Management / Market Analysis

Drilling Deep for Oil Stocks?

How are oil producers reacting to lower prices?

And up in the headlines came a bubblin' crude. Oil, that is. Texas tea. Black gold. As the oil VIX[i] hovered near 60, some called swingin' volatility the "new normal." Others searched for meaning in bouncy benchmarks as Brent crude more than doubled WTI's monthly gains with one day left in February. Pundits parsed February's rise-the first since June-for signs of stabilization, bottoms and double bottoms. Feel free to tune it all out, because all this yammering is largely meaningless for investors. None of it tells you where oil prices will go. Nor should you let it drive you headlong into Energy stocks, as some have done lately-for all the talk of "bargain hunting," there still doesn't appear to be much upside looking forward.

Unless you're speculating on oil futures, there isn't much point in stewing over short-term swings and analysts' price targets. Volatility is just volatile. Unpredictable, too. If you're a normal long-term investor, what matters is whether prices are likelier to rise to levels that would make Energy firms profitable over the foreseeable future-solely a function of supply and demand.

Commodity prices usually move in cycles. As prices rise, firms invest more in production, hoping to ramp up output to capitalize. But they overshoot, supply outstrips demand, and prices fall. So firms cut costs and cut investment, and supply falls. Eventually it undershoots demand, and prices start rising again. These cycles can sometimes take years to play out. Energy prices stayed low for ages in the 1980s and 1990s as firms cut investment and production. They rose throughout the 2000s, and investment and production shot back up as high prices made shale production increasingly economical. And then 2014 happened.

So how are firms responding to crude's slide? Probably as you'd expect. Major international offshore oil drillers are idling rigs like it's 1995. New floating rigs, ordered during the boom years, are gathering dust.[ii] Advanced, deepwater rigs' operating costs have nearly halved as contractors compete for ever scarce business. Major offshore producers are cutting capex and scrapping planned exploration. All are hunkering down, cutting costs and focusing on efficiency.

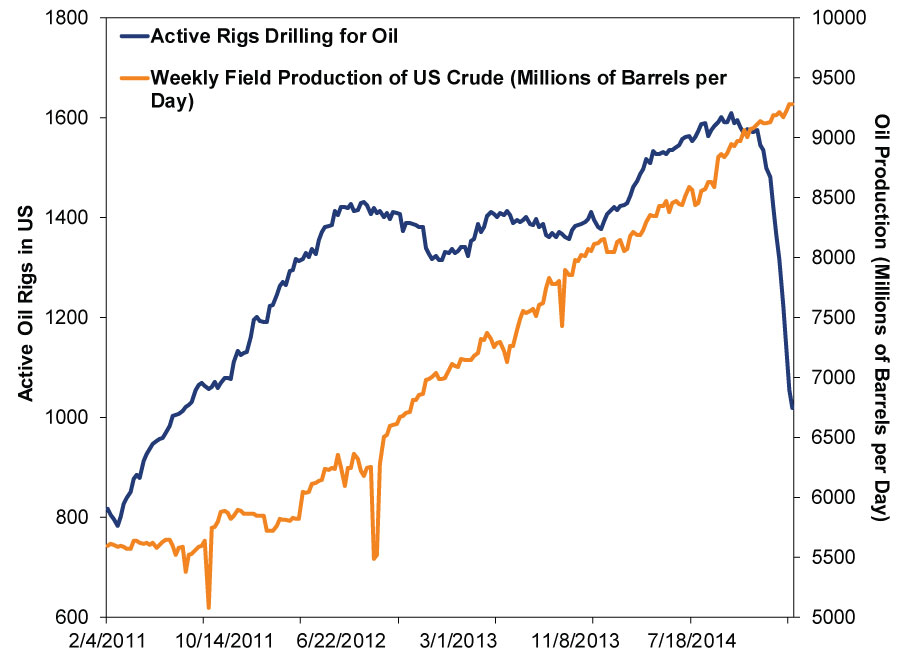

US firms are pulling back some, too. Oil-rig count has fallen 38.7% since 10/10/2014, finishing this week below 1,000 for the first time since June 2011. Yet production is still rising, suggesting firms are taking marginal producing wells offline-focusing on their most efficient gushers. (Exhibit 1). At some point, if prices stay low, production probably will fall. But for now, it seems firms still want to reap revenues to help offset the costs they've sunk into existing wells-they have financial incentives to keep pumping.

Exhibit 1: Rig Count and Production

Source: Baker Hughes, Inc. and the US Energy Information Administration, 2/4/2011 - 2/20/2015. We would have updated it through 2/27, but production won't come out until next week, so no dice. Sorry.

Not so in Britain, however. According to the updated Q4 GDP figures released Thursday, which give the first glimpse at spending, North Sea oil investment tanked. The oil and gas industry's investment in buildings and structures plunged -22.4% q/q, snowballing after Q3's -2.2% drop. This isn't terrible for the UK economy-overall growth continued, powered by consumption, exports, services and manufacturing-but it shows how low prices are pressuring high-cost projects like Britain's offshore wells.

Not everyone is pulling back. Oil-dependent nations are pumping away. Like Russia, which is reportedly courting Chinese investors to help develop more (and more advanced) oilfields. Industry analysts estimate Saudi Arabian production at 10 million barrels per day, the highest since last July. Broader OPEC output rose in January. Nations who lack the US and UK's diverse economies don't have the same flexibility to cut output without causing severe economic harm.

With production still rising overall and firms only just starting to cut back in some places, the longer-term supply trends don't seem likely to rise any time soon. Meanwhile, demand is growing, but not as quickly as supply, suggesting prices probably won't shoot up tomorrow. Or next week. They might stay volatile in the short term, but for the foreseeable future, supply and demand don't seem likely to change wildly enough to drive oil prices back into hugely profitable territory for producers. Betting on a big turnaround in Energy shares seems premature at this juncture.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] Yes, this really is a thing.

[ii] Metaphorically, because we are fairly certain dust does not gather on objects on the open sea. Other things, like salt, yes. But probably not dust per se.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Market Volatility, Energy Markets, US Inflation

2026-03-13

2026-03-13 -

Market Analysis Due Diligence and the DOL’s DOA Fiduciary Rule2026-03-13

-

In The News Oil prices will be lower in 6 months than when Iran conflict began, Ken Fisher argues2026-03-12

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today