Personal Wealth Management / Economics

Easing, British-Style

The BOE passed on more quantitative easing—for now.

It seems the Bank of England’s doves have more support for future quantitative easing. “More support” is a bit relative. Three of nine members voted “yea” on more stimulus, up from a solitary stimulus vote in the prior meeting.

But let’s talk about this word─stimulus. What the “yea” voters are calling stimulus is increasing a program, not dissimilar to the Fed’s, of buying long-term debt. This pushes money into the banking system—increasing reserves and theoretically giving banks more leeway to lend. But at the same time, it puts downward pressure on long-term interest rates. For individuals and firms, that should reduce the cost of long-term borrowing. And if banks were eager to lend, that could conceivably increase economic activity.

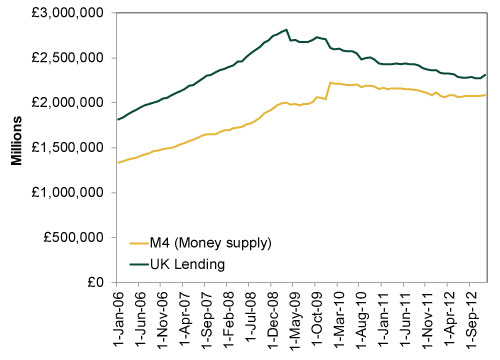

And there’s the rub—if banks were eager to lend. Demonstrably, they’re not. UK lending actually grew through the 2008 global credit crisis. But since reaching a peak in February 2009, it’s largely fallen off, as has money supply actually circulating in the UK economy. (See Exhibit 1.)

Exhibit 1: UK Lending Vs. Quantity of Money

Source: Bank of England, monthly amounts of M4 money supply and M4 lending excluding securitizations (monetary financial institutions’ sterling net lending excluding securitizations to private sector), seasonally adjusted, 01/01/2006 to 12/31/2012.

Whyis lending and money supply contracting if the BOE is, ostensibly, “easing”? The BOE’s repo rate has been at 0.5% since 2009. With the lower-end effectively fixed (without much room to go lower), such proposed “stimulus” flattens the yield curve. The difference between the long and short ends on a yield curve is effectively the operating profit a bank can make on its next loan. Flatten the yield curve, and you pinch bank-lending profit margins (in industry speak, net interest margins). Hence, such stimulus isn’t very stimulating, no matter how much money the BOE (or the Fed, for that matter) pumps out. (Call it “contractionary easing” perhaps?)

So that’s happening, but also (and more so than in the US), the UK faces an ever-changing regulatory environment. There’s the phase-in of new Basel III standards. In addition, the UK has been more proactive in proposing and codifying new regulations aimed at banks. For example, a new proposal would give the BOE power to not just “ring fence” multi-line financials (i.e., separating commercial and investment banking operations) but forcibly break them apart should the regulators feel they aren’t in full compliance with rules (many of which don’t exist yet). The intention is benign—increase capital cushions and prevent a repeat of 2008’s credit crisis. So banks not only must contend with new regulations they know about, but also with the heretofore undrafted rules and new powers regulators seem poised to wield. (Cue the deer in headlights.) UK banks face a choice. They can try to increase profits when the yield curve is relatively flatter by lending at higher rates to riskier borrowers. However, doing so means they might run afoul of future rules—or even differing opinions on existing ones—and thereby potentially risk a forcible break-apart at the hands of the BOE. Alternatively, they can cool their heels for a bit, collecting a small but risk-free rate by parking reserves at the BOE and waiting for the dust to settle. (Sound familiar? This is akin to what’s going on with the Fed.)

There’s that to contend with, and coming changes to broader Financials regulation as Britain’s Financial Services Authority (FSA) ceases to be, replaced by three new agencies all brought under the stewardship of the BOE as Mark Carney succeeds Mervyn King as Governor (reversing much of the regulatory streamlining that resulted from the Big Bang). Meanwhile, politicians are scratching their heads why growth has been sluggish and smaller firms unable to access credit, all while they’re demanding a pound of flesh from banks.

There’s some conjecture new Governor Carney will head a more dovish Monetary Policy Committee—and he may indeed, if one views the sole definition of “dovish” as “eager to pump out excess reserves, never mind if banks want to lend that money.”

Meanwhile, the current naysayers are more concerned about inflation, which is a touch above BOE’s 2% inflation target and is expected to stay there. Fair enough. But it seems to us a bit irrational for policymakers to fear inflation stemming from the BOE’s “stimulative” “easing” that discourages loan growth and slows money’s moving through the economy. After all, their dis- or deflationary policy may well dampen said inflation.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 30 - April 32026-04-06

-

Expert Commentary US Inflation, Fed Minutes, Consumer Sentiment | 3 Things You Need to Know This Week

2026-04-06

2026-04-06 -

Expert Commentary This Week in Review | Q1 Recap, Earnings Guidance, Elections

2026-04-03

2026-04-03 -

Market Analysis A Forward-Looking Lesson One Year After Liberation Day2026-04-02

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today