Personal Wealth Management / Market Analysis

Full Faith and Credit

As the debt ceiling drama kicks into overdrive, it’s worthwhile to step back and look at whether the fuss is truly warranted.

At Fisher Investments MarketMinder, we’ve said it before and we’ll say it again (and possibly even yet again before August 2 arrives): The debt ceiling is arbitrary and the debate entirely political. Politicians have been and will continue to tie it to broader issues like entitlement reforms, budget proposals, tax reform and more. But let’s limit this to the real issue: the debt ceiling and what happens if it isn’t raised.

Investopedia defines default as “the failure to promptly pay interest or principal when due”—which implies a sheer lack of funds to cover debt payments. In the US’ case then, debt repayment primarily refers to interest and principal payments on government-issued debt like Treasurys. Now remember, the debt ceiling governs the aggregate amount of debt—meaning the government can issue new bonds to replace the principal of maturing bonds. So the debate is really primarily over interest payments.

And as it turns out, tax receipts are currently sufficient to cover debt interest payments. That means not lifting the debt ceiling doesn’t necessitate a default. Not only that, but according to CBO estimates, the US can likely also continue to make Social Security, Medicare and Medicaid payments. Now, some argue the Treasury cannot prioritize its payments to put interest first. But during another episode of political bickering over the debt limit in 1985, the Government Accountability Office (GAO) stated the Secretary of the Treasury does have the authority to choose the order in which federal government obligations are paid. (See here for the actual note.)

So what would be impacted if the debt ceiling isn’t raised? Well, government could shut down, so we’d be back to mid-April’s debate over closing the federal government’s doors until a new debt ceiling deal can be reached. But remember, government has shut down before with no urgent, dire consequences. In 1995, government shut down for a few weeks with no dire consequences (excluding possible political popularity shifts). Recently, Minnesota’s state government went on hiatus. No dire consequences. So all in all, it seems most likely any issues stemming from a shutdown now would be political in nature.

Question: What’s happened to Portuguese, Irish and Greek bond rates over the last seven months (give or take) as their debt issues have become increasingly troublesome? Correct, they’ve nearly uniformly increased. Why? Because as investors’ concern about those countries’ abilities to repay their debts has increased, the interest rate they’ve demanded to hold their debt has also.

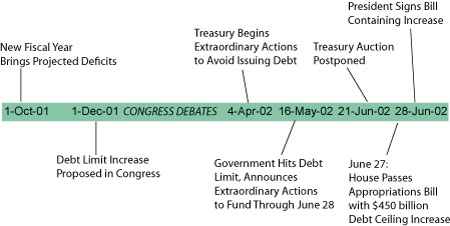

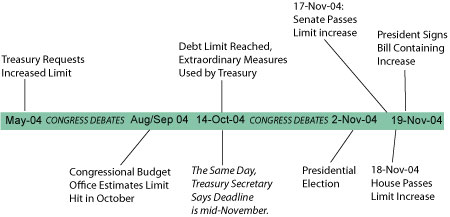

Now, what’s happened to US rates as debt discussions have heated up? Well, not much—if anything, they’ve come down slightly. So investors globally aren’t terribly concerned about US debt. So is investors’ (and markets’ in general) faith misplaced? Likely not. Historically speaking, the debt ceiling has been increased 90 times since 1940—and many of these have involved contentious debate. Today, many folks dismiss this long track record of bumping the ceiling higher by claiming “it’s different this time.” But is it really? Let’s take a quick review of some history. The timelines below illustrate the course of the political debate from the hotly contested 2002, 2003 and 2004 debt ceiling increases.

Exhibit 1: 2002 Debt Ceiling Timeline

Source: Congressional Research Service, Fisher Investments Research.

Exhibit 2: 2003 Debt Ceiling Timeline

Source: Congressional Research Service, Fisher Investments Research.

Exhibit 3: 2004 Debt Ceiling Timeline

Source: Congressional Research Service, Fisher Investments Research.

In all three cases above, debate over the debt ceiling swirled for months, the Treasury used extraordinary measures to fund government while warning of potential default and legislation was ultimately passed only days before the Treasury’s stated “deadline.” Now, this history may or may not continue playing out exactly as the above—but it’s helpful in at least setting expectations. What this shows is the political wrangling over the debt ceiling is not only not unusual, it’s typical. It would, in fact, be a modestly pleasant surprise if a deal were completed well in advance of the deadline (something April 2011’s government shutdown debate illustrates in the current Congress).

The debt ceiling is a political invention, designed by politicians to curry public favor for...politicians. Don’t believe us? Just try and figure out the rationale for what they have lifted it to. Right now, Democrats are generally arguing the ceiling should provide us leeway through 2012’s close. Not coincidentally, there’s a little matter called a “presidential election” in between now and then. And others are arguing the President should declare the debt ceiling unconstitutional. Ignore the fact the President can’t declare anything unconstitutional for the moment (that’s the realm of government’s third branch—the judiciary)—that such a possibility is even under consideration speaks to the political nature of the entire discussion.

At the end of the day, this debate is much more about upcoming elections, politicians’ reputations, political parties’ dedication to their platforms and good ol’-fashioned politicking and grandstanding. Saying the US debt’s backed by the full faith and credit of the US government is still very much meaningful—and those who say otherwise likely have some other agenda in mind. When the rubber meets the road, it’s overwhelmingly likely the debt ceiling is raised.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Q2 US GDP’s Stealthy Strength2026-07-31

-

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31 -

Market Analysis Don’t Fret the EU’s Low Summertime Gas Storage Levels2026-07-31

-

Economics On Fires and GDP2026-07-30

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today