Personal Wealth Management / Politics

Goldilocks Gridlock

Whether midterm election results leave you enthralled or enraged, the gridlock they bring is the real reward for investors.

We vote for gridlock. Photo by Scott Olson/Getty Images.

A reminder: This article deals with politics, which we are told is often a contentious topic. Please note we don't favor any political party-Republican, Democrat, Tory, Labour, Green, LDP, DPJ, Fidesz, etc.-and believe that ideology is blinding and quite dangerous to your portfolio's health. All (excluding maybe Fidesz) have done good and bad things for stocks over time.

Hey! Did you hear? The US midterm elections are over, with the Republicans logging a lopsided win to wrest Senate control from the Democrats and increase their House majority. Well, of course you did. Additionally, the GOP took the majority of the gubernatorial races, in what amounts to an electoral trifecta (or tri-terror, depending on your point of view). We admit, we were modestly surprised by the victory margin. As we wrote here and here, the structure of this year's midterm tilted Republican all along, but we expected a Senate sweep would require a virtually perfect campaign. Ah well, the outcome is the same either way-gridlock, which stocks love. In fact, we got even more delicious gridlock than we expected. We would suggest tuning out the media speculation over what it all means and where the two parties can agree. Celebrate instead this bigger, material positive for stocks.

Interested in market analysis for your portfolio? Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

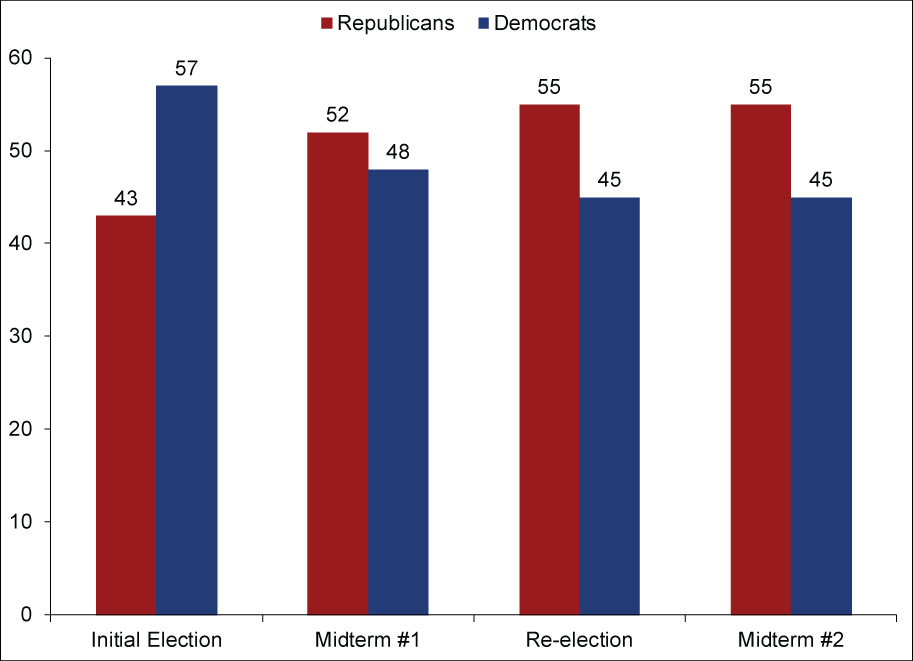

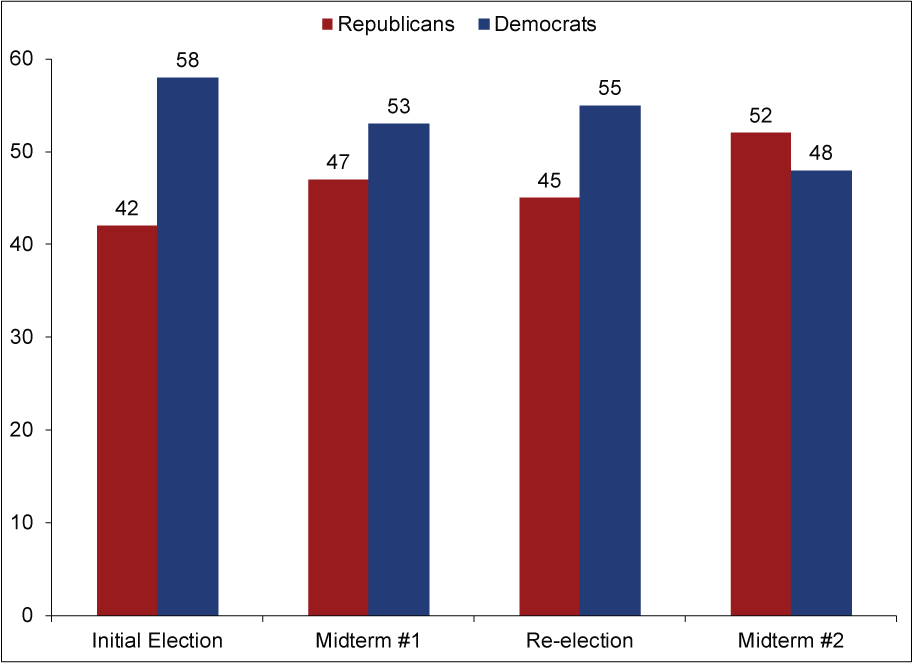

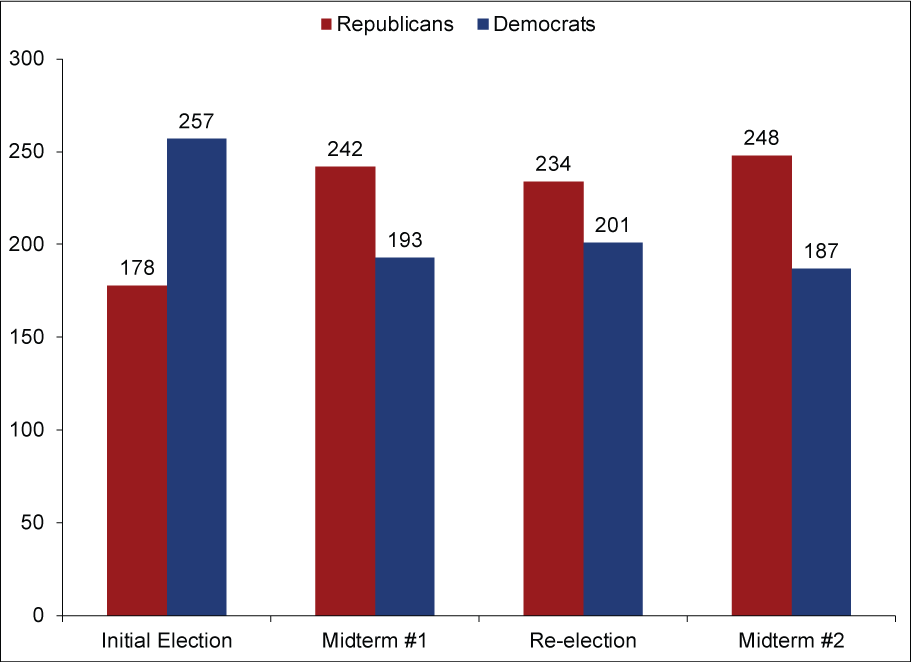

We figure most readers are probably well aware the Republicans finished Tuesday assured of having 52 Senate seats, with three more still undetermined. At most, that means Republicans will have a majority equivalent to the one the Democrats enjoyed (?) in the current Congress.[i] Whether it's 52 or 55 isn't very relevant though. Neither amount to a filibuster-proof majority. Neither, importantly, are sufficient to override a potential Obama veto without Democrats siding. Even when added to the increasingly GOP-controlled House (the Republicans added 14 more seats, bringing their edge to 248 - 187), it seems pretty clear contentious legislation backed by either party is likely a nonstarter. The gridlock now more resembles that seen under President Bill Clinton from 1994 on. (Exhibits 1 and 2)

Exhibit 1: Senate Control Following Elections, Clinton Administration

Source: United States Senate. Independents have been added to the Democrats' total, as per their voting tendencies.

Exhibit 2: Senate Control Following Elections, Obama Administration

Source: United States Senate. Independents have been added to the Democrats' total, as per their voting tendencies. Midterm #2 is an estimate based on votes counted as of this writing. 52 and 48 could change to as much as a 55 - 45 Republican edge.

The House looks similar for both-both Democratic Presidents had Democratic-controlled Houses before their first midterm, and then never again. (Exhibits 3 and 4)

Exhibit 3: House Control Following Elections, Clinton Administration

Source: Clerk of the House of Representatives. Independents have been added to the Democrats' total, as per their voting tendencies.

Exhibit 4: House Control Following Elections, Obama Administration

Source: Clerk of the House of Representatives. Independents have been added to the Democrats' total, as per their voting tendencies.

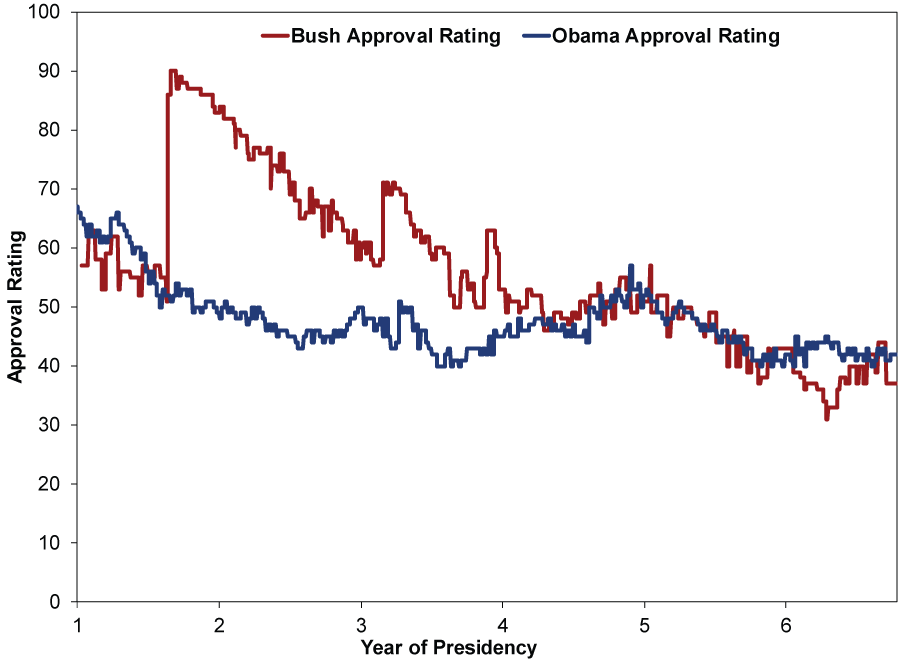

Now, the post-mortem on this will probably last for months, but we suspect the surprisingly big win at least partly stems from the same force that drove 2006's big Democratic victory-like President George W. Bush then, President Obama is quite unpopular today by historical standards. Excluding a slight wiggle earlier this year, the two presidents' approval ratings have tracked closely throughout their second terms. (Exhibit 5) And the midterm results were extremely similar.

Exhibit 5: Obama and Bush Approval Ratings Through the Second Midterm

Source: Gallup.

To put this further into perspective, consider: According to Gallup, Richard Nixon's approval rating with the opposition (Democrats) on August 5, 1974-four days before resigning in shame-was 13%. Bush and Obama ran under Tricky Dick's final mark for months before their respective midterm whitewashings. In the final poll before the 2006 midterms, Bush logged a postwar low 7% approval rating with Democrats. This year, Obama's approval among Republicans was 9%. Neither Bush nor Obama exceeded a 35% approval rating from Independent voters polled on the eve of the midterm.[ii] The President's party is unlikely to gain seats in a midterm without winning material support from independents and some support from the opposition.

Midterms ordinarily generate gridlock to some extent. Since 1926, the President's party increased control during midterms only twice. And as we've noted (and show below in Exhibit 6), midterms bring an unusually high frequency of positive market returns. Midterm election year Q4s and the subsequent Q1 and Q2 have each been positive in 86.4% of occurrences since 1928.

Exhibit 6: Midterms and the 86.4% Miracle

Source: Global Financial Data, Inc., as of 11/05/2014. S&P 500 Total Returns, 12/31/1925 - 09/30/2014.

While the 86.4% figure repeating is an odd coincidence, that this far exceeds the average quarter's 67.8% frequency of positivity isn't, in our view. Gridlock is bullish because it reduces one source of risk-contentious legislation impacting property rights, obstructing trade and business or otherwise materially disrupting commerce. These sorts of laws are usually nonstarters in a gridlocked Congress. The likely absence of this negative is a positive-but most investors don't realize it. Many get blinded by ideology, attempting to discern what the election means. Or their search for a positive catalyst causes them to overlook the non-negative.

This is where the media is today, reveling in a fantasyland of speculation about what who is going to run for the White House in 2016. This very morning, eight hours after West Coast polls closed, New Jersey Governor Chris Christie and Kentucky Sen. Rand Paul were each peppered with questions on Fox News Channel and CNN about their "intentions." (Unsurprisingly, both dodged, with varying degrees of acumen.) Whatever your thoughts about these gentlemen, their party, the opposition party, who the likely opponents are, it is premature to speculate what this election may mean for the next. Some confusingly ponder whether this new Congress will incite the necessary bipartisanship to bring "economic renewal" to the country-odd, considering America's hugely competitive private sector economy has churned higher for years amid gridlock and inaction. Besides, the aforementioned 1990s weren't exactly a time politicians held hands and sang Kumbaya, as illustrated by the Republican Revolution, long-lasting gridlock, government shutdowns and Bill Clinton's impeachment. All the while, the economy roared and stocks soared.

Let the media do the post-mortem on the midterms. Let the pundits speculate about elections two full years away. For now, we would recommend investors simply appreciate the gridlock they've got.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] We add the question mark because Congress at large only had a 7% approval rating, which, for some perspective, is only seven more percentage points than ISIS.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today