Personal Wealth Management / Market Analysis

How to Think About Health Care Stocks Now

The sector is more diverse and less defensive than many think.

Amid a global pandemic that has dominated world news, the Health Care sector is unsurprisingly front-of-mind for many equity investors. Many see it as an innovation hub offering profitable crisis solutions. Others see it as a stodgy, defensive haven. But in reality, Health Care is a diverse sector with a huge array of industries responding to different drivers. Here is a primer on how we think investors should approach the sector—both generally and in light of recent developments.

COVID-19 has put the Health Care sector under a spotlight, particularly as the race for treatments and vaccines heats up. Headlines frequently highlight individual Health Care firms’ apparent progress and speculate about winners. Health Care stocks also garner attention for their superior recent performance. Since global stocks peaked on February 12, the MSCI World Index is down -17.1%, while Health Care leads all sectors at -4.3%.[i] This leadership has burnished its reputation as a defensive sector. Many presume it is less economically sensitive and therefore likely to hold up better in a recession. Even in downturns, the logic goes, people will still consume healthcare products and services. While that has aspects of truth, we think it is an oversimplification. Digging deeper reveals more nuances.

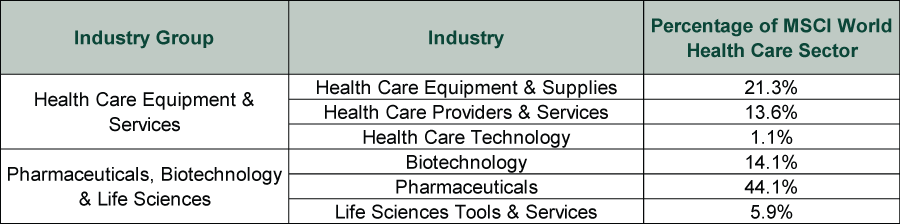

First, here is a look at the various industries comprising Health Care.

Exhibit 1: Health Care Sector Breakdown

Source: FactSet, as of 5/7/2020. MSCI World Health Care Index industry groups and industries. Percentages don’t sum to 100 due to rounding.

Most Pharmaceuticals firms fit the conventional understanding of Health Care firms, as demand for prescription drugs tends to be pretty stable regardless of overall economic conditions, helping keep Pharmaceuticals’ earnings and revenues relatively stable, too. The same holds true for Biotech and, to a lesser extent, Life Sciences. These industries are more about drug approval and innovation cycles than fluctuations in consumer demand tied to economic fluctuations. In our view, they spawned Health Care’s defensive reputation.

However, other Health Care industries are much more economically sensitive. For example, Health Care Equipment and Supplies includes makers of orthopedic devices used in procedures like joint replacements, hand reconstruction and spinal fusion. While these surgeries may significantly improve patients’ lives, they are considered elective—generally not matters of life or death. Prospective patients often delay them if they are experiencing—or expect—personal financial hardship. Deductibles and co-pays can make elective procedures a big expense. Moreover, they often necessitate long recoveries, potentially rendering patients unable to work. As a result, demand for elective procedures usually dips in recessions, hurting Healthcare Equipment and Supplies firms. Since elective procedures typically represent hospitals’ biggest profit source, demand for them also often impacts Health Care Providers & Services (which includes hospitals).[ii]

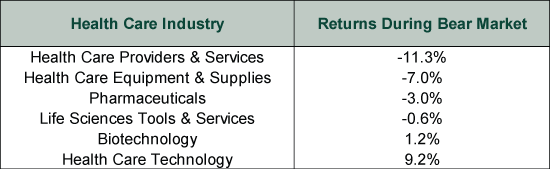

The current downturn’s unique source has contributed to a wide divergence in Health Care industries’ returns thus far in the bear market.

Exhibit 2: Health Care Industry Returns

Source: FactSet, as of 5/7/2020. MSCI World Health Care Providers & Services Index, Health Care Equipment & Supplies Index, Pharmaceuticals Index, Life Sciences Tools & Services Index, Biotechnology Index and Health Care Technology Index, total returns, 2/12/2020 – 5/6/2020.

State and local orders banning many procedures in order to prevent COVID-19’s spread and conserve medical resources are seemingly exacerbating the hit to elective procedures. Hence, overall hospital utilization is plunging. In an April 21 earnings call, one major hospital chain reported admissions had fallen by 30% thus far in April compared to the same period last year, ER visits and inpatient surgeries were down -50% and outpatient surgeries had decreased by -70%.[iii] Moreover, according to an analysis by FAIR Health, a nonprofit specializing in healthcare costs and insurance information, hospitals lose an average of $35,000 per COVID-19 hospitalization.[iv] Losses are even higher—$63,000 on average—for Medicare patients, who are generally over 65 and therefore more likely to require hospitalization for COVID. Congress has allocated $175 billion to support hospitals as a result, but whether this is sufficient to tide them over depends on how long the business disruptions last.

As for Health Care Technology’s leadership, this is intuitive, in our view. It is less economically sensitive in general since its revenues rely more on technological breakthroughs than steady patient demand. Plus, it is benefiting from increased demand for telehealth services as care providers communicate with patients staying at home.[v]

Another factor we think is driving outperformance for Biotech and some Pharmaceuticals firms: They tend to be large, growth-oriented companies with healthy balance sheets and consistently high profit margins. Such stocks have fared quite well on a relative basis year to date.

Drugmakers are also seemingly benefiting from hopes for COVID-19 treatments and vaccines. In our view, investors hoping to pick winners among them should tread cautiously. There are currently dozens of contenders, and it isn’t clear which will eventually come up with viable drugs. Second, those who do may opt to (or face political pressure to) sell it at cost in order to ensure broad access, rendering the development rather profitless. Finally, with so many focused on this, any success or likely success could swell sentiment, teeing up disappointment.

Whatever your view of Health Care, we think this sector’s diversity shows you it should be based on much more than one issue. Yet over the years, we have seen folks treat the Affordable Care Act, Medicare for All and drug price reforms as if they would impact every stock in the sector identically. In our view, taking into account key differences in industry characteristics and drivers is essential for investors in the Health Care space.

[i] Ibid. MSCI World Health Care Index total return and MSCI World Index total returns by sector, 2/12/2020 – 5/6/2020.

[ii] “Sending Hospitals Into Bankruptcy,” Editorial Board, The Wall Street Journal, 4/19/2020.

[iii] Source: FactSet, as of 5/7/2020. From HCA Healthcare’s Q1 2020 earnings call held on 4/21/2020.

[iv] “The Projected Economic Impact of the COVID-19 Pandemic on the US Healthcare System,” FAIR Health, 3/25/2020.

[v] “Demand for Telehealth Services Amid Pandemic Just What the Doctor Ordered for Investors,” Yiqin Shen, Claire Rychlewski, Troy Hooper and Kyle LaHucik, Forbes, 4/22/2020.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today