Personal Wealth Management / Market Analysis

Japan: Can’t We All Just Get Along?

America isn’t the only nation that makes political hay over budgetary stalemates.

Japan announced a largely immaterial 750 billion yen ($9.4 billion, about 0.2% of GDP) fiscal stimulus package last week with a stated aim of combatting a weakening domestic economy. The stimulus, primarily targeted at post-earthquake reconstruction measures and social programs, came amidst speculation of Tuesday’s announcement the Bank of Japan (BOJ) is providing more monetary stimulus (think quantitative easing). In fact, it was just 40 days ago the BOJ announced its most recent round of quantitative easing—expanding its asset purchase program by 10 trillion yen ($125 billion, or about 2.0% of GDP). Tuesday, the BOJ maintained its policy of incrementalism, announcing a nearly identical asset purchase program expansion of 11 trillion yen.

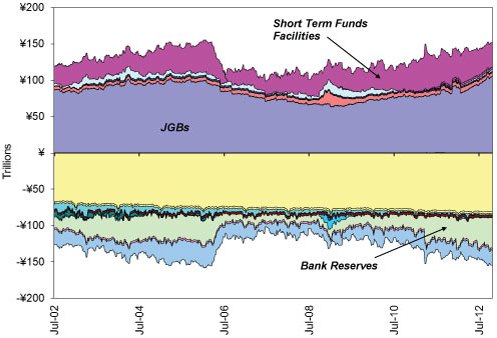

Exhibit: Central Bank Assets and Liabilities: Bank of Japan

Source: Thomson Reuters and Bank of Japan, as of 10/24/2012.

Naturally, this saga would not be complete without good old-fashioned political brinksmanship. Funds used for Japan’s latest fiscal stimulus program will actually come from Japan’s general account reserves as politicians are currently at an impasse on legislation allowing the Ministry of Finance to issue bonds—essential to finance government spending. (Sound familiar?)

Not a new issue in Japan, the budgetary stalemate—analogous to the US debt ceiling/fiscal cliff debate—is driven by the opposition Liberal Democratic Party’s (LDP) growing impatience over the timing of an intended snap election to dissolve the lower house and unseat Prime Minister Yoshihiko Noda. Prime Minister Noda, leader of the Democratic Party of Japan (DPJ), which holds the slimmest of majorities in parliament, maintains a 20% approval rating —hardly a position of leverage. Noda’s efforts to persuade the opposing LDP to pass the critical finance legislation have thus far proved futile.

Nevertheless, a financing bill needs to be passed by the end of November in order to move forward with a planned December bond auction to finance Japans deficit spending (think the US-debt-ceiling debacle last summer) and keep the government from shutting down. With recent negative economic data including exports, machine orders, industrial production and deflation coming in worse than expected, a government shutdown—and the subsequent slowdown in government spending—could certainly drag on headline GDP. It seems unlikely Japanese politicians won’t compromise on this avoidable situation, yet surely this “good crisis will not go to waste.” The LDP may force Noda to call a snap election earlier than his prior (and non-specific) timeline of “soon” in exchange for LDP votes necessary to pass the finance bill. An election could continue the revolving door of Prime Ministers in Japan—after all, Noda is the seventh in as many years.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today