Personal Wealth Management / Market Analysis

Life After Brexit: The UK Economy

While Brexit talks might hang over sentiment, the UK's economic fundamentals remain strong.

As the sun comes up, the world is digesting British voters' decision to leave the EU. The news rocked markets, and many fear more trauma is in store. As we wrote here, it will take years to discover the societal implications, and political uncertainty will likely linger for some time. But that doesn't mean markets will sink. As we discussed at length here, nothing has changed immediately. Per Article 50 of the Lisbon Treaty, the UK will have two years to negotiate exit terms and a new relationship with the EU. Slow-moving political issues like this typically fade into the background, letting cyclical factors re-emerge as the swing factor for stocks. And here, difficult as it may be to fathom in the heat of the moment, fundamentals support UK stocks. The BoE stands ready to provide liquidity as needed. Once the initial reaction fades, markets should get relief from the vote now being a known quantity. The often colorful campaigning, which dampened investors' mood in recent weeks, is over. Investors should cease assessing any and all economic data through a Brexit lens. Pundits can stop putting asterisks after all data showing growth, warning that this is prior to the Brexit vote. Investors can now home in on the data, which suggest the UK economy is in fine shape, with consumption and services leading growth.

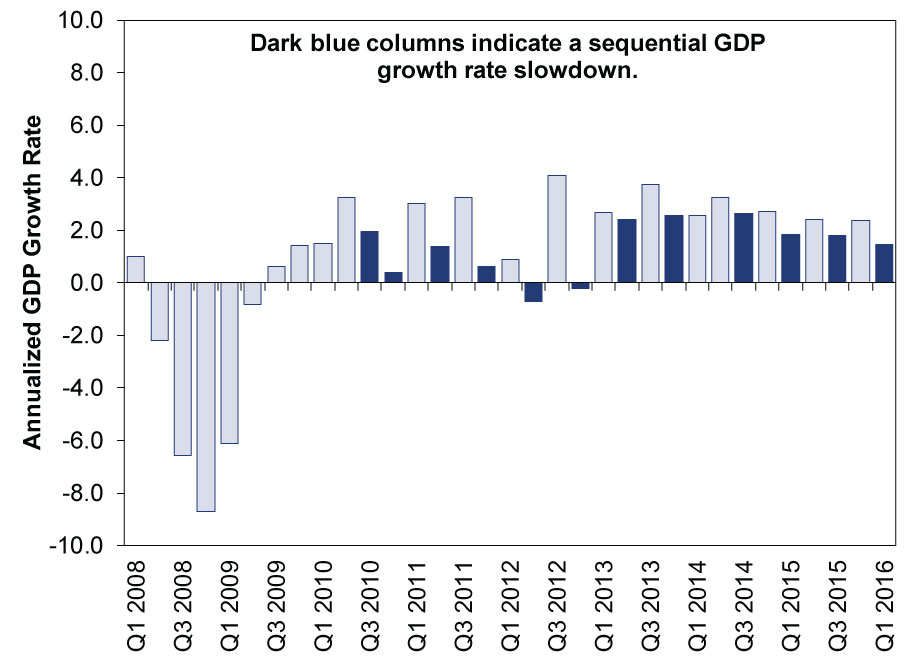

UK GDP did slow in Q1 2016, from 2.4% annualized to 1.4%.[i] However, slowdowns often come and go during expansions. Exhibit 1 shows annualized GDP growth since 2008, with slowdowns illustrated by the dark blue columns.

Exhibit 1: Growth Rate Fluctuations Aren't Unusual

Source: FactSet, as of 6/22/2016. UK GDP growth (annualized), Q1 2008 - Q1 2016.

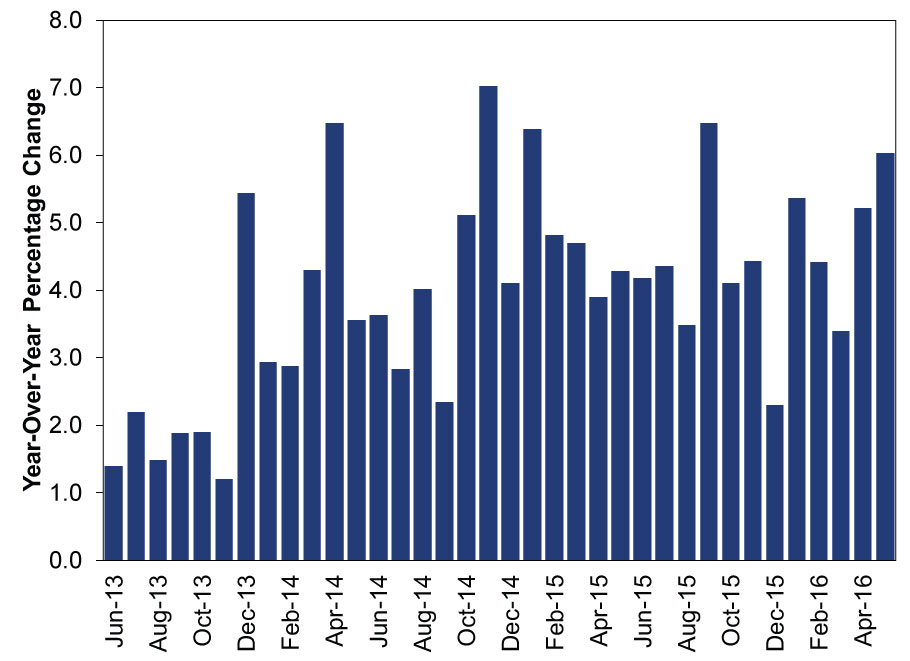

Monthly data published since Q1's close suggest growth continues. UK retail sales jumped 0.9% m/m May after a 2.0% gain in April.[ii] On a year-over-year basis, retail sales rose a whopping 6.0% y/y in May.[iii] UK consumers have been fueling growth for some time (against a near-constant backdrop of fears they'll falter, an article for another day), and there is little sign consumption is slowing. (Exhibit 2)

Exhibit 2: UK Total Retail Sales Volume

Source: FactSet, as of 6/22/2016. June 2013 - May 2016.

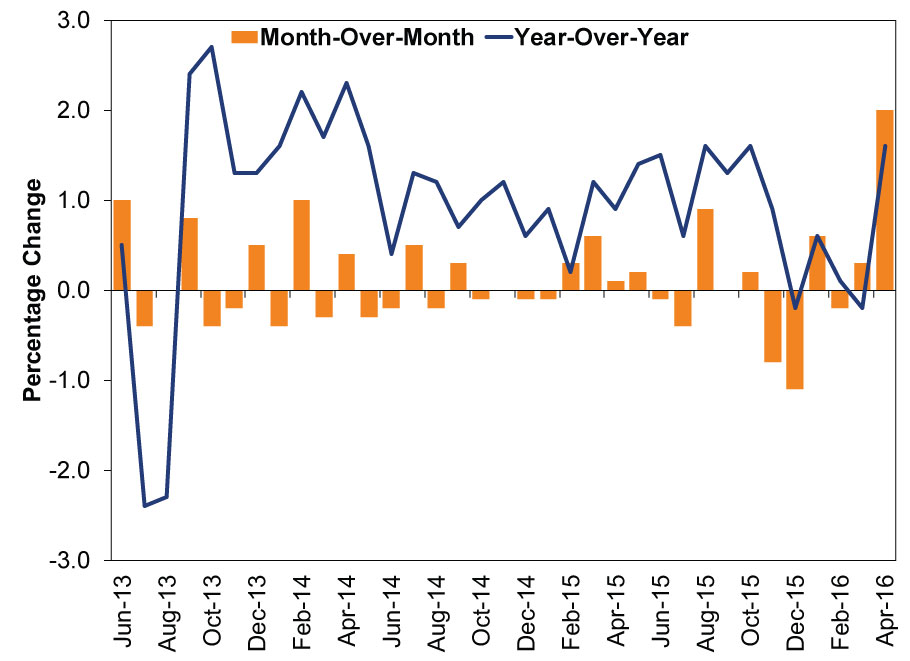

While consumption has driven growth in recent years, it is worth noting that industrial production is up in three of the last four monthly readings, and it jumped markedly in the latest report (April). (Exhibit 3) Far be it from us to suggest this indicates rebounding industrial production, at roughly 15% of GDP, is going to drive growth. But it isn't showing signs of material weakness lately.

Exhibit 3: UK Industrial Production

Source: FactSet, as of 6/22/2013. June 2013 - April 2016.

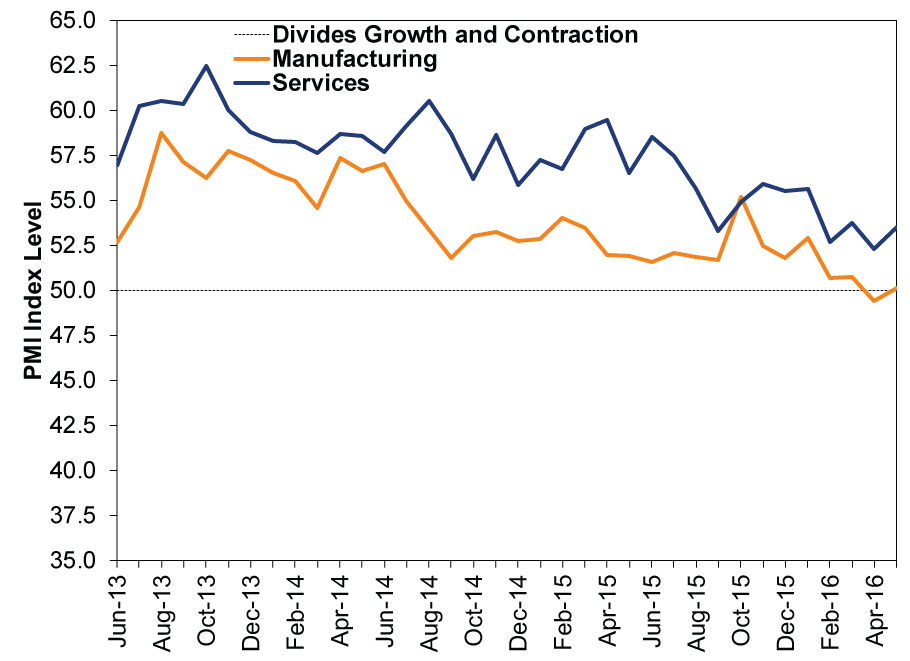

While Markit's UK Purchasing Managers' Indexes (PMI) for Manufacturing (50.1) and Services (53.5) have ticked down from years past, both topped 50 in May, suggesting more than half of surveyed firms reported growth. What's more, these gauges don't measure the magnitude of growth (unlike GDP or output measures), instead illustrating how broadly growth is spread. Hence, PMI's downtick doesn't necessarily mean slower GDP growth.

Exhibit 4: Manufacturing and Services PMIs

Source: FactSet, as of 6/23/2016. June 2013 - May 2016.

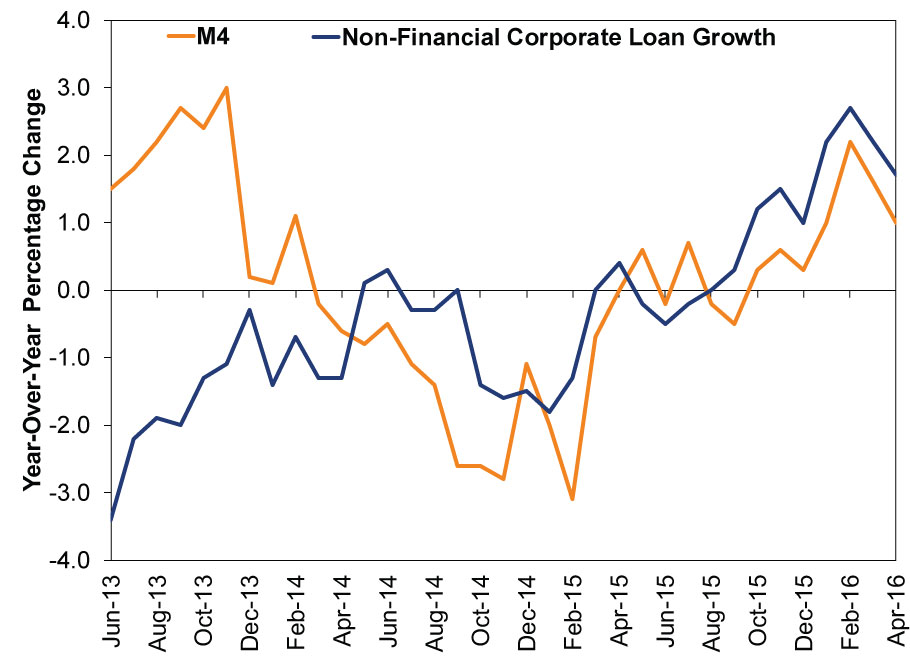

While The Conference Board's Leading Economic Index has posted flat reads for two straight months, this is driven largely by two survey-based indicators-consumer expectations and the expectations for housing sales. Both could easily have been skewed by Brexit uncertainty. Credit market gauges, less subject to skew, show growth. UK broad money supply (M4) and loan growth to non-financial companies are rising and the yield curve is positively sloped, suggested lending should support growth looking forward.

Exhibit 5: UK M4 and Non-Financial Loan Growth

Source: Bank of England, as of 6/22/2016. June 2013 - April 2016.

As the Brexit fog lifts, we expect investors will see economic fundamentals like these more clearly, and the fear of major Brexit fallout will give way to relief.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today