Personal Wealth Management / Economics

Parsing Profits

Stagnating headline earnings aren't the full story.

Recession. In economics, it refers to a sustained period (commonly measured as two straight quarters or more) of reduced output, commerce and a general widespread malaise. Thankfully, this isn't the case right now in most of the world, but some suggest we're in a different kind of recession-a "profits recession," in which a period of mildly lower US corporate profits allegedly bodes poorly for stocks. As evidence, they point to falling S&P 500 earnings in Q2 and expectations for another drop in Q3-widely known information at this point, and largely baked into stock prices. Moreover, these seemingly dreary numbers have some key mitigating factors, and the overall profit picture is better than most presume. Corporate America should continue providing fundamental support for stocks.

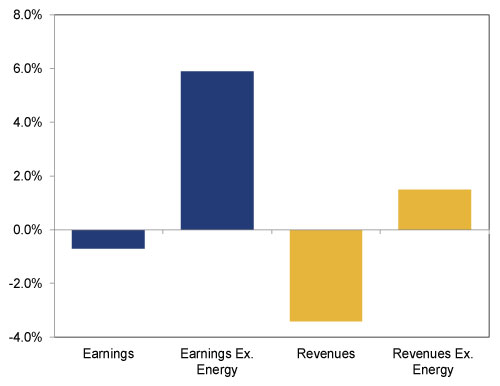

With 490 S&P 500 companies reporting, aggregate Q2 earnings growth is estimated at -0.7% y/y. But Energy firms' -55.4% year-over-year drop bears most of the blame. All other sectors except Industrials enjoyed rising profits, and excluding Energy, aggregate Q2 earnings growth rises to 5.9% y/y. Some also fret the second straight quarter of falling revenues, the first such slide since 2009. Scary! But this also stems from Energy firms, whose sales fell -31.8% y/y. Factoring out that whopping drop, and aggregate S&P 500 Q2 revenues jump from a -3.4% drop to 1.5% y/y growth. We aren't in an earnings or revenues recession. We're in an Energy recession, which isn't a recession. (See Exhibit 1)

Exhibit 1: S&P 500 Q2 Earnings and Revenue Year-Over-Year Growth

Source: Factset, as of 8/27/2015. Year-over-year growth in S&P 500 Q2 earnings and revenues.

Energy's "recession" is a big negative for these firms, and judging by widespread expectations for oil prices to bounce, we think it is a negative markets don't yet fully appreciate. But for most of the rest of Corporate America, Energy's woes are an underappreciated boon-a freebie cost cut! Energy-intensive industries like manufacturing, agriculture and transportation are the most high-profile beneficiaries, but the gains are widespread. Petrochemicals are also a direct input in plastics, adhesives, fertilizers and coatings. Lower oil prices boost producers' net profits. Plus, when consumers spend less on energy, they have more to spend on discretionary goods and services, which can boost sales for firms in those industries.

Q2's profit tally also provides evidence strong-dollar fears are still weighing on earnings expectations. The dollar-as-headwind narrative says the strong currency dents earnings for US multi-nationals, as goods become more expensive overseas, hitting demand, and revenues earned overseas fall when converted back into dollars. These revenue assumptions are true, but they're only half the story. Multinationals incur overseas costs as well as sales, and the strong dollar makes foreign-sourced raw materials, components, shipping and labor cheaper. This helps offset the dollar's impact on revenues and is a big reason earnings broadly beat expectations in Q2. You can see this in the divergence between consensus expectations for earnings and revenues. As Q2 earnings season dawned, analysts projected a -4.5% drop in sales, not far from the final. But earnings expectations were also off at -4.5% y/y. Analysts underestimated the cost side. The same thing happened for Q1 earnings season. Analysts projected a -2.8% sales drop as reporting began, almost square on the target. But their pre-season profits projection of -4.6% y/y missed badly. Q1 earnings grew 0.9% (8.7% y/y excluding Energy).

That many highlight the negatives of a strong US dollar-but under-appreciate the offsetting positives-is a sign expectations remain low, and analysts don't yet appear to have caught on to reality. Currently, analysts expect Q3 sales will fall -2.6% y/y while profits fall -4.3% y/y-lower than the -1.1% y/y drop they expected at Q2's end. Yet sales expectations didn't change much in that window. Seems to us analysts remain overly pessimistic about firms' costs, setting a low bar for Q3 results to clear. Overall profits may still be flattish, but the gap between results and expectations is what ultimately matters.

The Bureau of Economic Analysis's measure of total US corporate profits further underscores the point. This captures all firms, public and private, filing quarterly corporate tax returns. After-tax corporate profits rose at a 1.3% seasonally adjusted annual rate in Q2, rebounding from two straight drops. Even if they wobble further from here, the overall choppy trend since early 2014 didn't sink stocks, and we see no reason it would be different this time.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary US Inflation, Fed Minutes, Consumer Sentiment | 3 Things You Need to Know This Week

2026-04-06

2026-04-06 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 30 - April 32026-04-06

-

Expert Commentary This Week in Review | Q1 Recap, Earnings Guidance, Elections

2026-04-03

2026-04-03 -

Market Analysis A Forward-Looking Lesson One Year After Liberation Day2026-04-02

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today