Personal Wealth Management / Market Analysis

Puerto Rico Can’t Afford Its Debt

Puerto Rico's troubles don't presage trouble for broader markets.

The Greek drama has dominated the stage lately. But is a new act coming soon-this one closer to home on the island of Puerto Rico? Some call its fiscal situation much worse than Detroit. Others see Puerto Rico as "America's Greece," an economy plagued by structural issues, too much debt and in need of deep reform. (Which piqued our curiosity. Possibility of "PRexit" has captivated the Twitterverse. Can other portmanteaux like "PRaccident" or a "PReferendum" be far behind?[i]) We'll give the "Puerto Rico is America's Greece" crowd one thing: Greece is mostly a political issue at this point, lacking size and surprise power to cause broad economic or market issues. The same can be said of Puerto Rico.

Puerto Rico's economic struggles aren't new. Since 2006, the island's economy has grown only once annually[ii] and has been plagued by various structural issues. After corporate tax breaks expired in 2006, businesses left en masse-delivering a big blow to the economy. Outdated legislation (the Jones Act) pushes up the cost of living and impedes trade with the mainland-something Puerto Rico can't afford, particularly now. Migration to the mainland US has accelerated, sapping the commonwealth of human capital and much-needed tax revenue. Rampant tax evasion and expensive government-sponsored programs have squeezed the island tight.

To buy time to revive its flagging economy, Puerto Rico borrowed heavily to fund spending-taking advantage of its debt's special tax status (US territorial debt is exempt from federal, state and local tax). In states that don't issue much debt, that benefit has historically been attractive to tax-averse investors. Add in potentially higher yields compared to some municipalities, and it's not hard to see why mainland investors, particularly national municipal bond funds, used to look favorably on Puerto Rican debt.

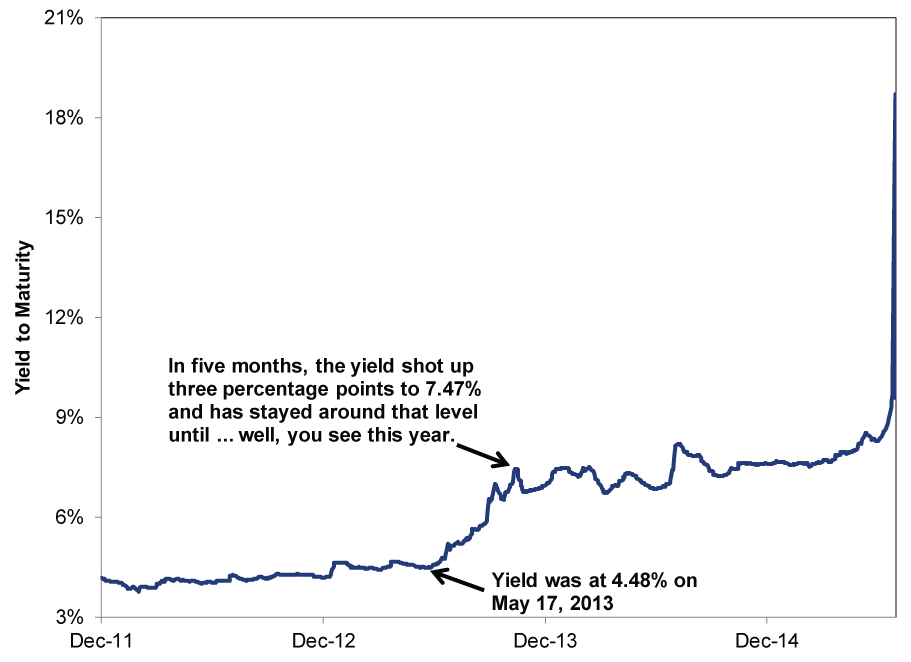

But without cash coming in from other sources, it was only a matter of time before the island started running into trouble, as Governor Alejandro Garcia Padilla admitted on June 28. However, all the things we just typed and Padilla's public declaration didn't come as much of a shock to many: The territory's troubles are well known. (Exhibit 1)

Exhibit 1: S&P Municipal Bond Puerto Rico Index

Source: S&P Dow Jones Indices, as of 7/1/2015. S&P Municipal Bond Puerto Rico Index, "Yield to Maturity" from 6/30/2005 - 7/1/2015.

Unless you own Puerto Rican bonds, most of this story is sociological, not economic-just politics and legal issues. As a US territory, Puerto Rico's situation is highly unusual. It is subject to US law, but it isn't eligible to use the US bankruptcy code and declare Chapter 9. (Being a state wouldn't help, as states can't declare bankruptcy, either.) Its constitution also stipulates that payments on general obligation bonds must take precedent before any other payments-the Puerto Rican equivalent of the US Constitution's public debt clause.[iii] As Bloomberg's Matt Levine writes:

"Unlike lending to Argentina, lending to Puerto Rico avoids the risk that the borrower will change the law on you. Unlike lending to Detroit, lending to Puerto Rico avoids the risk that your bonds will be restructured in bankruptcy without your consent. Puerto Rico's legal position encouraged investors to lend it too much money, and pay too little attention to whether it could pay it back-because they knew that, legally, it couldn't not pay it back."

The chatter today focuses on whether Puerto Rico should be allowed to declare bankruptcy like US municipalities or whether creditors should come to the table of sacrifices-interesting, but not very market-related. Legislative change isn't coming any time soon, and the federal government said assistance is unlikely.

Now, investors in Puerto Rican debt could well end up taking some losses, though perhaps not to the degree some envision. Bond mutual funds and hedge funds hold nearly 40% of Puerto Rico's debt, but only a couple muni bond funds have outsized positions. Also, most Puerto Rican bonds are insured, and bond insurers have a big incentive to prolong the process to avoid default (in which they would have to pay up). Just last week, the state-owned power utility reached a deal with creditors and bond insurers to avoid a missing a payment. Plus, Puerto Rico's debt is on a staggered maturity schedule and funded by different revenue streams-it's not one big payment all due at once. For investors, this is simply a lesson in the importance of diversification and not loading up on any one investment for tax status and after-tax yield alone. To the extent you own fixed income, it's crucial to consider why-we believe the primary role is to dampen equity volatility. Buying into an overleveraged US territorial asset for tax efficiency overlooks that.

Puerto Rico doesn't threaten municipal markets or markets at large, either. The island's global economic footprint is tiny. Though some have called Puerto Rico "America's Greece," it is actually a heck of a lot smaller. Its economy of about $100 billion would rank around Mississippi and New Mexico-numbers 36 and 37 in gross state product-and comprise about half of Detroit's gross metropolitan product. If Detroit didn't roil the US muni market-let alone global markets-when it went bankrupt in 2013, we fail to see how an economy half its size would be able to. Also, the $70 billion of debt figure getting tossed around is total debt[iv], not what's owed immediately. For the fiscal year ending June 30, 2016 Puerto Rico owes roughly $2 billion-about $1.2 billion of which are general obligation bonds, which the government must prioritize. In the $3.7 trillion US muni market, Puerto Rico's entire $70 billion in debt comprises a scant 1.9%. (And that $1.2 billion that Puerto Rico needs to pay this fiscal year? 0.03% of the whole muni market). Most of the remaining 98.1% in US muni bonds is in far better shape. Just as Detroit didn't represent all US cities when it went under in 2013, Puerto Rico isn't indicative of the typical US municipality either-its issues are its own, and markets know this. (Exhibit 2)

Exhibit 2: Puerto Rico Bonds vs. US Muni Bonds

Source: S&P Dow Jones Indices, as of 7/1/2015. S&P Municipal Bond Puerto Rico Index and S&P Municipal Bond Index, "Yield to Maturity" from 12/1/2011 - 7/1/2015.

For investors, Puerto Rico is merely a reminder: Always diversify, in bonds or stocks. It is simply not a broad market risk.

[i] Sorry.

[ii] That would be 2012. Source: Government Development Bank for Puerto Rico.

[iii] One key difference being, of course, that the US Federal Government easily has sufficient tax revenue to cover its debt obligations. Puerto Rico seems not to.

[iv] And in that $70 billion, public corporations-for which the government is ultimately on the hook-hold approximately $25 billion.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

-

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27 -

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today