Personal Wealth Management / Economics

Q3 US GDP: Comparing Pure Private Sector Components to Headline GDP

The media celebrated a growth acceleration, but a more even-keeled reaction seems apt to us.

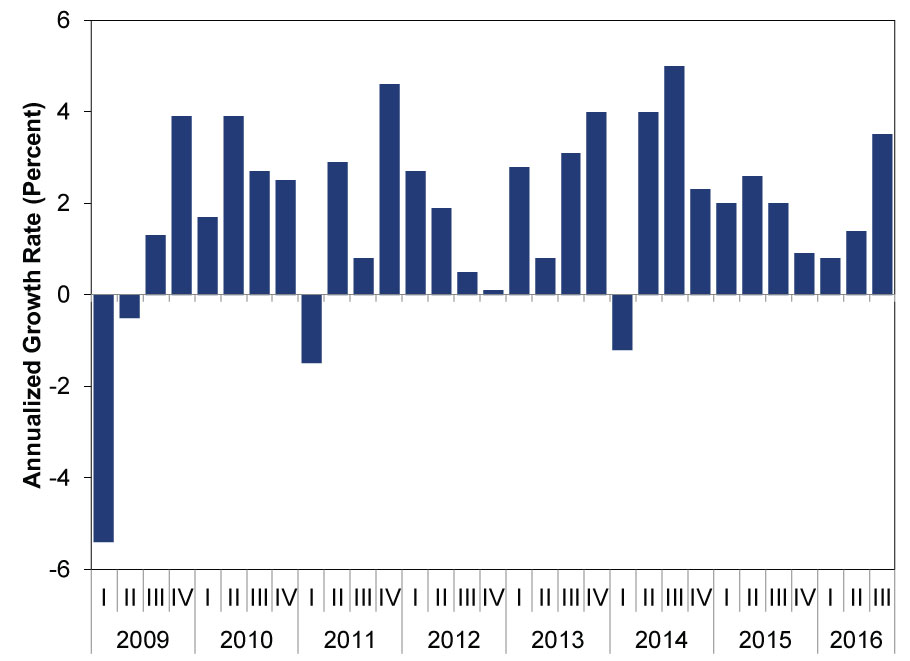

Thursday, the US Bureau of Economic Analysis released its third estimate of Q3 GDP, and the data show growth was 3.5% annualized-up from 3.2% and slightly higher than analysts' consensus estimates of 3.3%. The media was fast to seize on the sunny headline figure, with many dubbing it The Fastest Growth in Two Years. Now, they're on to fretting this growth rate is unsustainable. In terms of headline growth, we don't disagree-it is the fastest in two years and was driven by some wonky components. But under the hood, it doesn't seem like such a sharp acceleration at all-it's in keeping with the trend we've seen for years now. The reaction to this latest revision is yet more evidence sentiment is warming toward a more rational take hard data have justified for years.

GDP is comprised of personal consumption, private investment, government consumption and net exports. The "headline" figure everyone talks about is the sum of these major categories. This is what many folks presume is "the economy" in statistical terms.

Exhibit 1: US Real GDP Growth Rates Since 2009

Source: US Bureau of Economic Analysis, as of 12/22/2016.

As a statistic goes, that's all fine and dandy. Except calling GDP "the economy" overrates what the data actually show. GDP tallies government spending as always and everywhere positive. Maybe some arch-Keynesians would agree, but many economic schools of thought would note it can crowd out private investment. Someone worried about the trade deficit and pitching protectionism may agree with net exports (exports minus imports) being included, but most economists agree rising imports stem from strong domestic demand, which isn't a sign of weakness. Private investment also consists of inventory change: When inventories rise, that adds to GDP. But that rise could stem from either an inability to sell goods on hand or stocking up in anticipation of demand. It's open to interpretation. We won't even get into the accounting for the financial services industry, which is so odd that it shows a big positive contribution to UK GDP in 2008 .

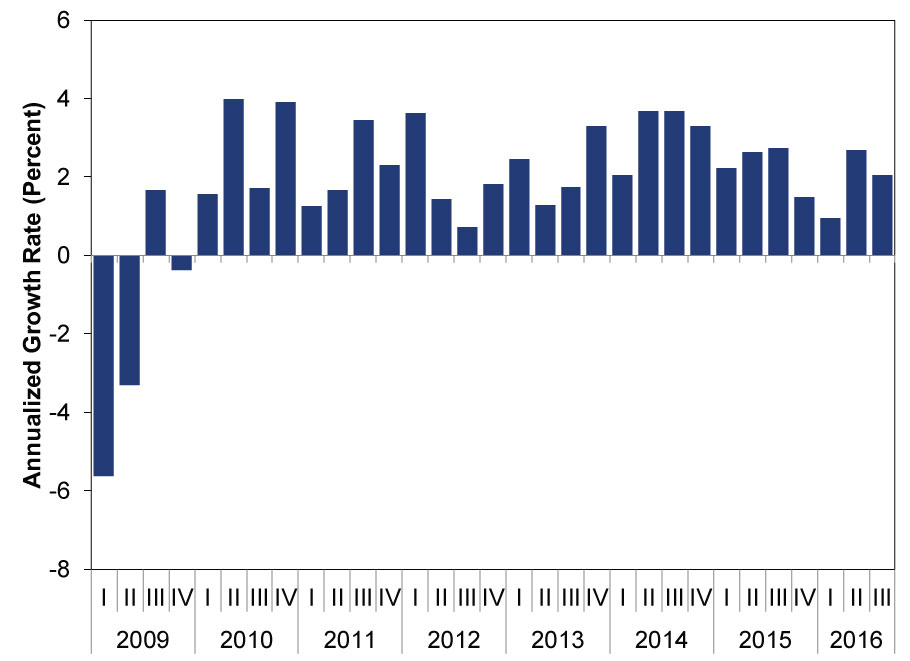

To get a cleaner view, take a look at what we call Pure Private Sector GDP. This strips out all those potential sources of noise and focuses on Consumer Spending, Non-Residential Fixed Investment (business investment) and Residential Fixed Investment (real estate, also a subcomponent).

Exhibit 2: Pure Private Sector GDP

Source: US Bureau of Economic Analysis, as of 12/22/2016.

Instead of the sharp uptick, these cleaner categories' growth slowed from 2.7% annualized to 2.1%. We're sorry if that's disappointing, but it is just a fact. What it also shows is Q2 was far better than most people who fixated on the slow 1.4% headline growth rate appreciated. Actually, Q3 2016 was the first quarter in two years in which headline growth was better than pure private sector GDP. Maybe if more folks looked under the hood, they would have realized reality was brighter than feared all along.

Now, as for Q4, the consensus expects headline GDP to slow to the 1.6 - 2.4% range. Maybe that will prove right, maybe not. But whatever they guesstimate, take this lesson to heart: Forgetting to look under the hood can cause your impression of growth to deviate from reality.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

-

Expert Commentary US Jobs, Eurozone Inflation, Private Credit | 3 Things You Need to Know This Week

2026-03-30

2026-03-30 -

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today