Personal Wealth Management / Market Analysis

The Definition of Surprise Power

Because US involvement in Syria is being weighed publicly the world over, it is unlikely to carry enough shock or surprise power to materially affect stocks.

War drums are banging a terrible rhythm—and the growing crescendo now is about Syria. The world over, citizens are concerned. If that’s you, please know you aren’t alone. My heart aches for the Syrian people—for them this is a very real and terrible situation. From an investment point of view, however, should the (seemingly imminent) strike on Syria come to pass, it is unlikely to move markets in a material fashion.

I’ll not rehash any of Elisabeth Dellinger’s excellent analysis of Syria’s limited economic and market impacts. My reasoning is more about how markets function. Markets don’t wait for events to happen before deciding to move—volatility occurs in both directions as investors weigh the probable future outcomes. This efficient mechanism of assigning probabilities is why a strike on Syrian military targets by a “coalition of the willing” is unlikely to be materially negative for equities. Quite simply, a Syrian strike lacks surprise power.

It seems most folks know that last week Syria’s two and half year civil war reached a new point of darkness, as reports of a chemical weapons attack in Damascus surfaced—seemingly, the deadliest chemical strike in over two decades. The United Nations is presently attempting to verify the facts on the ground, but multiple sovereign nations and intelligence agencies already assert without equivocation the attack was conducted by the Syrian government on its own people. The evidence seems to be a phone call US intelligence intercepted in which Syria’s defense ministry demanded an explanation for the strike from a chemical weapons unit official.

What happens next isn’t known with certainty—nothing is. A short-term military campaign is currently being telegraphed to the world as the highest probability scenario. Recall, Barack Obama issued a “red line” warning to Syrian dictator Bashar al-Assad—a chemical weapons strike would carry consequences. He crossed it, it seems, so here we are. Inaction appears to be the lowest probability option. “Bluffing” likely carries negative fallout on the international stage—namely, the message sent to strategically more important, yet equally unsavory nations. The US may decide this outweighs the potential political fallout of a limited military strike or deeper military involvement in the region.

Again, little (if any) of this is news, and that’s exactly my point. Markets are busy reflecting this probable scenario into securities prices in real time. But efficient markets use this widely known information to make highly informed decisions about the impact said events have on future earnings. If a military (or economic event, for that matter) occurs precisely how the consensus expects, there is no new information for the market to reflect— thus, markets don’t have much reason to materially move as a result of the event.

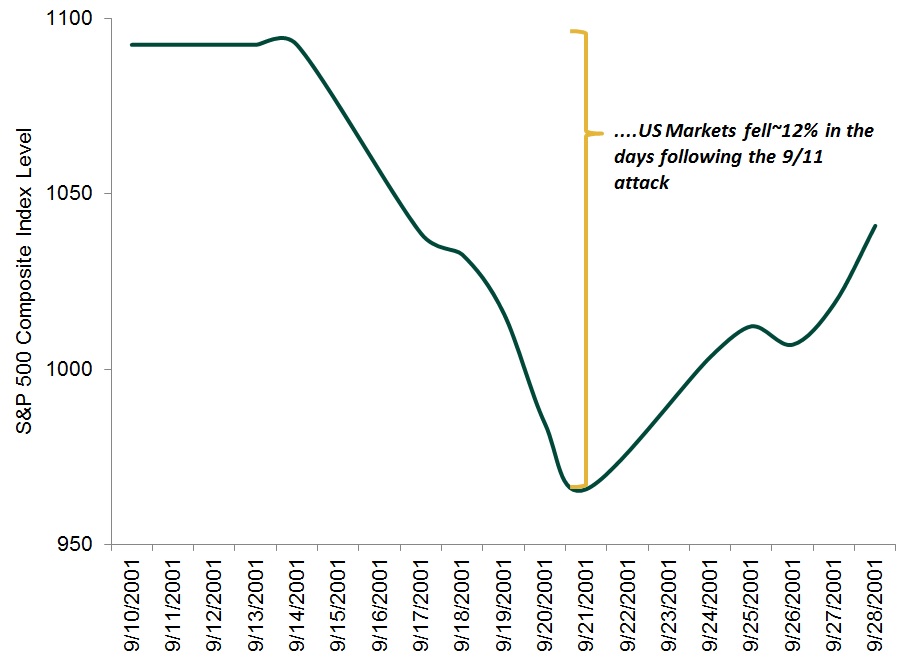

I am not positing Syrian developments won’t create volatility—they likely will. But as time goes on, events in Syria lose surprise power to an even greater degree. Contrast this with the tragedy that occurred on September 11, 2001. That dark day defined surprise power—it changed the world forever. On September 10, we couldn’t possibly imagine what would take place the following day. When markets reopened days after terrorists killed nearly 3000 people, equity markets justifiably reacted with shock and a rather acute sell-off. (Exhibit 1)

Even ignoring that the 9/11-related selloff was short-lived, Syria’s very different because of the surprise power it lacks. Investors don’t need an uncanny ability to predict the specifics over the coming days and weeks. That I’m writing about this unfortunate dilemma and human catastrophe—as the entire world is reflecting—reduces the chances the situation unfolds with enough astonishment to drastically impact markets.

Exhibit 1: S&P 500 Price Index in September, 2001

Source: Standard and Poor’s, Fisher Investments Research. S&P 500 Price Index closing level and returns from 09/10/2001 – 09/28/2001.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Pumping Up the Yen?2026-07-17

-

Expert Commentary This Week in Review | US-Iran Conflict, US Inflation, New UK Prime Minister

2026-07-17

2026-07-17 -

Market Analysis Business Friendly Bureaucracy or No, Britain is Growing2026-07-16

-

Economics Don’t Doubt the Old World2026-07-16

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today