Personal Wealth Management / Behavioral Finance

The Maddening Mr. Market’s Favorite Trick

Stocks' recent upturn isn't abnormal.

The Dow broke 18,000! The S&P 500 topped 2,100! Other round numbers tremble in fear, wondering if they're next! Ok, we made up the last one, but our point remains: Folks have taken notice of stocks' big rebound following mid-February's lows, especially since they crashed through some "psychologically important" barriers.[i] Some wonder if it's a sign of economic stabilization, while others suggest this is a temporary reprieve before a further fall. However, we believe stocks are doing what they typically do during bull markets: rise higher, without any predictable pattern. The market's sharp rebound serves as a keen reminder to investors who thought the bull was stuck or tapped out-stocks can move quickly, both down and up, and staying disciplined and invested is paramount to reaping their long-term gains.

Many have focused on what stocks have done so far this year, especially since the movement has been so dramatic: a clear example of how quickly stocks can rebound. (Exhibits 1-2)

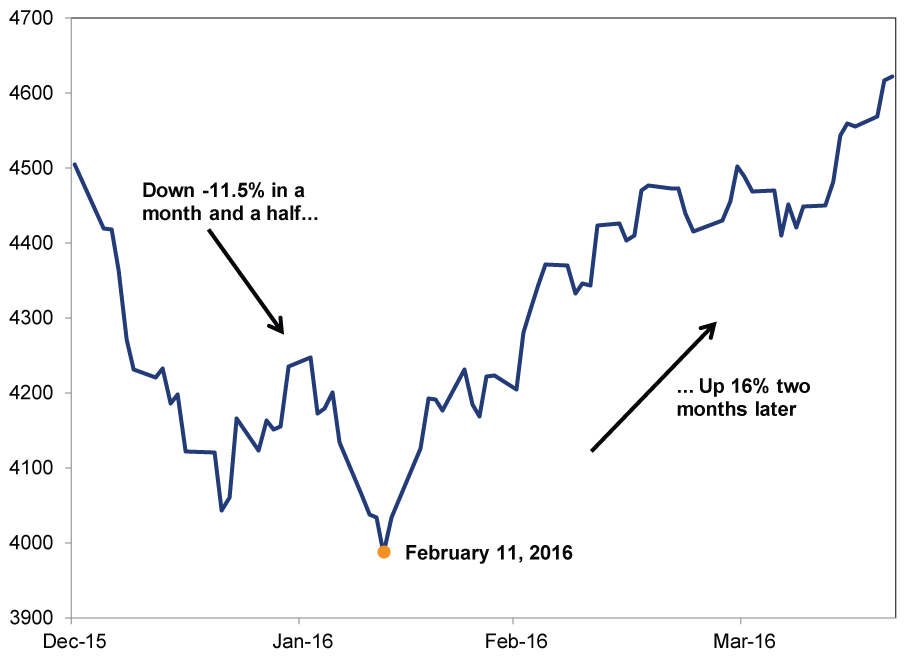

Exhibit 1: MSCI World in 2016

Source: FactSet, as of 4/21/2016. MSCI World Index with net dividends, 12/31/2015 - 4/20/2016.

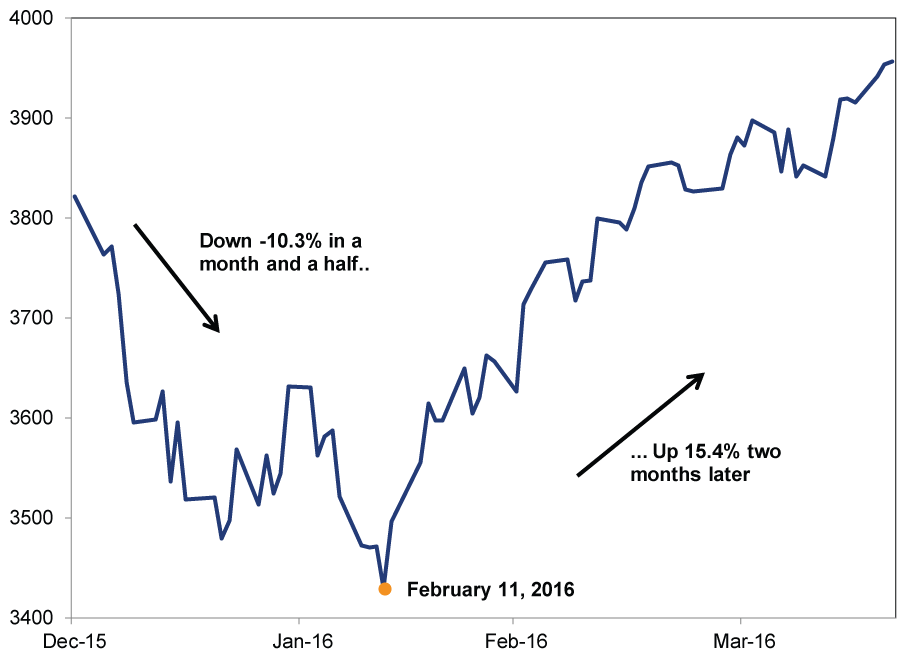

Exhibit 2: S&P 500 in 2016

Source: Global Financial Data, as of 4/21/2016. S&P 500 Total Return Index, 12/31/2015 - 4/20/2016.

The recent surge has pushed the S&P 500 out of its correction (a short, sharp, sentiment-driven decline of -10% or worse), which dated back to its prior high on May 21, 2015. World stocks haven't retraced all lost ground, but they're within shouting distance. The MSCI World is just -4.8% off its 5/21/2015 high, and the strong dollar (which reduces US investors' foreign returns) is partly to blame.[ii] In UK sterling, the MSCI World is a mere -1.1% off its 4/10/2015 high.[iii] But any way you slice it, most major indexes globally are at or near their prior peaks, and we believe it is only a matter of time before global equities are higher overall.

This recovery highlights the positive volatility stocks frequently experience during bull markets. It is also quite normal, as volatility cuts both ways. But on the heels of a lengthy correction, it's all too easy to forget fast moves are frequent. Some pundits thus argue sentiment is currently out of whack, driving stocks higher than warranted, and it's only a matter of time before the pullback returns. Yet to us, it looks like a typical correction rebound. Stocks frequently fall fast during corrections, but they often recover just as quickly. In the 48 trading days following February 11, the S&P 500 is up 15.4%.[iv] Consider what stocks did over the same timeframe following past corrections. In 1998, after the S&P plunged -19.1% and bottomed on August 31, the index was 18.8% higher 48 trading sessions later. Similarly, the S&P jumped 18.3% after a correction of -14.2% ended on March 11, 2003. And in 2010, the S&P clawed back 8.4% after a -15.2% midyear correction bottomed on July 2. And 48 days after the 2012 correction's June low, it was up 10.2%. Now, it is a hair premature to declare this correction over, given global stocks haven't eclipsed their pre-correction high. But reviewing that history shows this bounceback is pretty typical of correction rebounds.

As great as this rebound has been, we caution investors from presuming stocks hitting (or not hitting) certain index levels means anything-it doesn't. Despite all the headline attention, numbers like 18,000 or 2,100 are nothing but trivia to stocks. They reflect a given index's particular, arbitrary calculations as well as its past movement-not what's to come.

Alternatively, with returns flattish over the past 18 months, some suggest the bull market is out of juice after seven years. However, this commits the same type of error: presuming recent past performance means either lower, limited future returns or the bull is about to end. But that isn't how markets work. For one, bulls die in one of two ways: They run out of steam as euphoric expectations outpace reality-not the case today, given how dour investor sentiment is toward an underappreciated global economy. Or, alternatively, a big, widely unnoticed negative wallops markets. We see nothing fitting that bill right now. Today, plenty of drivers economically and politically support more bull market. Solid growth in both the developed and emerging world. Gridlocked governments in most developed economies, preventing disruptive legislative change. The fundamental backdrop is positive, and with sentiment currently dour, we'd anticipate reality positively surprising most investors. The degree to which sentiment swings up based on that pleasant surprise remains to be seen-and is likely the determining factor in the magnitude of returns this year.

But for investors to enjoy those gains, they must remain in the market-easier said than done, particularly since stocks don't give an "all-clear" signal once they're done falling. After a big, quick rebound, we understand why some folks might even be upset stocks are higher : It can be incredibly frustrating to watch markets soar past you if you got out. During times like this, we remind investors to keep their investment goals in mind. If you require long-term growth, you'll likely need to own stocks. The price to pay for that growth is the maddening short-term volatility that accompanies equity markets-just when you think stocks will do one thing, they do another. This is a constant battle investors must fight, but by training themselves to focus on the bigger picture and filter out short-term noise, they can put themselves in a better position to benefit from those returns.

[i] The scare quotes are your signal that those don't exist. No index level is psychologically important to the point of impacting market movement.

[ii] Source: FactSet, as of 4/21/2016. From 5/21/2015 - 4/20/2016.

[iii] Ibid. From 4/10/2015 - 4/20/2016. Returns in Canadian dollars show just how loony currency skew can be. In CAD, the MSCI World recovered from its September pullback by the end of 2015, hit a new all-time high, then entered a correction. It is clawing back now, but still down -7.4% (per FactSet) from that peak.

[iv] The source for this figure and the others in the rest of this paragraph: Global Financial Data, as of 4/21/2016.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary US Inflation, Fed Minutes, Consumer Sentiment | 3 Things You Need to Know This Week

2026-04-06

2026-04-06 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 30 - April 32026-04-06

-

Expert Commentary This Week in Review | Q1 Recap, Earnings Guidance, Elections

2026-04-03

2026-04-03 -

Market Analysis A Forward-Looking Lesson One Year After Liberation Day2026-04-02

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today