Personal Wealth Management / Market Analysis

A Discussion on Consumer Credit Trends

The US consumer is in better shape than many believe.

It’s been a challenging few years for US consumers: A housing bear market, an equity bear market, a credit panic, a recession, political turmoil and tight-fisted banks. And with some slowness in recent personal consumption data, many fear consumers still aren’t in great shape. Yet recent data suggests that’s not the case.

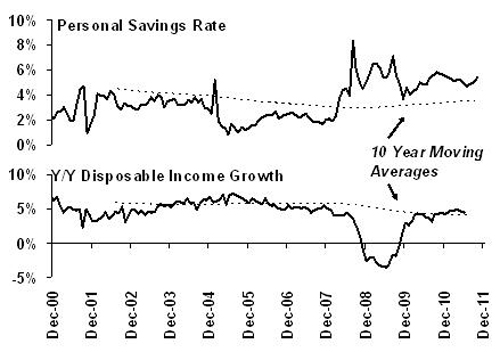

Despite the stubbornly high unemployment rate and contrary to what many would think, personal savings and income are growing (Exhibit 1). Today’s savings rate of over 5% is well above average, causing the consumer’s aggregate balance sheet to improve every payday—today’s household cash balance of $8 trillion is nearly 30% higher than just five years ago. Opting to save cash may have weighed on spending, but looking forward consumers appear well-positioned.* Moreover, annual disposable income growth—nearly 4%—is trending right around its ten-year moving average.

Exhibit 1: US Personal Savings Rate and Disposable Income

Source: Thomson Reuters as of 08/2011

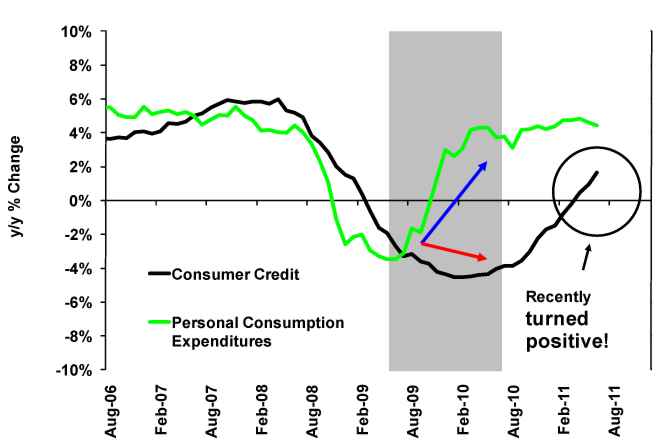

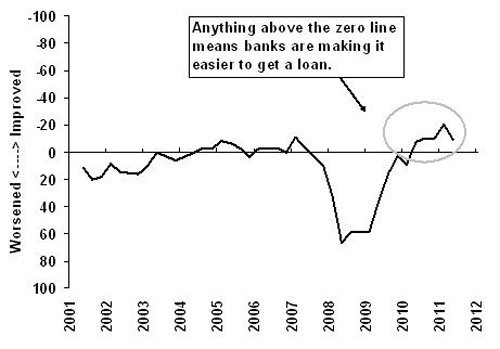

Consumer credit and consumption have a pretty strong relationship over time, but after 2008’s financial panic the connection broke. Though consumption rebounded fairly quickly (personal consumption is at an all-time high), borrowing remained pressured as consumers and lenders deleveraged their balance sheets. Now, banks are resuming lending, and consumers are less debt-averse, hence consumer credit growth has re-emerged (see Exhibit 2)—and credit is becoming readily available to fund future spending (Exhibit 3 illustrates several quarters of increased willingness to lend).

Exhibit 2: US Personal Consumption and Consumer Credit Annual Growth

Source: Thomson Reuters

Exhibit 3: Senior Loan Officer Lending Survey: Consumer Underwriting Trends

Source: Federal Reserve

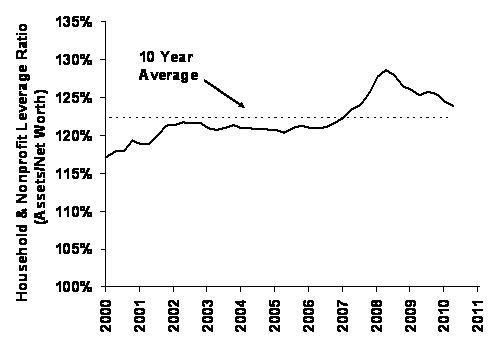

Also helping consumers, perplexing as this may be, is the surge in foreclosures. Though we realize foreclosure is difficult for those going through it, it’s important to understand foreclosing can help personal balance sheets, as it reduces aggregate consumer leverage and improves aggregate cash flow. Strategic defaults (encouraged by the Mortgage Forgiveness Debt Relief Act (MFDRA) of 2007, which made certain debt forgiveness a non-taxable event) are a way to instantaneously improve aggregate consumers’ financial situations. In fact, banks have “forgiven” more than $500 billion since 2007, mostly tied to residential loans (the MFDRA of 2007 saved consumers nearly $200 billion in income tax alone).**

Exhibit 4: US Household & Non-Profit Leverage Ratio

Source: Federal Reserve 08/2011

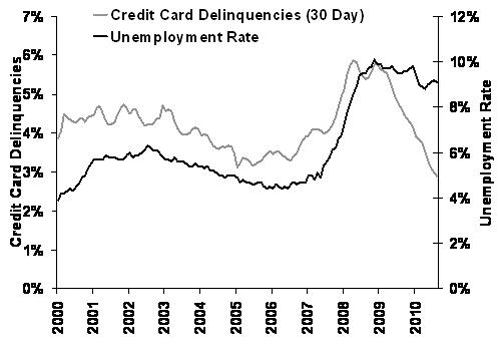

And here’s one more sign consumers are doing better: Two years after the recession’s end, consumer delinquencies are at the lowest level since before 2000. Measured by compiling data from six major credit card trusts, 30-day delinquencies as a percentage of total loans fell to just 2.9% in July 2011.***

Exhibit 5: US Credit Card Delinquencies

Source: Bloomberg 08/2011

With lower aggregate leverage, higher cash balances, positive income trends and resurgent lending, in our view consumers don’t appear down for the count. Moreover, with Personal Consumption Expenditures accounting for about 70% of US economic activity, a stronger consumer could help propel domestic demand into 2012.

* Federal Reserve, BEA

** FDIC

*** Bloomberg

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today