Personal Wealth Management / Market Analysis

A Friday Fact-Check for a Tuesday

Before making investment decisions, evaluating articles’ claims and use of data is key.

This week, we noticed some, um, quirky claims in the financial press. Innocuous sentences that cited data and didn’t seem to say anything too outlandish. Yet the numbers, in many cases, didn’t do or mean what the rest of the sentence said they did. Most readers probably just blew right through them. But we, being professional nitpickers, did no such thing. These data had some problems we think people should consider. Not to play “Gotcha” with the financial punditry, but to show investors the importance of evaluating everything they read—even seemingly fact-driven sentences—before making investment decisions.

Our first example is the one that kicked off this whole idea. It comes from Tuesday’s Wall Street Journal, in an article warning that stocks’ early 2019 rally is on thinner ice than past rallies because fewer companies are joining the rush to new heights (a claim best discussed another time). Lurking within it was this observation: “Technology shares in the S&P 500 have surged 26% this year, helped by shares of FANG companies—Facebook Inc., Amazon.com Inc., Netflix Inc. and Google parent Alphabet Inc.—coming back into favor.”[i]

The number here is correct. Through Monday’s close, the S&P 500 Information Technology sector price index was up 26.09% year to date, which rounds to 26%.[ii] Problem is, none of the FANG companies are in this sector. It is easy to think of them as Tech, because they are Internet-based and some are well-known “disruptors,” a term often associated with Tech. Alphabet and Facebook even used to be Tech. But then came a late-2018 sector reshuffling, which flipped them into the new Communication Services sector as Interactive Media & Services companies. Netflix also lives in Communication Services, in the media industry. Amazon, meanwhile, hangs out over in Consumer Discretionary like any good little retailer would.

The problem with this error is that it could lead to weird moves if taken at face value. One concerned about frothy Tech might indiscriminately dump non-Tech companies. One trying to capture FANG performance may buy an S&P 500 Tech ETF thinking they are getting those famous four firms, only to discover too late they went 0-for-4. So before you act on information, make sure the information is actually valid.

Here is another brief example:

Is this the tech bubble part two? It’s fair to ask, given how big [the Nasdaq 100] is getting versus the rest of the market. At about 36 percent of the S&P 500, it’s creeping up on 1999-style dominance.[iii]

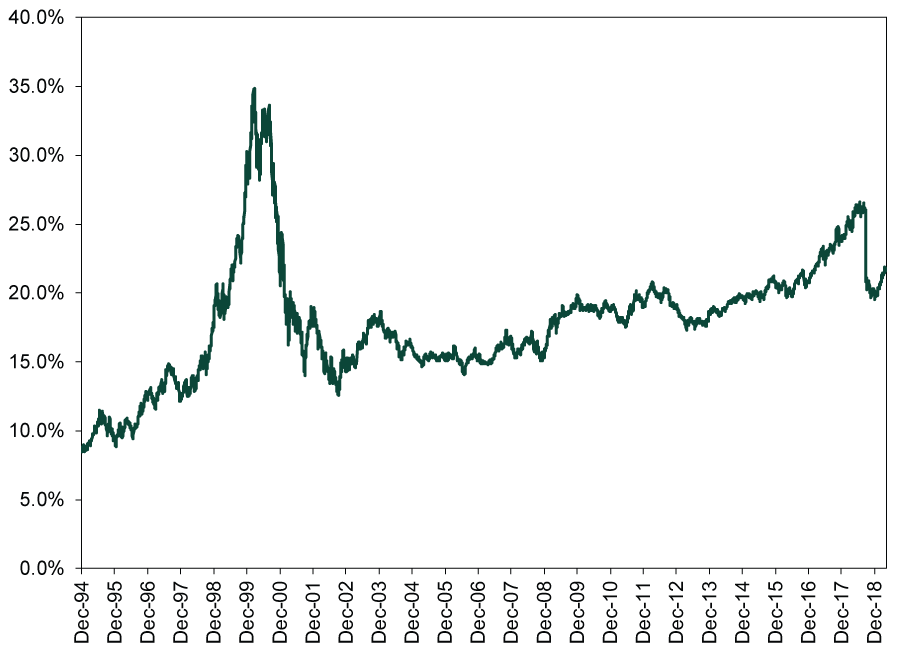

Well yes, Nasdaq 100 market cap is 35.94% of S&P 500 market cap, rendering that sentence technically truthy.[iv] Only problem: Just 37 of the Nasdaq 100’s components are in the Information Technology sector.[v] Of the rest, 17 are Communication Services, another 17 are Consumer Discretionary, 6 are Consumer Staples, Financials and Utilities have 1 each, 16 are Health Care and 8 are Industrials. The S&P 500, meanwhile, has 68 Tech companies, 32 of which are also in the Nasdaq 100—and 36 that aren’t, including some really big names that rhyme with words like Shoelett Smackard, Floracle, Fleagate and Bred Chat. Thus, logic would seem to dictate that the correct metric to weigh here is Information Technology’s weighting in the S&P 500. Presently, it is 21.6%, quite far below its Tech Bubble peak, 34.9%.[vi] Its rate of increase is also far milder than when the Tech Bubble inflated, as Exhibit 1 shows. Viewed this way, Tech’s recent rise doesn’t seem bubblicious. (A conclusion the article agreed with in the end, as it happens.)

Exhibit 1: Tech as a Percentage of S&P 500 Market Cap

Source: FactSet, as of 5/7/2019. S&P 500 and S&P 500 Information Technology market capitalization, 12/31/1994 – 5/6/2019.

Our final case study comes from The New York Times, but we feel bad saying that because this is an error pretty much every mainstream financial commentary has made at some point, and this snippet gets a nod here solely because it was the latest instance.

The central bank [the Fed] aims for 2 percent inflation, a level that’s low enough for consumer comfort but high enough to guard against economy-damaging price declines. The Fed has struggled for years to hit that target. Price increases excluding volatile food and fuel came in at just 1.6 percent for the year through March, and consumer expectations for inflation have been hovering at low levels.[vii]

Once again, all the numbers here are correct. The Fed targets a 2% annual inflation rate, and the year-over-year inflation rate of the Personal Consumption Expenditures (PCE) price index excluding food and energy was indeed 1.6% in March. Buuuuuuuuuuuut, “core” PCE is not the Fed’s target.[viii] Rather, the Fed targets 2% annual inflation in the headline PCE, which includes food and fuel. Take it from St. Louis Fed President James Bullard, who said, “The FOMC will target the headline inflation rate as opposed to any other measure (e.g., core inflation, which excludes food and energy prices) because it makes sense to focus on the prices that U.S. households actually have to pay.”[ix] That was seven years ago.

Headline PCE clocked in even slower in March, at 1.5%.[x] That further proves the article’s point, which centered on the Fed’s repeated failure to reach its target since establishing said target in 2012, highlighting central bankers’ inability to fine-tune the economy simply by pulling interest rate levers. But it would strengthen the piece if the Fed’s target were correctly articulated.

[i] “Stocks’ Latest Rally Isn’t as Broad as Other Recent Climbs,” Jessica Menton, The Wall Street Journal, May 5, 2019. https://www.wsj.com/articles/stocks-latest-rally-isnt-as-broad-as-other-recent-climbs-11557230401

[ii] Source: FactSet, as of 5/7/2019.

[iii] “If This Is a Tech Bubble in Stocks, It’s the Expansionary Phase,” Lu Wang and Jeran Wittenstein, Bloomberg, May 3, 2019. https://www.bloomberg.com/news/articles/2019-05-03/if-this-is-a-tech-bubble-in-stocks-it-s-the-expansionary-phase

[iv] See Note ii.

[v] Ibid.

[vi] Ibid.

[vii] “Fed Leaders Try to Talk Up Inflation Without Stoking Rate Cut Expectations,” Jeanna Smialek, The New York Times, May 3, 2019. https://www.nytimes.com/2019/05/03/business/economy/federal-reserve-inflation-interest-rates.html

[viii] Source: BEA, as of 5/7/2019.

[ix] “President’s Message: Recent Actions Increase the Fed’s Transparency,” James Bullard, The Regional Economist, April 2012. https://www.stlouisfed.org/~/media/files/pdfs/publications/pub_assets/pdf/re/2012/b/pres_mes.pdf

[x] Ibid.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today