Personal Wealth Management / Market Analysis

A Post-Fed Look at Yield Curves in America and Beyond

Unnoticed by most folks, things have improved a bit.

This is not an article about the Fed rate cut. It is not about the fed-funds target range dropping by 25 basis points to 1.75% - 2.0%. It is not about the supposed “split” among policymakers, three of whom dissented from the decision (two voting for no change, one for a bigger cut). It is not about the “dot plot” of Fed people’s forecasts, which allegedly showed some divergent thinking. It is not about pundits’ claims that this was a “hawkish cut,” whatever that even means. Rather, it is a brief commentary on the yield curve. No one seems to notice, but it has improved over the past three weeks. So have international yield curves. Shall we have a look?

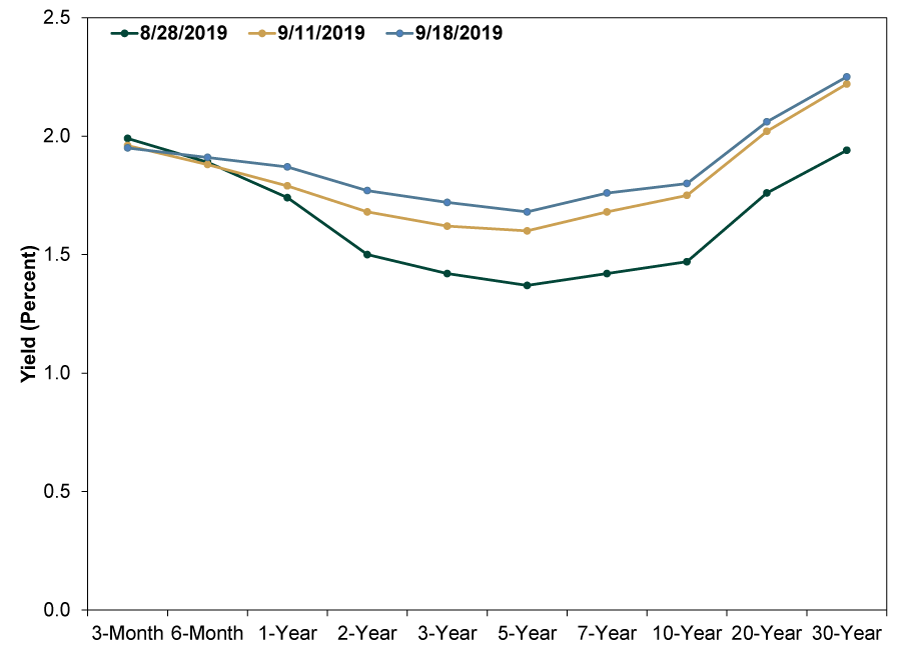

Exhibit 1 shows the US’s yield curve on August 28—when the gap between the 3-month and 10-year yields was at its most negative this year—as well as one week ago and today. Short rates fell a smidge during this span, while long rates inched higher. We aren’t about to argue past narrowing predicts future narrowing, but the past few weeks do hint at investor sentiment. Markets discount all widely known events, including widely expected Fed rate cuts. So it seems logical to assume markets have spent the past couple weeks pricing in today’s move. That long rates rose despite expectations for a rate cut is a hint investors might be moving past the summer’s deep pessimism.

Exhibit 1: The US’s Quietly Improving Yield Curve

Source: FactSet, as of 9/18/2019. Benchmark government bond yields on 8/28/2019, 9/11/2019 and 9/18/2019.

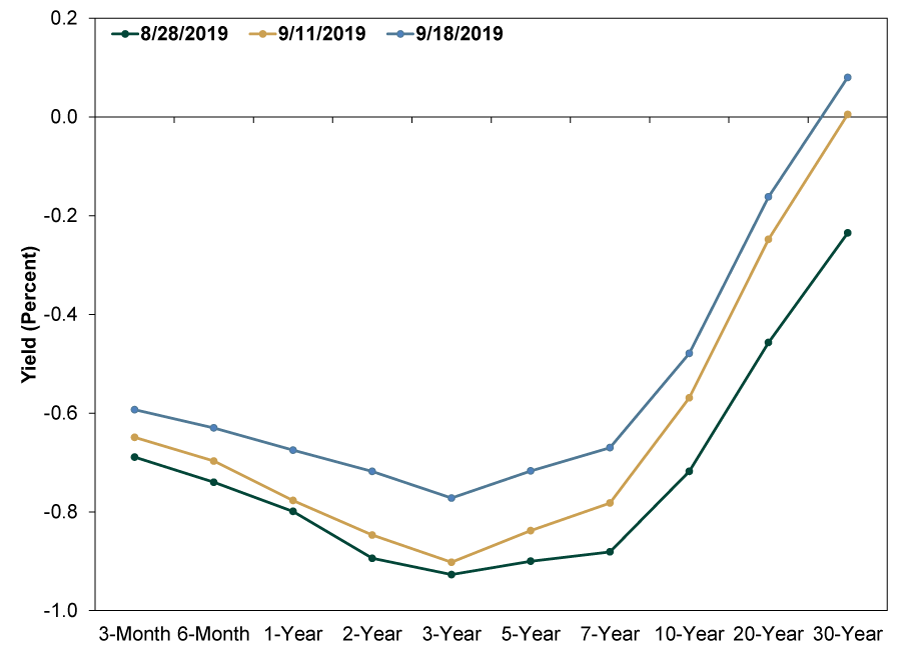

Germany is another interesting case. There, too, long rates have risen over the past three weeks. 30-year yields have finally turned positive. This, despite the ECB announcing a week ago that it would restart long-term bond purchases. Short and long rates each defied central bankers, rising after the announcement of a tiny rate cut and the resumption of quantitative easing (QE). As a result, the yield curve is no longer inverted. Other eurozone yield curves have evolved similarly.

Exhibit 2: Germany’s Quietly Improving Yield Curve

Source: FactSet, as of 9/18/2019. Benchmark government bond yields on 8/28/2019, 9/11/2019 and 9/18/2019.

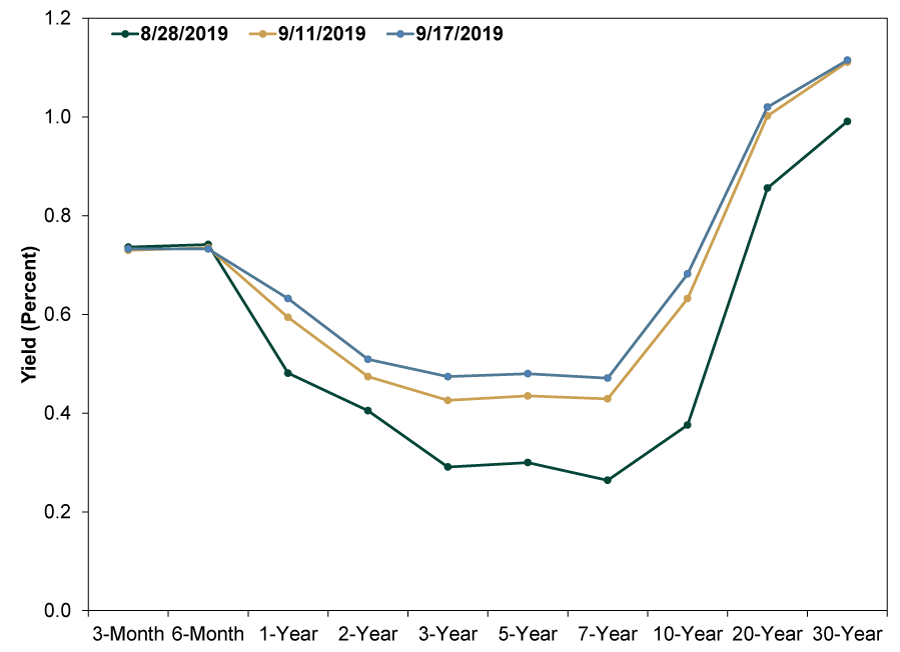

Same song, third verse in the UK, where the gap between 3-month and 10-year yields narrowed from -36 basis points on August 28 to just -5 basis points on Tuesday (as we write, Wednesday’s closing short-term yields aren’t yet available).

Exhibit 3: The UK’s Quietly Improving Yield Curve

Source: FactSet, as of 9/18/2019. Benchmark government bond yields on 8/28/2019, 9/11/2019 and 9/17/2019.

As a result of these improvements—plus some funky wobbles in Japan’s funky yield curve—the global yield curve has morphed from slightly inverted three weeks ago to slightly positive. Functionally, there isn’t a meaningful difference between slight inversion and slight steepness—both round to flat. Plus, the aggregate yield spread is arguably less significant than whether there is enough divergence among countries for banks to be able to borrow in one and lend in another for a tidy profit. This interest rate arbitrage persevered even as the global curve inverted, thanks to negative rates in Europe and Japan and America’s relatively higher long rates. So we think this year’s fears over inverted yield curves were false from the get-go. But inversions did weigh on investor sentiment. Should they continue reverting to positively sloped, it wouldn’t surprise us if sentiment improved further and this bull market’s animal spirits began stirring again.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-17

-

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today