Personal Wealth Management / Market Analysis

A Prime Way to View the Latest Jobs Numbers

What labor force participation rates do-and don't-tell investors.

As August gets going and parents count down the days before school begins, financial media are doing a little cheering of their own about Friday's "banner jobs report." Specifically, nonfarm employers added 209,000 jobs in July and the unemployment rate dropped to 4.3%. Many analysts banged on about the political implications of the latest jobs numbers, but we aren't focused on that here. Rather, we found a less-heralded stat-the prime-age labor force participation rate-more interesting because its trend highlights how sentiment remains below reality, evidence investors&rsqu o; optimism isn't universal (never mind euphoric).

The unemployment rate makes most headlines, but the BLS has dozens of ways to measure US labor markets. One prominent gauge is the labor force participation rate: the percentage of the civilian population, 16 years and older, that is working or actively looking for work. The "prime-age" rate-which focuses on the 25-54 age group[i]-hit 81.8% in July, the highest since December 2010.

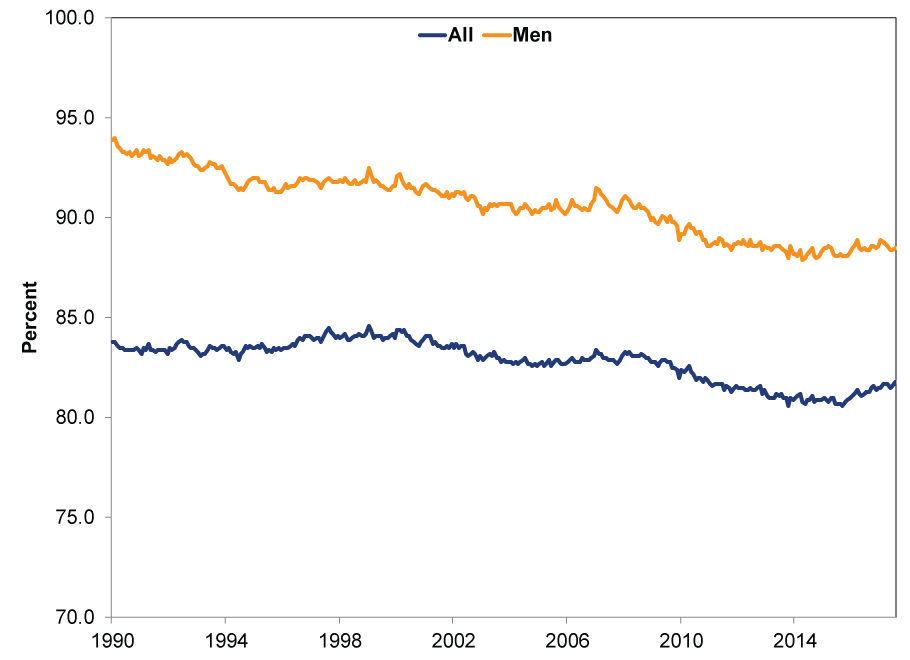

Policymakers often cite this rate when discussing employment trends, and they commonly squawk about its long-term decline. The Obama White House wrote a 47-page paper about falling prime-age males' labor force participation, and the issue also arose during the 2016 presidential election. More recently, Fed chair Janet Yellen mentioned the falling labor participation rate in broader remarks to Congress about the opioid crisis. Based on the general tone, you might think the workforce has been in perpetual decline. However, the data tell a different story as the slide seemingly stopped about two years ago. (Exhibit 1) While the prime-age men's participation rate has been flat to up a teensy bit over that period, the total participation rate is clearly trending higher.

Exhibit 1: Prime-Age Labor Force Participation Rates Since 1990

Source: Bureau of Labor Statistics, as of 8/7/2017. Labor Force Participation Rate (25-54 yrs., Men) and Labor Force Participation Rate (25-54, yrs., All), from January 1990 - July 2017.

Much of the concern over labor force participation's long-term decline is sociological-as far as markets are concerned, this generally isn't an economic issue. Most of the potential causes are sociological, too-and largely related to demographics. For instance, some workers may be retiring earlier, which would weigh on the participation rate. Similarly, younger people may be spending more time in school-for a bachelor's or advanced degree-before joining the workforce and ultimately increasing their long-term earnings power. These developments are meaningful and affect people's lives, but they have limited market impact-sociology doesn't drive stock returns.

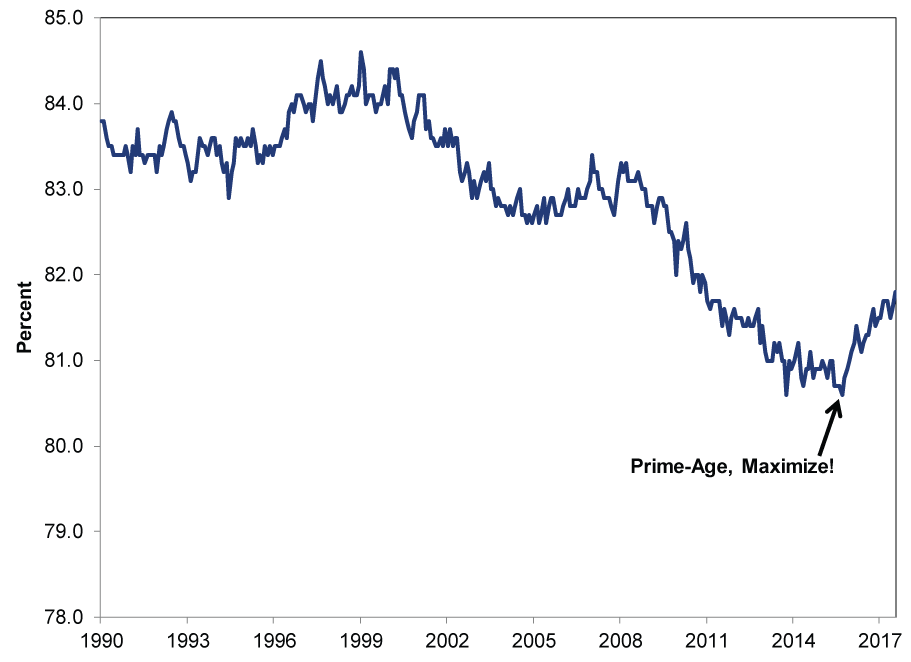

Our interest lies more with the way pundits discuss the participation rate, as if it is still sliding. While the prime-age rate is lower today than it was 10 and 20 years ago, it isn't fair to call it "falling." Since bottoming at 80.6% in September 2015, it has risen 1.2 percentage points. A two-year rise looks to us like a widely overlooked nascent bounce. (Exhibit 2)

Exhibit 2: The US's Prime Age Has Been Improving

Source: Bureau of Labor Statistics, as of 8/7/2017. Labor Force Participation Rate (25-54, yrs., All), from January 1990 - July 2017.

Changing demographics playing a big role here, too. As the fine folks at the Atlanta Fed noted in a piece titled Behind the Increase in Prime-Age Labor Force Participation:

It turns out that most of the increase in the prime-age LFPR [labor force participation rate] has been because of increased LFPR within demographic groups-in particular, prime-age women and especially women without a college degree. Prime-age men have not contributed much to the rise in participation beyond the increased participation associated with a more educated population.

In particular, the largest contribution from changes in behavior among prime-age women over the last year came from a decrease in the propensity to be out of the labor force because of poor health or being in the shadow labor force (wanting a job but not looking).

This, too, is sociological. Interesting! But not the sort of thing that impacts stocks. Yet people's reactions to and opinions about labor force participation reveal a lot about sentiment. The sociological implications of the long-term decline in male labor force participation have given folks a rather cloudy view of labor markets. When payrolls jump as they did in July, broad reactions are full of "yah, buts." "Yah, but it's all low-paying restaurant jobs." A few years ago, it was, "yah, but it's mostly part-time work." Or, or, or. What they broadly miss is that the growing US economy is gradually pulling more people back to work and into the labor force-typical during a maturing expansion. Employment data are late-lagging, but this is a prime example of how sentiment continues undershooting reality.

Lingering labor market skepticism is a sign stocks still have more Wall of Worry to climb. If investors were universally optimistic, labor force participation's long decline probably wouldn't continue making headlines. It would be a footnote, with more focus on the positives. People would likely be shouting from the rooftops about "full employment," instead of dwelling on those left behind and worrying about lack of opportunities. That labor market data still inspire concern despite their nascent improvement is a sign markets aren't anywhere near euphoric, contrary to pundits' occasional claims.

[i] What the BLS considers as workers' most productive age range.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27 -

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

-

Politics This Week in Gridlock: Europe Edition2026-03-26

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today