Personal Wealth Management / Market Analysis

A Stock Market Correction Is Never “Due”

Corrections do not operate on schedules, so they are never "due" or "overdue."

Welp, looks like volatility is back! While US markets are bobbing around all-time highs, eurozone stocks are down -6.5% since April 13.[i] In euro, that is. Eurozone bond yields popped up, too, with German 10-year yields jumping from 0.08% on April 20 to 0.52% on May 5-and most other nations following suit. Absent a clear fundamental reason for the slide, some are saying eurozone stocks and bonds were just "due" for a pullback given their rapid rise in recent months. We've seen similar statements about US stocks, too, and sorry but we just don't buy it. While markets never move in a straight line, there is no "due" when it comes to corrections.

Though corrections (quick, steep, sentiment-based drops between -10% and -20% or so) happen about once a year on average during bull markets, they don't follow schedules. Nor does a given magnitude of near-uninterrupted rises require stocks to pull back. If this were true, US stocks probably would have corrected shortly after 2013's 32.4% rise-they didn't.[ii]

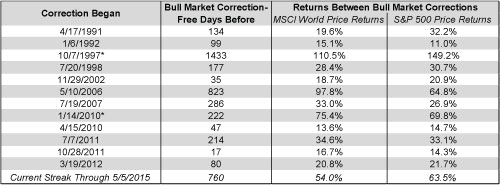

Corrections define random. This bull market, so far, had two in 2010, two in 2011, one in 2012-and nada since. The 1990s bull had its first begin on 4/17/1991-six and a half months after the bull began. That one ran through 8/12/1991, and the next began mere months later on 1/6/1992. Correction number two ended on 4/8/1992, and five years passed until the next, which ran from 10/7/1997 to 11/12/1997.[iii] That bull's final correction came in 1998, when stocks fell between 7/20/1998 and 10/5/1998.

This inconsistent frequency was by no means an anomaly of this bull or the 1990s. The 2002-2007 bull market first corrected on 11/29/2002, less than two months after the bear market ended. That pullback ended in March 2003, and stocks didn't correct again until 5/10/2006. The final correction ran from 7/19/2007 to 8/16/2007, ending less than two months before the bull market did. And some bulls, like the one from October 1987 to January 1990, had zero corrections. Again, random, making the time elapsed since the last correction an odd reason to assume one must lurk. A correction doesn't become more or less likely because a certain amount of time passed since the last-one could always strike at any time, without warning.

Since the 1990s bull began, global stocks have risen for as few as 17 days between corrections and as many as 1,433 days. As for magnitude, the range of returns between bull market corrections shows similar wide spread: As small as 13.6% to 110.5% for global stocks, and 11.0% to 149.2% for US stocks. Where is the pattern here? Where is the schedule? What is the recipe? There isn't one-and that is the nature of this unpredictable beast. Here is a table, which we've titled "Corrections Define Randomness," because they do.

Exhibit 1: Corrections Define Randomness

Source: Factset, MSCI World and S&P 500 Price Returns, 10/11/1990 - 5/5/2015. *The 10/7/1997 and 1/14/2010 corrections reached 9.7% and 9.6%, respectively, but both round to 10%, and we are being generous to those who think a correction is "overdue" and citing them. Dating is based on the MSCI World Price Index.

All of this "stocks are due" mumbo jumbo suffers the same basic fallacy: It assumes past performance predicts future returns. But this isn't true. Stocks are forward-looking, and past returns don't write the future. Pardon the tautology, but the future writes the future.

This would all be academic if investors weren't so easily swayed into acting on warnings like "stocks are due." Some act out of fear; others out of the belief they can time both ends, buying back in lower later. Regardless of the motivation, recent history shows the danger. We saw the same "we're due" warnings last year and the year before. Had you followed their advice, and remained out of stocks since then waiting for the correction, you would have missed some pretty handy growth-a big opportunity cost. Stocks' average annualized return during bull markets is about 21%, including all corrections and pullbacks. If your goal is to grow your portfolio over time, you don't need to avoid corrections. But capturing bull market upside is a must.

Not that we're pure buy-and-hold advocates, of course. If you have strong evidence a bear market is forming, making stocks likely to fall 20% or more over a longer stretch, then it can make sense to sit out for a while. Bear markets have identifiable fundamental causes, making them possible, although extremely difficult, to forecast. Corrections come out of nowhere, are driven purely by sentiment and end as suddenly as they begin, making timing them a fool's errand. Success would require perfect precision at the top and bottom to come out ahead. Nailing it at the top is only half the battle-buying at the bottom requires buying when everyone else is ready to capitulate. Sounds easy on paper, but in practice, it's exceedingly difficult. We aren't aware of anyone who has timed corrections repeatedly-if they had, they'd be a living legend.[iv]

So here is the simple truth: Corrections can happen any time, for any reason-or no reason! They're uncomfortable, but enduring them is the price we pay for bull markets' great returns. Our advice: Accept the tradeoff, and stay cool whenever the next correction arrives.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] FactSet, as of 5/6/2015. MSCI European Economic and Monetary Union Index returns with net dividends, 4/13/2015 - 5/5/2015.

[ii] FactSet, as of 4/7/2015. S&P 500 Total Return Index, 12/31/2012 - 12/31/2013.

[iii] The drop was 9.6%, which rounds up to 10%.

[iv] Not even Warren Buffett, who is fond of saying he never sells.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-17

-

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 9 - March 132026-03-16

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today