Personal Wealth Management / Market Analysis

A Stock Selection Lesson in Red Flag Avoidance

A firm's heavy reliance on government money is a red flag, especially in an election year.

(Editor's Note: MarketMinder does NOT recommend individual securities; companies referenced herein are merely cited as examples of a broader theme we wish to highlight.)

In selecting securities, very often the name of the game isn't so much to find the glitziest firm you can, but rather, to avoid those with identifiable red flags. For some, it's what they are excluding in presenting non-GAAP earnings.[i] For still others, it's outstanding legal actions or confusing business structures. But one timely red flag, particularly in an election year: a firm that relies heavily on government policy for its sustainability.

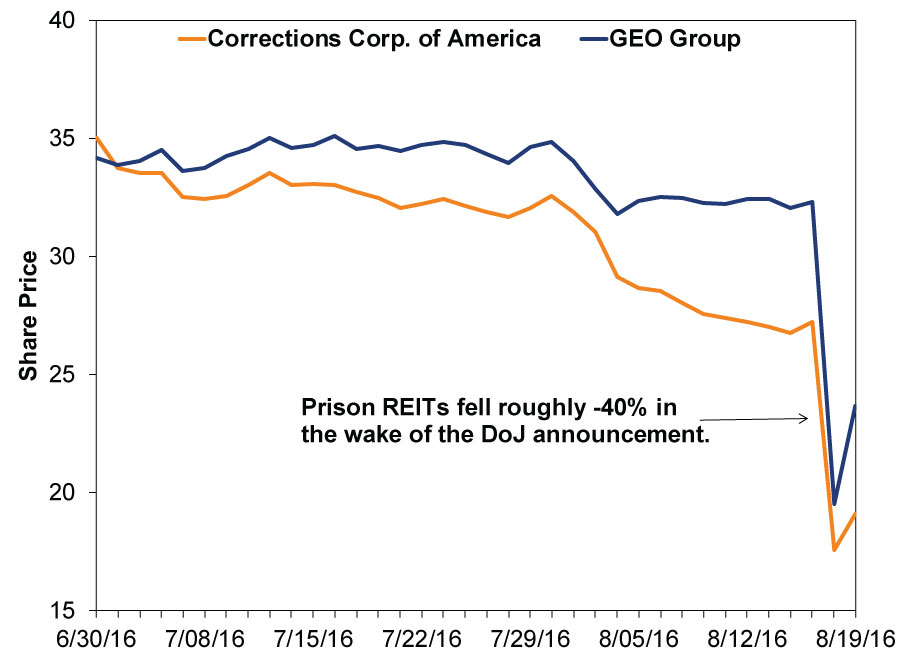

Thursday, investors in two Real Estate Investment Trusts (REITs) were taught this lesson rather harshly, after the US Department of Justice (DoJ) announced it would cease using private prisons to house federal inmates over the next few years. From a market-wide perspective, this announcement has the weight of a butterfly. Even from a sociological or political one it isn't huge: Only about 11% of federal inmates (~22,100 people) are housed at privately run facilities. But for Corrections Corporation of America and GEO Group, it is much larger.

To be sure, these two firms are not exclusively (or even primarily) reliant on the federal government for business-they run state and local facilities, as well as prisons abroad. But many see the feds' move as a precursor to other potential actions. You see, the DoJ's inspector general conducted a study of private prisons compared to government-run facilities. The DoJ interpreted the study's findings as showing private prisons didn't offer much cost benefit, were more dangerous (to inmates and employees) and overall lower quality, concluding that institutions run by the Federal Bureau of Prisons are a better option. Now, the private prison companies disagree, and note that the study essentially compared apples and oranges. You can draw your own conclusion about all of that-our interest is different. If state and international authorities decide to follow the DoJ's lead, it would spell trouble for private-prison shareholders.

If you decide to purchase shares of a REIT that deals exclusively in prisons, you are buying something that is pretty directly confined[ii] to a government policy. If that policy changes or shifts-even when it isn't the biggest deal in the world-the business could be adversely affected. Due to this seemingly small change, the two prison REITs noted fell massively, before rebounding somewhat Friday.

Exhibit 1: Private Prison REITs

Source: FactSet, as of 8/19/2016. 6/30/2016 - 8/19/2016.

All this would be an interesting curiosity with little to no takeaway for investors-after all, the cumulative market cap of the two publicly traded prison REITs before the DoJ's -40% haircut was only about $5 billion.[iii] But the issue of being held captive[iv] by government policy isn't unique to prison REIT shareholders.

Many other firms share this issue. Take, for example, solar and wind power. Even some customers-to say nothing of shareholders-are at risk of government policy change. Consider the issue of rooftop solar panel installation. Many governments from places as far-flung as California and Spain offered benefits to encourage homeowners to install panels-and firms in the field marketed based on those programs. However, when push has come to shove in each, policy revisions severely hurt firms and consumers.

In many states, officials subsidize the installation of rooftop solar panels through a system called net metering. Net metering offers credits to owners of solar panels for power they didn't use and fed back to the power grid-credits they can use to reduce their power bills, sometimes significantly. However, this doesn't take into account the fact solar panels are an intermittent generation source-they don't run consistently at all times of day. When the sun is shining, solar panel owners frequently feed power back into the grid. But that isn't necessarily the peak consumption time-night is. And when solar panel owners consume power at night, they are drawing off the grid, but at subsidized rates based on the power they fed back to the grid at non-peak hours-which has become a thorny political issue.

Hawaii and Nevada curtailed credits in 2015, greatly imperiling the cost/benefit of installation. In California, utility regulators elected to continue the practice-but radically altered the rate schedule, greatly mitigating the financial benefit. The same situation, on a broader scale including renewable energy power plants, hit Spain as part of its budget-cutting push in 2012.

For investors in solar and wind firms, such policy shifts could imperil the firms they eye. Simply, few firms in this space are truly cost-competitive with fossil fuels absent government subsidies, both to consumers and the firms. This is even more true today than four years ago, considering fossil fuel prices' decline. After all, alternatives like solar and wind are designed to replace oil and gas. Their high cost relative to fossil fuel power has always been a headwind to greater adoption and use. With oil prices today less than half their 2014 levels, solar and wind's cost competitiveness is reduced even further, making them more reliant on subsidy, a risk in any year-but particularly an election year, after which policy could shift.

There are some industries where government involvement is unavoidable (Defense, for example). And, of course, it is possible to mitigate the risk of adverse consequences stemming from policy shift through diversification. We firmly believe you should never-and we do mean never-put more than 5% of your portfolio in any one individual company's stock or bonds. But also, we believe you should consider your portfolio's exposure to this form of political risk. When investors' returns hinge on government money, policy shifts are a big risk.

[i] Remember, all US firms must report GAAP earnings. The reporting of non-GAAP earnings by public companies is a fine practice that can add great insights to a firms' success. For example, when currency volatility is high, constant currency results give investors a much clearer picture of a business' results than pure GAAP measures.

[ii] Ha! See what we did there?

[iii] Source: FactSet, as of 8/19/2016. Combined market value on 8/17/2016.

[iv] We did it again. Sorry.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Reviewing Q1 Earnings and What Q2 Expectations Say2026-06-18

-

Market Analysis Kevin Warsh and the Magical Delete Button2026-06-17

-

Market Analysis The Politics and Practicalities of the Social Security Trust Fund2026-06-16

-

Market Analysis Gold Fails the Safe Haven Test Again2026-06-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today