Personal Wealth Management / Economics

A Vicious Cycle?

Friday’s unemployment report showed better-than-expected hiring, but that hasn’t stopped some from fretting unemployment’s impact on economic growth.

Friday’s US employment report showed hiring totaled 103,000 jobs in September, exceeding too-dour consensus estimates of 60,000. Private-sector employers added 137,000 workers, while government payrolls contracted by -34,000. And August’s figures, which had shown zero jobs added (the source of much ire), were revised higher to show a modest gain. The employment rate, however, didn’t change—per the government’s calculations, only 90.9% of Americans in the workforce have jobs.

There’s little doubt that’s lower than the US’s post-war historical average of 94.2% employment. Some opine this creates something of a negative feedback loop—high unemployment dampens consumer demand (which accounts for roughly 71% of US economic activity), in turn lowering growth, ultimately resulting in low job creation. And then you’re back to square one. This cycle, triggered by what a strict Keynesian might call “low aggregate demand,” underpins many assertions of the desperate need to (governmentally) boost employment. Sounds like a complicated problem to solve! And in theory, it would be, except this cycle exists only in the theoretical economy, not the real one.

For this theory to be law, its opposite should hold equally true. Periods of high employment—like June 1953’s 2.6% unemployment rate, February 2001’s 4.2% or November 2007’s 4.7%, should create a positive chain reaction: High aggregate demand pushing the economy ever higher, reducing unemployment even further and resulting in a self-perpetuating cycle of eternal growth and full employment. Now consider: Those three monthly readings are all from months immediately preceding recession.

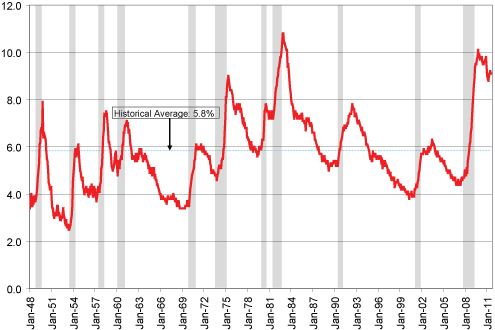

The exhibit below plots the US unemployment rate with recessions (as determined by the National Bureau of Economic Research) shaded. So as shown, it’s rare we get a recession when unemployment’s above the post-war average. Far more commonly, we’re well below the average when recessions arrive.

US Unemployment Rate, January 1948 – September 2011

Sources: Federal Reserve Bank of St. Louis, National Bureau of Economic Research.

And that makes a broad point about the relationship between unemployment and economic growth. Simply, the level of unemployment, be it ultra high or super low, tells you quite little about the economy’s future direction.

High unemployment is symptomatic of past economic weakness. It’s much like a cough that lingers for weeks after a cold has come and gone. When unemployment rises due to economic weakness and associated layoffs, companies don’t rehire in anticipation of a return to growth. They wait until experiencing ademonstrated rebound in sales. Then, too, firms commonly get productivity boosts during recessions (learning to make do with less), which allows them to delay hiring more. And hiring is a costly long-term investment for businesses, so it’s rational they’d be patient. Therefore, it’s not abnormal unemployment’s high and the economy’s growing—it’s actually quite typical. For example, look at the 1980s in the chart—unemployment was above average for the majority of the expansion. But that didn’t stop the economy and consumer spending from growing during that time.

We certainly agree more hiring would be a clear positive—after all, no one envies the position of those seeking work. But stretching this societal point to imply there’s a lack of aggregate demand in the US economy is going too far. After all, though only 91% of Americans are employed (as measured by BLS), consumer spending is at an all-time high.

That employment has a heavy influence on many folks’ feelings about the economy seems to us to be driven by the fact it’s highly relatable to any person’s lot in life. And readers, please set your expectations now: You are going to hear an enormous amount of political bluster about unemployment and what it means as we move towards the election. But frame this in its proper perspective: Economies do not add jobs overnight—irrespective of government plans—and the US’s economic future doesn’t hinge on that.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Insights Ken Fisher on Inflation Data, Currency Reset Risks, Commodity Opportunities and More– April 20262026-04-17

-

Market Analysis Foraging Through Japan’s February Data2026-04-17

-

Expert Commentary This Week in Review | Iran Conflict Update, Canada Election, UK GDP

2026-04-17

2026-04-17 -

Market Analysis An Economic Check In on the UK2026-04-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today