Personal Wealth Management / Politics

A Word on Impeachment and Stocks

If it occurs, impeachment likely wouldn’t end the bull market.

Editors’ Note: Our political commentary is non-partisan by design. We favor no party, elected official or politician and assess political developments solely for their potential economic or market impact.

With summer’s official end this past Monday, a chill isn’t the only thing in the morning air. Impeachment talk is, too. Late last week, reports emerged that President Trump pressured Ukraine’s president to investigate potential corrupt dealings involving former Vice President (and current presidential hopeful) Joe Biden’s son Hunter. House Democratic leaders claim this shows Trump collaborating with a foreign government to influence the 2020 election. They responded by formally opening an impeachment inquiry late Tuesday. Predictably, headlines are jam-packed with reporting, analysis, speculation and opinions, with some concluding impeachment is super meaningful for stocks. In our view, this is too hasty. While the drama may spur short-term market jitters, history shows impeachment isn’t necessarily negative for stocks.

In a sense, these latest developments aren’t new. Impeachment chatter has ebbed and flowed since roughly January 20, 2017, President Trump’s swearing-in. First it centered on alleged Russian collusion, then on alleged obstruction of justice and misuse of campaign funds. But yesterday, after more than three quarters of House Democrats joined calls for impeachment, House Speaker Nancy Pelosi directed the six committees investigating various Trump-related matters to continue doing so “under that umbrella of impeachment inquiry.”[i]

If you are looking for guesses about how this shakes out, winners and losers or implications for the 2020 presidential race, you have come to the wrong place. The situation is fluid, with fresh news, rumors and hot takes emerging seemingly by the hour. In our view, speculating about possible outcomes is a poor use of pixels right now.

As of this writing, a House impeachment vote isn’t scheduled. The next step is likely a heaping helping of testimony, hearings and fanfare, after which a simple majority vote would send Articles of Impeachment to the Senate. If it gets that far, a two-thirds Senate vote is required to convict and oust the president.

We are outlining possibilities here, not probabilities. Theoretically, both parties declaring this a hilarious misunderstanding and enjoying a good chuckle before returning to normal Congressional business is also a possibility.[ii] But markets move on probabilities, not possibilities. Based on what we know today, the probability of removing President Trump from office seems quite low. Since Republicans control the Senate by a 53 to 47 margin, Democrats would need 20 GOP senators to declare Trump guilty and remove him from office.[iii] If they did, we would all say hello to President Pence. Yet no Republican senators have come forward to support impeachment yet. Can they get those 20 senators? No idea, but presently it seems like a stretch. Moreover, impeachment isn’t politics as usual. A Republican-controlled Senate voted not to convict Democratic President Clinton. The bar is high.

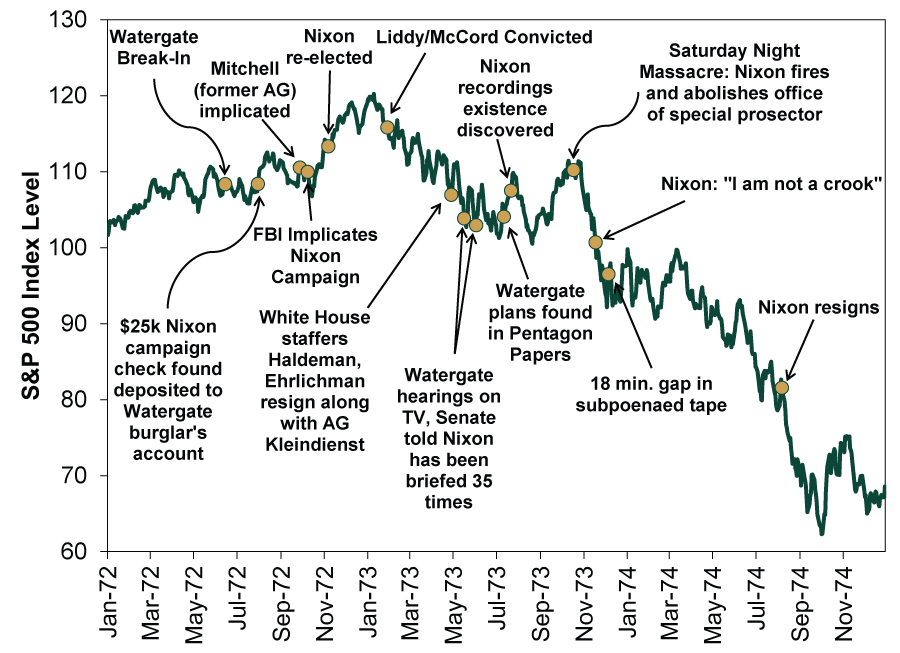

Even if impeachment advances, history doesn’t indicate market doom necessarily awaits. There are only two data points to draw on since reliable US stock market data begin, and neither suggest stocks would automatically suffer due to impeachment. As Exhibit 1 shows, the S&P 500 endured the 1973 – 1974 bear market while the Watergate scandal erupted and eventually forced President Nixon’s resignation under threat of impeachment. The political turmoil likely heightened volatility, but there was plenty else to roil markets then—such as the Arab oil embargo, Nixon’s economically damaging price controls and the Nifty Fifty stock bubble bursting. With this backdrop, pinning all the blame on Watergate seems inaccurate to us.

Exhibit 1: S&P 500 Surrounding Nixon’s Resignation

Source: Global Financial Data, Inc., as of 5/10/2017. Daily S&P 500 Price Index, 1/3/1972 – 12/31/1974.

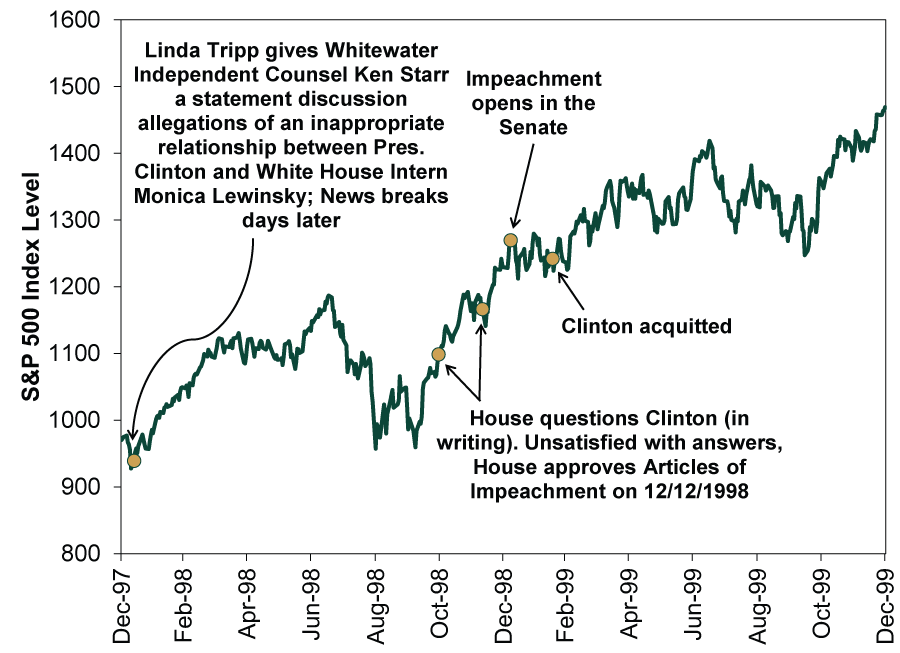

Conversely, US stocks mostly rose during the Lewinsky scandal and President Clinton’s impeachment trial.

Exhibit 2: S&P 500 Surrounding Clinton’s Impeachment

Source: Global Financial Data, Inc., as of 5/10/2017. Daily S&P 500 Price Index, 12/31/1997 – 12/31/1999.

It isn’t as though the impeachment inquiry has snuck up on investors, either. Congress was already investigating—this new iteration is just extra official. Further, this drama will play out in public, likely mitigating surprise power. If an impeachment trial opens, expect nothing to get more coverage. Stocks will hear the noise and likely bake in all opinions, forecasts and arguments. Surprises move markets most—and those don’t look likely as of now. Of course, short-term volatility tied to sentiment swings is always possible. Rising partisan rancor could roil sentiment here and there. But that is true impeachment or no—and is normal for a bull market.

As election season heats up, fevered impeachment coverage plus campaign trail bombast could make this a tough time to keep political biases from influencing your investment decisions. But we believe it is critical to do so, as such biases are blinding and can spur terrible investment decision-making. So do your best to stay above the fray and view developments dispassionately—like markets.

[i] “Pelosi Announces Impeachment Inquiry of President Trump,” Natalie Andrews and Andrew Duehren, The Wall Street Journal, 9/25/2019.

[ii] Seem far-fetched? That is sort of the point of possibilities. It is also why speculating about them is seldom fruitful, in our view.

[iii] Two Independent senators, Bernie Sanders of Vermont and Angus King of Maine, caucus with the Democrats. Hence, we counted them as Democrats.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today