Personal Wealth Management / Politics

A Word on the Inflation Reduction Act’s Climate Spending

Tax breaks and subsidies don’t make surefire investment winners.

Editors’ Note: MarketMinder is politically agnostic. We don’t prefer any politician, political party or policy proposal and assess political developments for their potential economic and market impact only.

As investors continue digesting the Inflation Reduction Act (IRA), which is now heading from the Senate to the House of Representatives, the conversation seems to be shifting from its tax changes to its spending provisions—in an optimistic sense. We have seen numerous articles arguing the tax breaks and subsidies for wind, solar, electric vehicles and other similar technologies will bring big gains for investors who try to ride those waves. Sounds nice, but in our view, this is a manifestation of a basic behavioral error: Stocks are probably too efficient for Congress’s plans to be a meaningful market driver from here.

In our coverage of the tax provisions, we pointed out that nothing in the bill was a surprise. Its contents were pulled over from the old Build Back Better budget reconciliation bill, which bounced around Congress throughout 2021 and early 2022. That bill was a hodge-podge of the Biden administration and several high-profile congresspeople’s campaign pledges, placing these initiatives in headlines way back in 2020. In our view, that history—and all the speculation, forecasts, opinion pieces and other chatter it generated—sapped the tax changes’ surprise power, which is the primary source of most legislation’s market impact. What is true for taxes must logically be true for the subsidies and tax breaks headed “green” energy’s way.

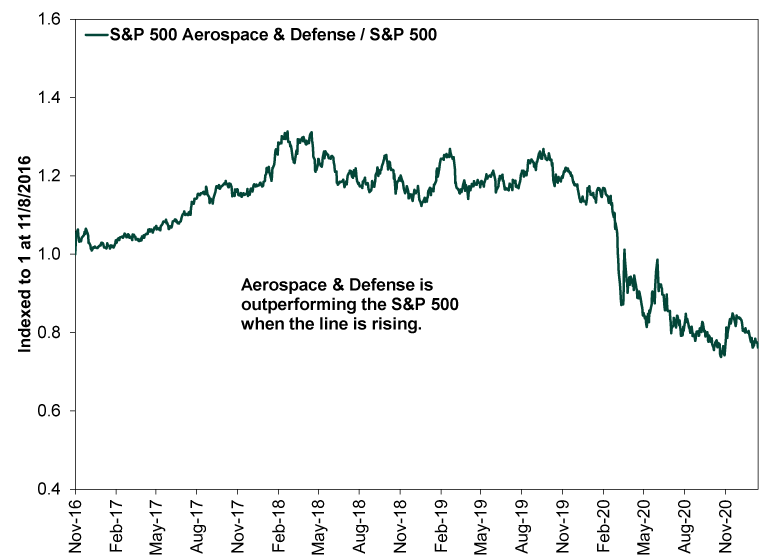

People touted wind, solar and electric vehicles as “Biden stocks” much the same way they heralded Aerospace and Defense stocks as “Trump stocks” after the 2016 election, presuming the new administration would bring policy shifts favoring that industry. But that thesis backfired, as Aerospace and Defense trailed the S&P 500 by a country mile over the entirety of President Trump’s term after leading for a spell early on. (Exhibit 1) This time, coverage of the IRA’s green provisions references recent stock price jumps for a number of the supposed winners, suggesting it is similarly priced.

Exhibit 1: So-Called Trump Stocks Weren’t Big Winners

Source: FactSet, as of 8/9/2022. S&P 500 Aerospace & Defense Industry and S&P 500 total returns, 11/8/2016 – 1/20/2021. Indexed to 1 at 11/8/2016.

Even the presumption that there are surefire winners from the IRA seems overstated to us. It stems from the basic assumption that government support will bring big success for the relevant companies and industries, vaulting them past competitors (presuming future Congresses don’t redirect the money, which is scheduled to drip out over a decade). But we are old enough to remember the story of Solyndra, a Bay Area solar company backed by the Obama administration over a decade ago. It was supposedly the future, but it went belly up, leaving taxpayers on the hook. An electric vehicle battery plant that received federal funds in 2010 charted a similar course, going from fanfare to furloughs and floundering within two years. Not to point fingers at the Obama administration—pretty much every presidential administration in modern history has made similar foibles. But it is a good reminder that governments don’t always pick winners.

Similarly, for those eager at the prospect of private investors backing the so-called “green banks” that will invest in wind, solar and electric vehicle firms, consider the UK’s ongoing misadventures with the government’s Future Fund, which takes stakes in startups. Fresh disclosures this week revealed, according to one non-executive director, that “‘most’ companies in the portfolio had ‘limited chance of growth to a sufficient scale of success’ and would become ‘zombie businesses.’”[i] That is just the tip of the iceberg of the world’s long history of public-private partnerships with questionable success.

Consider another possibility: that while Congress is directing subsidies to one corner of the clean-energy world, the market is channeling capital to another. Wind, solar and electric vehicles get a lot of green street cred because they lack smokestacks and tail pipes, but the world of clean and renewable energy is much broader and includes less-discussed innovations that are potentially more scalable. What about technologies that can generate more electricity on a smaller geographic footprint than wind and solar? What about solutions to high gas prices and auto emissions that don’t have such heavy mining footprints and the accompanying sociological concerns? These areas don’t get much attention from politicians, clearing the way for private investors and the market to propel technology forward. We don’t make long-term forecasts, and we don’t operate on long-term investment theses, but we see a strong chance that this frontier eventually proves more fruitful than politicians’ current darlings, cutting against the popular thesis today.

After a bear market, the lure of seemingly surefire winners is powerful. But markets don’t work like that—anything with that much hype rarely pans out. Moreover, investing is about the long-term journey toward market-like returns, not chasing quick moves in narrow categories. So stay diversified, think like markets, and don’t fall for hype.

[i] “The UK Government’s Venture Fund Has a Problem – With Failure and Success,” Helen Thomas, Financial Times, 8/9/2022.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Market Volatility, Energy Markets, US Inflation

2026-03-13

2026-03-13 -

Market Analysis Due Diligence and the DOL’s DOA Fiduciary Rule2026-03-13

-

In The News Oil prices will be lower in 6 months than when Iran conflict began, Ken Fisher argues2026-03-12

-

Market Analysis Rounding Up Odds and Ends From Global Energy Developments2026-03-11

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today