Personal Wealth Management / Market Analysis

Abenomics and Other April Fools

With a sales tax hike about to bite an already weakening Japanese economy, the Land of the Rising Sun looks even more like the Land of Rising Disappointment.

If Japan’s sales tax hike bites its already weakening economy, Prime Minister Shinzo Abe might not be grinning for long. Photo by Scott Halleran/Getty Images.

Ordinarily, April in Japan means one thing: the cherry blossom festival! For many Japanese, the arrival of spring and bursting sakura blossoms represent great hope and new beginnings. This year, however, April 1 brings a less joyous beginning—a sales tax hike. A sales tax hike, that is, on top of an already wilting economy and economic reform plans that seem more April Fools than reality. Hopes still seem high for the Land of the Rising Sun, but to us, it looks more like the Land of Rising Disappointment.

This isn’t what most folks expected when Shinzo Abe became Prime Minister in December 2012 on promises to restore Japan’s economic (and military) might. Recalling an old folktale, Abe promised to fire “three arrows” at Japan’s long-moribund economy: aggressive monetary stimulus, fiscal stimulus and economic reform. It wasn’t the first time anyone had promised the third arrow, but with a 70%-plus approval rating, Abe seemed to have the clout. He also seemed to understand the importance—the lesson of the “three arrows” folktale is that the whole is greater than the sum of the parts. That would suggest Abe knew arrows one and two, alone, wouldn’t cut it.

And so Japanese stocks took flight, enjoying a sentiment-driven rally as Abe fired arrows one and two in early 2013. Abe’s cabinet front-loaded ¥10.3 trillion in fiscal stimulus, and the BOJ launched an open-ended “quantitative and qualitative easing” (QQE) plan to increase the monetary base by ¥62 trillion in 2013 and ¥70 trillion this year, with a goal of weakening the yen and bringing inflation to 2% annually within two years. As for reform, Abe talked. A lot. Throughout 2013’s first half, he assured investors his “growth committee” was exploring ways to cut corporate taxes, reform the labor code, improve corporate governance and encourage behemoth businesses to restructure, improving competition. That teed up expectations for groundbreaking measures at his hotly anticipated reform announcement in June, but the package fizzled—it was long on pie-in-the sky growth targets and general wants, but short on actual policy changes.

Japan optimists tried to rationalize the disappointing proposals by saying Abe didn’t want to rock the boat ahead of July’s upper house election. And Abe, with an upper house victory in his belt, did gather the press for another reform announcement in September—but this, too, lacked anything concrete. When Abe tried again in January, claiming he would “drill” through vested interests in order to finally bring Japan into the 21st century, the world largely sighed.

As did Japan’s economy. Early on, to the untrained eye, arrows one and two seemed to work. Real GDP grew at seasonally adjusted annual rates of 4.5% and 4.1% in Q1 and Q2, respectively, and export values soared thanks to the weak yen. Inflation, too, improved. Still falling when Abe took office, CPI was positive by June and finished February 2014 at 1.5% y/y. But under the hood, all was not well. Export volumes barely budged even as values regularly rose over 20% y/y—the weak yen didn’t do much for actual output. It also hurt businesses and households by making imported energy far more expensive—not a great development for a country relying on foreign fuel after taking every nuclear power plant offline. That rosy inflation number is largely a function of pricy imported fuel: Strip out fresh food and energy, and inflation is up to just 0.7% y/y as of February—this is not a virtuous cycle of growth and prices lifting each other. It’s a headache of higher energy prices.

Now, enter the sales tax hike. It jumps from 5% to 8% on April 1. Consumers have been front-loading big-ticket purchases in advance, with household spending growth outstripping GDP growth in Q4. Common sense says that pull-forward effect would last until the tax takes effect, yet household spending fell -0.25% in February. That also defies the main premise behind the government’s efforts to drive up inflation. As their logic went, while Japan remained in deflation, consumers would always delay spending in hopes of a better deal—higher prices were supposed to goad folks into spending more today. A fine theory! Problem is, if prices and overall cost of living rise while wages stay stagnant, folks will pinch pennies wherever they can. Some major firms recently agreed to hike base salaries for the first time in years, but overall, wages haven’t kept pace with prices.

Japanese households, simply, are squeezed. When the calendar flips to April 1, they’ll be even more squeezed. Finance Minister Taro Aso announced the government’s solution last week: frontload 40% of Japan’s fiscal-year spending into Q2 to offset the expected drop in demand. It’s the same old tax-then-spend tactic Japan has tried, off and on, through 17 years of lackluster growth. We rather doubt it works any better this time.

We also wouldn’t put much stock in Abe’s continued reform pledges. Talk is cheap. Action is what matters, and the only item seeing action lately is the military—Abe seems to be spending his energy pushing for a buildup of Japan’s self-defense forces, and these initiatives are costing some hefty political capital. Pacifist coalition partner New Komeito isn’t pleased, and insiders say the government’s cracks are showing. Meanwhile, within Abe’s Liberal Democratic Party, some factions aren’t pleased with slow economic progress and proposed electoral reforms that would cut into the party’s rural power base. These, along with labor groups and the notoriously bureaucratic Japan Business Federation, are the vested interests Abe will have to drill through.

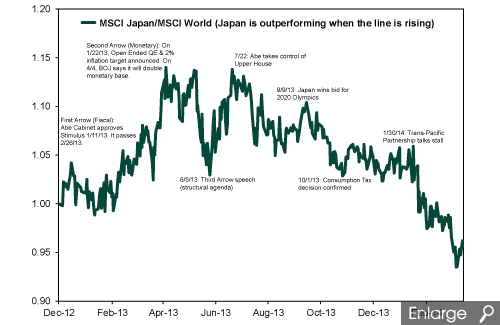

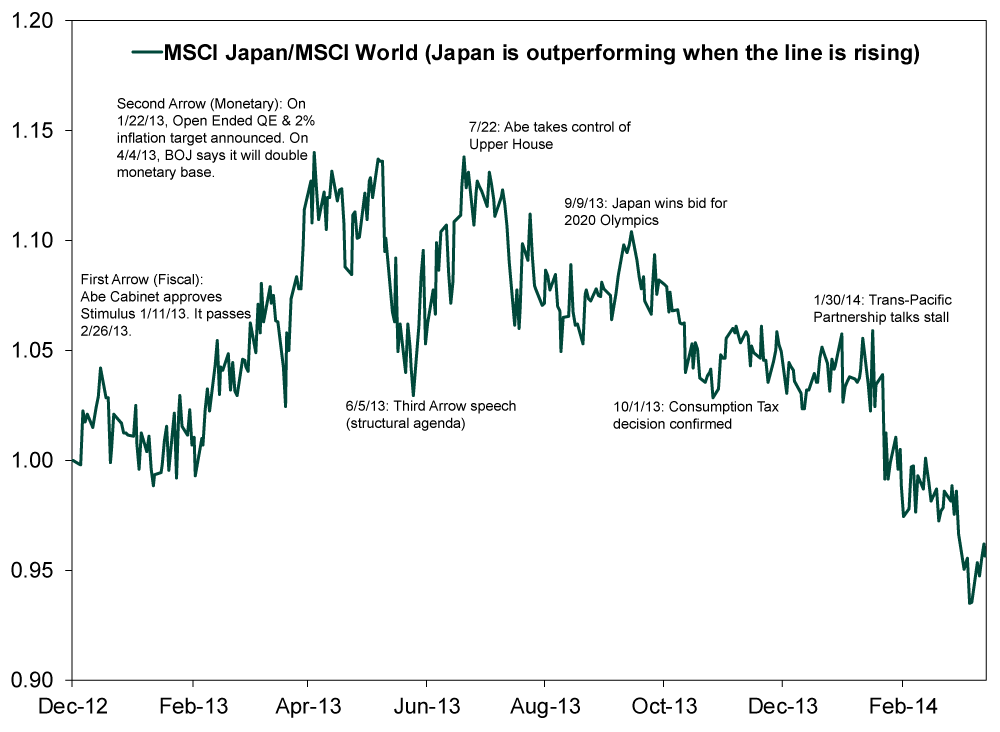

Despite all this, many still expect Japanese stocks to do well this year. Many professionals predicted Japan would top the world. To us, however, the chances look slim. For as much attention as Japan got last year, those gains were concentrated in the first half. As shown in Exhibit 1, while Japan outperformed through late May, it has lagged badly since, and Japanese stocks have now underperformed, cumulatively, since Abe’s election. Looking ahead, there doesn’t appear to be much reason for this to radically reverse course.

Exhibit 1: MSCI Japan Relative Returns

Source: FactSet, as of 3/31/2014. MSCI Japan and MSCI World Indexes, 12/14/2012 – 3/28/2014.

To anyone still holding out hope, we offer a parting anecdote. Japan last hiked its sales tax in April 1997, from 3% to 5%. At the time, Japan had been enjoying a fairly solid recovery. But then an 18-month recession set in, with consumer spending falling -13.2% in 1997. Nominal GDP has never regained the high it hit in Q1 1997. Now, we aren’t saying Japan is guaranteed another 17 lousy years from here simply because of a sales tax. But that prior experience speaks to a sales tax hike’s theoretical ability to choke off a budding expansion. With all the other factors not going in Japan’s favor at the moment, we’d suggest better opportunities lie elsewhere.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News What ‘IPO’ really stands for — and whether you should be buying SpaceX and the AI giants2026-06-23

-

Market Analysis Today in Brexit, Day 3,652: Brexit Turns 102026-06-23

-

Expert Commentary 3 Things You Need to Know This Week | Global PMIs, US PCE Inflation, Annuities

2026-06-22

2026-06-22 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—June 15 - June 192026-06-22

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today