Personal Wealth Management / Economics

About That Stronger-Than-Expected GDP Report

Not as hot under the hood, given a lot of the upside was from net exports and inventory change, but still fine.

With many folks fretting economic slowdown, Friday’s Q1 GDP report received more attention than usual. The result: better-than-expected growth! While pundits were quick to high five, we think investors are better off playing it cool and calm. This report was neither as good as the headline figure hinted nor as bad as many feared earlier this year.

Q1 GDP growth accelerated to 3.2% annualized from 2.2% in Q4, easily topping expectations of 2.0%.[i] Nice news, but the excited reaction seems a tad overstated. The acceleration came mainly from trade, inventory changes and government spending, which aren’t necessarily positives. Export growth is fine, but imports’ decline—while adding to GDP—could be interpreted negatively as imports represent domestic demand. Likewise, inventory growth contributes positively, but it is open to interpretation. Rising stockpiles could mean businesses expect solid demand—and we suspect that is the case here—or a sign of firms having difficulty moving product. Government spending also isn’t always well allocated and could crowd out private-sector activity. All this added over two percentage points to Q1 GDP growth, more than half the total.

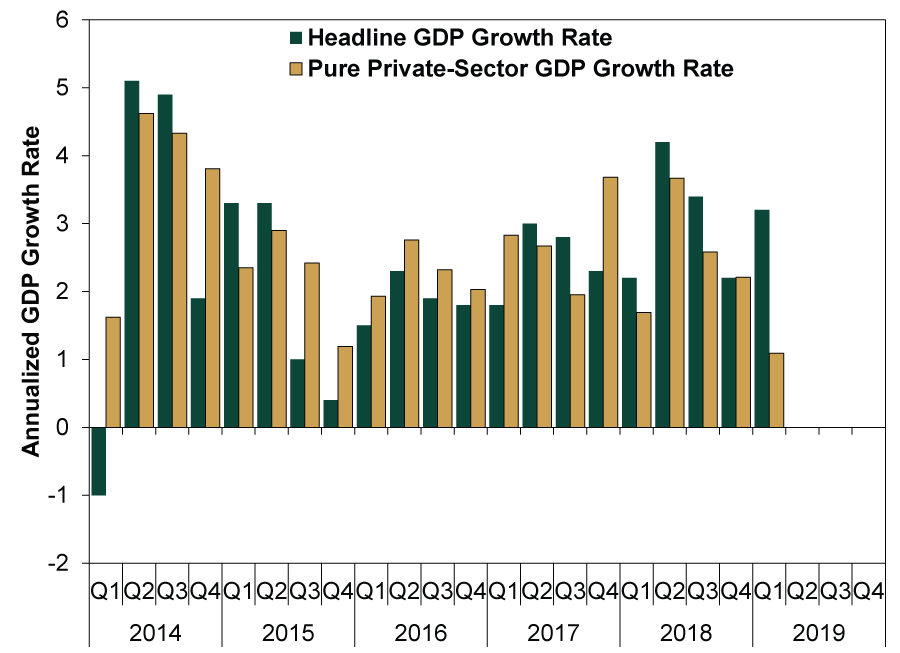

In contrast, private sector GDP continued slowing in Q1. Collectively, the components we consider pure private-sector demand—consumer spending, business investment and real estate activity—slowed to 1.1% annualized from Q4’s 2.2%. (Exhibit 1) Which is still fine, don’t get us wrong. It just isn’t as great as the headline figure some pundits touted. However, it also beats expectations from earlier in the quarter, when many pointed to real-time estimates of output and feared 0.3% growth or even worse.[ii] Overall, with America’s pure private sector components chugging along, we see little reason here to be concerned about growth.

Exhibit 1: Headline and Pure Private-Sector GDP

Source: Bureau of Economic Analysis, as of 4/26/2019. GDP and “Pure Private-Sector GDP” (personal consumption expenditures, residential investment and nonresidential private fixed investment), Q1 2014 – Q1 2019.

Some suggest suspect growth drivers are masking private sector demand weakness, but we think this is too dour. Private-sector GDP may not always have the biggest growth contributors, but as long as it is ticking higher overall, we think it shows economic fundamentals are fine. As Exhibit 1 showed, ebbing and flowing is normal. Also, there could be seasonal quirks at play. Q1 is known to understate GDP growth due to faulty seasonal adjustments. The BEA says its statisticians have fixed these issues, but it may be they are still working out the kinks. Further, GDP is backward looking, and for investors, stocks look forward. GDP may tell you what happened—imperfectly—but what matters more for markets is what lies ahead, which leading economic indicators imply is likely further growth.

With widely watched headline GDP beating expectations, it seems pundits are starting to take a rosier view and citing marquee economic reports like this—and other data such as March’s best-in-two-years retail sales—as reasons to be bullish. We think this is a bit off base, but it does signal warming sentiment—a glass more full than empty. Pundits may reach the right conclusion—economic optimism—for the wrong reasons, but with the economy growing fine and forward-looking gauges suggesting more ahead, sentiment isn’t out of whack, in our view. Bull-killing euphoria doesn’t come until most disregard leading indicators that contradict their backward-looking cheer. Until then, we expect stocks to continue rising.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Insights Ken Fisher on Inflation Data, Currency Reset Risks, Commodity Opportunities and More– April 20262026-04-17

-

Market Analysis Foraging Through Japan’s February Data2026-04-17

-

Expert Commentary This Week in Review | Iran Conflict Update, Canada Election, UK GDP

2026-04-17

2026-04-17 -

Market Analysis An Economic Check In on the UK2026-04-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today