Personal Wealth Management / Market Analysis

About Those European Banks

European bank stocks took a pounding, but Lehman comparisons miss the mark.

Editors' note: MarketMinder does not recommend individual securities. The below is simply a broader theme we wish to highlight, not a recommendation to buy, sell, hold, sell short, free deliver, gift or otherwise transact in any securities mentioned.

By now, you have probably seen the headlines. There is "a bitter cocktail of concerns swirling around Europe's banks." Many fear the industry is "facing its own Lehman Brothers moment." "Deutsche Bank's hybrid bonds are locked in a death spiral," the Stoxx Europe 600 bank index "hit multi-year lows" as Societe Generale plunged another 14% on Thursday, and it's all about to come crashing down "like a game of Jenga." But before you brace for September 2008 redux, take a deep breath, have a glass of something comforting, and stick with me. I'm not about to argue everything is hunky dory[i] in European Financials, but the issues at hand are widely discussed and not the sort that wipe a few trillion off global GDP before anyone realizes that's happened. The sector's fundamental outlook hasn't vastly worsened this year, and there are some key differences between now and 2008.

Here, as best I can summarize them in a short space, are the various, loosely related fears that have snowballed. Most visible to Americans are flattening yield curves, which heightened fear of shrinking (or even negative) net interest margins, which could whack loan profits and threaten earnings. Adding another wrinkle, falling high-yield bond markets and trouble in commodity-related sectors drove jitters over credit quality and future loan losses. Less discussed here are the regulatory issues-namely, the implementation of Europe's system for winding down failing banks by "bailing in" shareholders, creditors and large depositors (instead of bailing them out with taxpayer money) and the adoption of Basel III's highest capital requirements in 2019. The latter is fairly simple: Eurozone banks are a bit behind US and UK banks at building capital buffers, and investors worry they'll have to issue new equity to get there (presuming flat yield curves will give them few earnings to retain), further diluting earnings per share. To say shareholders are fatigued with bank equity issuance is probably an understatement. Since 2007, Banco Santander has doubled the number of shares in circulation, diluting earnings by half. Standard Chartered has 50% more shares out there. Deutsche Bank has an astounding 140% more.[ii]

Bail-in is a bit more complex. Conceived in 2013, finalized in 2014 and taking effect last month, it makes Cyprus's 2013 misadventures the blueprint for all future eurozone bank failures, making investors prone to run at the first sign of trouble, before central banks can bail them in. They're extra antsy because officials haven't been exactly clear on what could trigger a bail-in-past statements from ECB Chief Mario Draghi implied simply failing a stress test could do it.

The implementation of new rules everyone knew was coming probably wouldn't ordinarily hit sentiment this much, but Portugal's central bank botched a bail-in in late-December. The bank in question is Novo Bank, which rose from the ashes of the failed Banco Espírito Santo in 2014. Novo Bank was the "good bank," with all Banco Espírito Santo's viable assets, which the state planned to sell off later. They bailed in some bondholders at the time, following the Cyprus blueprint (but sparing depositors), and it all seemed orderly. But in December, when readying Novo Bank for sale, the central bank re-resolved it to shore up capital, transferring about €2 billion in bond liabilities back to Banco Espírito Santo, where they became basically worthless overnight. But instead of treating all bondholders equally, they decided to spare retail investors, instead transferring the five bonds that happened to belong to institutional investors-namely, Blackrock and Pimco. Markets do not like it when governments pick winners and losers, especially when it is so arbitrary and contravenes what was intended to be an orderly, predictable, continent-wide system. That makes it hard to assess and price risk, and it forces investors to adjust their expectations in a hurry. That particular uncertainty might be short-lived, as the Novo Bank case is already on its way to court, and judicial precedent might restore sanity, but that's too far off to handicap now.

In the meantime, investors have repriced European bank bonds in a hurry to account for the added risk-particularly hybrid bonds, known officially as contingent-convertible and colloquially as coco, which convert to equity when the bank needs to shore up capital, making them among the first in line to get bailed in. Investors don't really appear to be discriminating among the weak and healthy banks for the moment. Italian banks got hammered-understandably, as their nonperforming loan ratios exceed most other countries' and the government only just finalized a clean-up plan-but so did healthier banking stalwarts in Germany and France.

Of these, Deutsche Bank stole the most headlines, with its coco bonds and shares leading the way down.[iii] Last year, Deutsche announced it was pausing dividend payments for two years, and even with the cut, its preliminary Q4 earnings were awful (by "earnings," I mean a €6.7 billion loss, their worst ever). Tier 1 capital fell from 11.5% in Q3 to 11.1% at year-end, and with yield curves flat and global growth fears swirling, investors put two and two together and feared Deutsche would stop paying interest on its cocos and dilute shareholders again with yet another capital raise. Cue those Lehman comparisons. After all, who can forget Lehman's mounting losses, rumored insolvency and the constant "No I swear it's totally fine" from former CEO Dick Fuld, mere weeks before bankruptcy?

But this is nothing like Lehman. As we've written many times over the years, Lehman was illiquid, not insolvent. Mark-to-market writedowns on mortgage-backed securities hit its capital, yes, but they also wrecked its loan collateral, making it impossible to secure overnight funding to cover its daily obligations. At the time the Fed forced its bankruptcy,[iv] Lehman's assets exceeded its liabilities. On paper it was solvent. It just couldn't sell the assets, which weren't liquid, and as a pure investment bank, it couldn't tap the Fed's discount window for emergency funding. And needless to say, other banks wouldn't lend to it. Without cash to cover daily needs, it died.

Deutsche is different: It's solvent and liquid. Yes, its credit default swap costs spiked, but that doesn't mean its actual default risk spiked. As others have noted, cocos aren't liquid, and selling an illiquid asset during a freakout is unwise and undesirable. Credit default swaps are the quick solution if you want to hedge a bond, and rising demand spiked costs. Simple as that. As for capital, that 11.1% Tier 1 ratio is fully compliant with current Basel guidelines, and it's higher than Deutsche's Tier 1 ratio in 2007 and 2008. Besides, capital is an arbitrary measure and regulatory construct. Regulators pick and choose what qualifies, making odd decisions like "all sovereign debt is totally fine," which leads to odd situations like Cypriot banks calling Greek debt a viable part of their liquidity buffer (that's why they failed). Banks are supposed to build it up in good times so they can draw on it during bad times. A bank whose capital falls during a nasty quarter is a bank being a bank, using its cushion. The alternative is deleveraging at every hint of trouble, which would be deflationary and turn minor bank headwinds into systemic problems.

Having a bit less capital doesn't make it impossible for banks to function, lend and stay afloat. Being illiquid would make it impossible for banks to function, lend and stay afloat regardless of capital, because capital must be liquidated for it to be of use in a pinch. If a bank is liquid, they can probably cover their obligations and do fine whether their Tier 1 capital is at 6% or 20%. Deutsche Bank is liquid. It's so liquid, as it happens, that it is buying back a bunch of bonds to put those interest payment fears to bed[v] and, in a fun little accounting trick, book a profit and shore up capital. As Bloomberg's Matt Levine writes :

One thing this tells you is that the worries about Deutsche Bank aren't very acute. I mean, you can worry about Deutsche's long-term profitability or capital position or legal expenses or ability to transform itself or whatever; those are all real and substantive worries. But bank panics aren't about long-term profitability. They're about liquidity: They're sparked by the worry that the bank won't have enough money to pay you back. The fact that the market would reward Deutsche Bank for reducing its liquidity to improve some theoretical accounting metrics suggests that its concerns about Deutsche Bank just aren't that pressing.

More succinctly: Folks don't queue up outside bank branches demanding their deposits back because of questions about profit growth's trajectory.

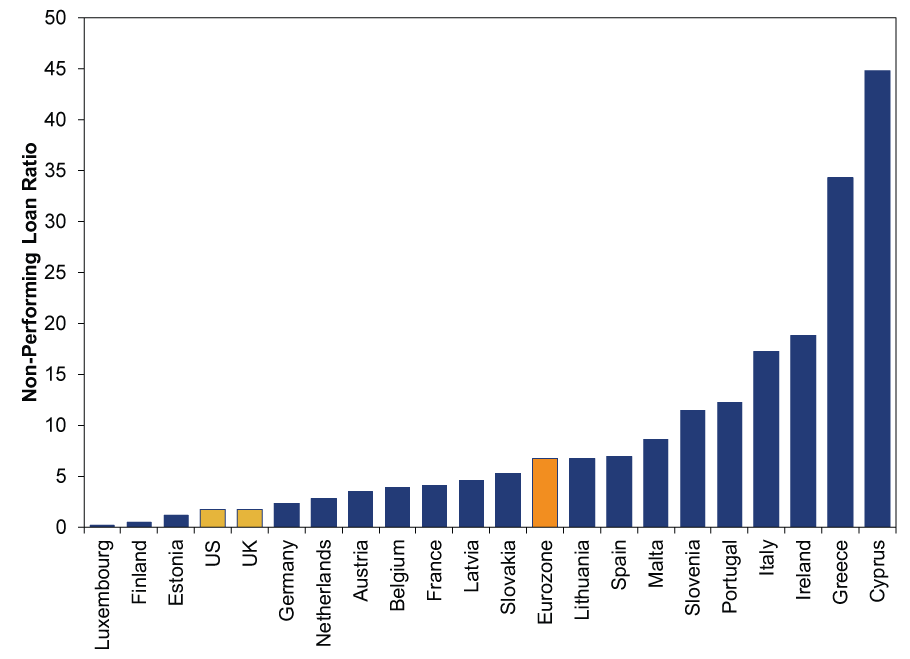

As for the rest? Across the European banking system, conditions are miles better than most appreciate. Capital ratios are up substantially from the crisis's depths. Balance sheets have more cash. Book values are up across the board. Non-performing loans are down throughout core Europe, and as Exhibit 1 shows, German banks' non-performing loan ratio, at 2.3%, is just a tick higher than the US and UK. Legal and regulatory fees and settlements are a wild card, but eventually these will wane, further reducing costs.

Exhibit 1: Non-Performing Loan Ratios in the Eurozone and Select Countries

Source: World Bank, as of 2/10/2016. Non-performing loans as a percentage of total gross loans. All figures are for the year 2015 except for Luxembourg (2013), Finland (2012), US (2014), Germany (2014), France (2014) and Italy (2014), due to data availability.

As for the other fears in this vortex, they're simply another manifestation of long-running and widely overstated fears of slowing global growth and cheap oil. Forward-looking economic indicators largely point positively in the developed world and commodity-importing Emerging Markets. Continued growth should support corporate profits, boosting investment banking results and capital markets activity. Outside the Energy and Materials sectors, high-yield corporate bonds are mostly ok. Flatter yield curves do impact bank profits, but Treasury markets are volatile. We're in the middle of a fear surge where sentiment is so irrational, investors are paying for perceived stability. As fundamentals regain influence, the competing forces tugging at supply and demand should keep long-term yields in the overall directionless drift they've endured since last year (just as market forces tugged yields higher after a similar, though less exaggerated, plunge last spring).

Finally, while reading too much into valuations is chancy, it's worth noting all these banks are trading at extremely heavy discounts to book value. That is a strong sign they're down on sentiment and widely known fears, not severe fundamental problems. It's the latest case of investors seeing a 2008 repeat around every corner while ignoring the positives. It shouldn't take much good news to bring relief.

[i] David Bowie reference intentional.

[ii] This is also why comparisons of share prices today to those during the crisis are off base. Supply is up massively, so the same share price today reflects a far larger market value of the entire business.

[iii] A note on repricing risk: Deutsche issued the cocos in question in May 2014, when bail-in was but a twinkle in regulators' eyes and long before Portugal botched Novo Bank. The offering was oversubscribed at about 8x. There isn't much evidence investors were terribly discerning or really grasped the fact their 6% coupon wasn't sacrosanct, particularly once some esoteric German accounting rules were factored in. Now reality is setting in.

[iv] See the Fed's September 15, 2008 meeting transcript, do a keyword search for Lehman, and read through the high-fiving and back-slapping as they congratulate themselves for taking a stand and making an example of the investment bank by denying its suitors funding. Despite the fact they'd arranged and aided JPMorgan Chase's shotgun wedding to Bear Stearns earlier than year, when Bear was in a predicament identical to Lehman's.

[v] They would reportedly buy secured bonds, not cocos, but the implication is that if they have the cash to buy back bonds, they have the cash to pay coco interest.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

-

Interesting Market History COVID-Panic’s Lockdown-Low Anniversary2026-03-25

-

Market Analysis The Golden Paradox2026-03-24

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today