Personal Wealth Management / Market Analysis

America Forever?

US stocks have been leading lately, but don’t forget the benefits of a global focus.

US stocks have been on something of a tear of late—outpacing the rest of the developed world overall. The non-US developed world (as measured by the MSCI EAFE) hasn’t done terribly—its stocks are positive YTD and over the past 12 months.i They’ve just lagged the US overall and on average.

The buzzword in the prior bull market was “global” and Emerging Markets were particular darlings. But investors may now be asking, if the US has done so well, why bother with global? Because leadership will rotate. It always does.

Also, US outperformance is a relatively recent phenomenon. Over the past ten years (ending 03/31/2013) EAFE outperformed US stocks.ii Proof non-US stocks are best? Nah—just more of the same rotation. US stocks led for much of the 1990s. If you decided that meant US stocks were somehow permanently better, you missed the buoying effects foreign stocks had during much of the 2000s when US stocks overall lagged.

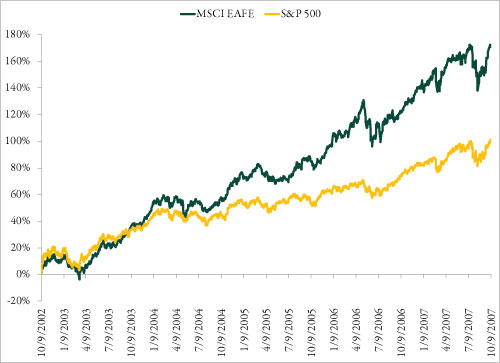

Don’t take that to mean cycles happen in neat decades. They don’t—any 10-year measurement is purely arbitrary. Cycles can be shorter or longer (US stocks about matched global during the 2000-2002 bear market, but lagged badly in the 2002-2007 bull—Exhibit 1). There’s just no way to know which stock category will be superior 3, 5 or 10 years from now.

Exhibit 1: US Versus Non-US Developed Stocks

Source: Thomson Reuters, Global Financial Data, Inc., S&P 500 and MSCI EAFE price returns from 10/09/2002 to 10/09/2007.

The marvelous part is, if you’re in it for the long haul, you needn’t pick and choose US versus foreign. Instead, you can invest globally. First, investing globally provides more opportunities. Second, finance theory tells us the more broadly you diversify, the more you mitigate risks extant in narrower categories. You can’t get broader than global—until we discover sentient life forms in other solar systems who are similarly motivated by profits.

But this means, as a global investor (if you’re doing it right), you’ll experience periods when US will outperform, or foreign will outperform or Technology or Germany or mid-cap Consumer Discretionary stocks will. But finance theory tells us all equity categories, if properly constructed, should yield similar returns over long periods, though traveling different paths.

Those “different paths” frequently trip up investors, behaviorally. It can be excruciating to watch a narrower category do materially better. More so if that outperformance period runs for some time. But radically shifting focus, like moving from global to wholly US (or wholly non-US or German or mid-cap Consumer Discretionary) is often much more about chasing heat than anything else. And for many investors, there’s a bit of home-country bias as well. After all, Greecewas the among the best performing developed nations globally in Q1 2013. In 2012, European nations (Belgium, Denmark and Germany) were atop developed world performance.Yetwe see few arguing European stocks are inherently, structurally superior.(Rightfully so.)

Heat chasing is devilishly tough to diagnose in oneself. We don’t do it because we know we’re chasing heat. Rather, we justify it as a smart, rational decision. But if you’re considering any form of material category change, ask, “What do I know about this category that few others realize, making it inherently long-term superior moving forward?” (We say again, it should be something few other people realize—not, for example, “Well, Europe is kind of an economic mess right now,” because that defines widely known.) If the reason for the shift is largely past performance, it’s heat chasing.

And heat chasing can be costly. Research firm Dalbar, Inc., helps quantify just how costly (using easily measured mutual fund flows). In their annual study on investor behavior, they found that over the past 20 years (ending 12/31/2012), equity mutual fund investors earned an annualized 4.3% while the S&P 500 annualized 8.2%.iii Now, some of the performance lag could be because the mutual funds themselves underperformed. But Dalbar’s research also showed the average mutual fund investor held their funds for just 3.3 years. In Dalbar’s words: “One of the most startling and ongoing facts is that at no point in time have average investors remained invested for sufficiently long periods to derive the benefits of the investment markets.” iv In other words—investors switched strategies much too often. They chased heat. They got spooked. They experienced a range of emotions leading them to make material changes that may not have been in their long-term best interests, and as a result, their performance suffered.

In our view, it’s likely US stocks outperform the world for the balance of the year—we believe we’re at a stage in a maturing bull market when the world’s largest stocks typically outperform. And the US is home to a huge chunk of those biggest-of-the-big firms. But because we have a global focus, we wouldn’t want to miss out on the myriad long-term benefits of broader, global diversification.

i Thomson Reuters. S&P 500 total return and MSCI World Index total return net of dividends

ii Thomson Reuters. S&P 500 total return and MSCI World Index total return net of dividends

iii Dalbar, Inc., 2013. Quantitative Analysis of Investor Behavior.

iv Dalbar, Inc., 2013. Quantitative Analysis of Investor Behavior.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Reviewing Q1 Earnings and What Q2 Expectations Say2026-06-18

-

Market Analysis Kevin Warsh and the Magical Delete Button2026-06-17

-

Market Analysis The Politics and Practicalities of the Social Security Trust Fund2026-06-16

-

Market Analysis Gold Fails the Safe Haven Test Again2026-06-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today