Personal Wealth Management / Market Analysis

American Banks’ Strength Doesn’t Make Them Great Investments

While the US economy is humming, helped along by banks’ strong balance sheets, a flatter yield curve will likely weigh on their profits eventually.

As financial crisis retrospectives make the rounds, a refreshingly large sample note the US banking system’s current strength. Failures are way down, profits are way up, and lending is rising—all good things. Yet, none of this necessarily means US banks are a great opportunity for investors right now. Markets look forward, not backward, and US banks likely face some headwinds in the foreseeable future.

By all means, take a minute to celebrate how far banks have come since the crisis. Regulatory capital was just 2.5% of the eight largest banks’ total assets in 2007.[i] Now, the top eight banks’ capital-to-asset ratios average 6.6%.[ii] Problem banks exist, but their numbers are dwindling. As of Q2, the Federal Deposit Insurance Corporation (FDIC) lists 82 banks as “problem institutions.”[iii] In 2010, there were 884.[iv] Meanwhile, no banks have failed so far this year—down from 157 in 2010.[v] If the stretch continues, 2018 will be the first year since 2006 without a bank failure—not surprising with 96% of all banks profitable.[vi]

In Q2, US banks enjoyed record-high profits and soaring net interest income. Profits rose 25.1% y/y to $60.2 billion—not a bad haul.[vii] According to the FDIC, about half the gains were from last year’s corporate tax reform (a one-off), but the other half came from higher net interest income—profits from lending. Banks’ profits stem from the yield curve—namely, the gap between interest rates on their short-term funding and the long-term loans they extend to households and businesses. Because banks borrow short and lend long, the difference between short- and long-term rates—the yield curve—closely approximates their profit margins (aka “net interest margins”).

Often, when Fed rate hikes cause the yield curve to flatten, banks’ profits shrink. This time, after seven rate hikes totaling 1.75 percentage points since late 2015, the gap between the 10-year Treasury yield and effective fed-funds rate has narrowed about a percentage point. Yet banks have maintained their margins. What gives? The reason: Banks haven’t passed on Fed rate hikes to depositors. That is largely because the Fed’s quantitative easing (QE) programs since 2008 flooded the banking system with reserves. Before QE, banks competed for deposits—their funding base—by raising checking and savings rates alongside fed-funds rates. But with a reserve glut, banks didn’t need more deposits and haven’t much raised checking and savings account rates—as you may have noticed. Average rates still hover just above zero. Hence, banks have been relatively insulated from yield curve flattening thus far.

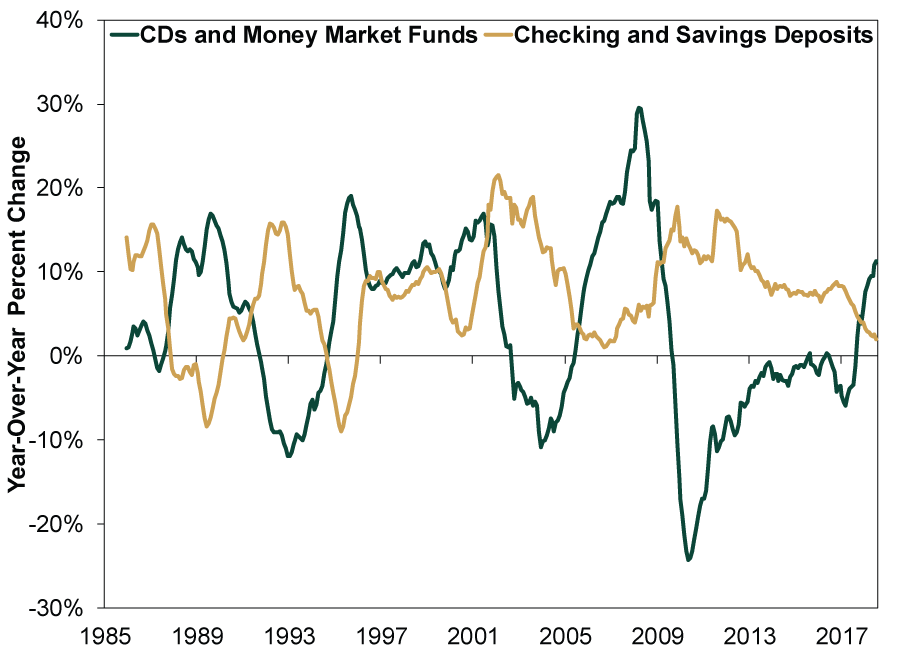

But monetary policy typically works with a lag, and there are signs banks may be about to raise deposit rates, which would weaken their loan profits. Last year, higher-yielding deposits—certificates of deposit (CDs) and money market funds—grew faster than lower-yielding deposits (checking and savings) for the first time since 2009. (Exhibit 1) Depositors are noticing better deals and moving to take advantage of them. To compete, banks will likely have to raise the rates they offer on checking and savings accounts. (Exhibit 2)

Exhibit 1: Higher-Yielding Deposits Growing Faster than Lower-Yielding Ones

Source: FactSet, as of 9/13/2018. Institutional money market funds, retail money market funds and small-denomination time deposits summed and demand deposits and savings deposits summed, January 1985 – July 2018.

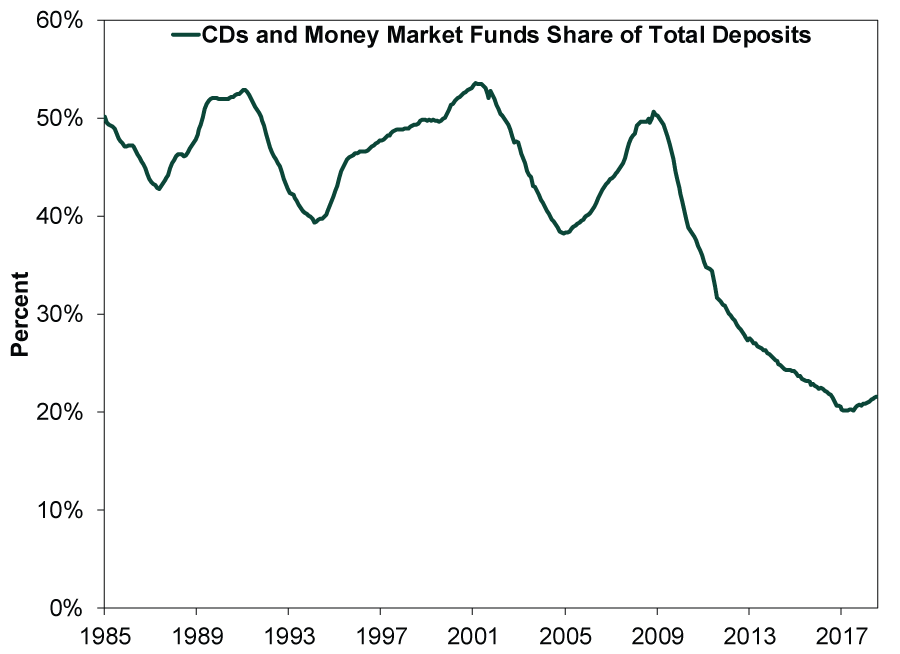

Exhibit 2: Higher-Yielding Deposits’ Share of Total Reversing Off All-Time Lows

Source: FactSet, as of 9/13/2018. Institutional money market funds, retail money market funds and small-denomination time deposits summed as a percentage of all deposit instruments (e.g., checking accounts, other checkable deposits, savings accounts, money market funds and CDs), January 1985 – July 2018.

As banks’ funding costs rise, their net interest margins erode. With the yield curve positively sloped, banks will likely still make loans—fueling overall economic growth—but they probably won’t be as plentiful or profitable, which is what matters for investors. August’s weaker loan growth may be the first sign of a shifting tide.

We aren’t wholly down on US Financials, but we think better opportunities lie in more diverse institutions whose profits aren’t tied to net interest margins—banks with strong capital markets businesses. But we think the largest Financials opportunities are outside the US, particularly southern Europe, where expectations are much lower and the potential for positive surprise higher as the ECB continues reducing QE.

[i] “Can We Survive the Next Financial Crisis?,” Yalman Onaran, Bloomberg, 9/10/2018.

[ii] Ibid.

[iii] Source: FDIC Quarterly Banking Profile, as of Q2 2018.

[iv] Ibid., as of Q4 2010.

[v] Ibid., as of Q4 2010 and Q2 2018.

[vi] Ibid., as of Q2 2018.

[vii] “U.S. Banking Sector Profits Hit Record $60.2 Bln in Q2 2018 - FDIC,” Pete Schroeder, Reuters, 8/23/2018.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-17

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, Central Banks, Defense Spending

2026-03-16

2026-03-16 -

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today