Personal Wealth Management / Market Analysis

An Often Overlooked, Yet Obvious Point on UK Trade

As a source of export demand, the eurozone in aggregate is significant to the UK. But this total view doesn’t tell the full story.

The UK’s experienced a fair share of weak GDP growth in recent years, largely due to its economy’s heavy exposure to revenue-light banks and, likely more significantly, government fiscal austerity. This austerity program likely carries an adjustment period in which short-term economic performance can be—and seemingly has been—impacted.

A core tenet of the UK’s austerity program is to rely more heavily on the private sector and exports to backfill government spending’s role over time. Given the eurozone’s ongoing travails, many across the pond fear the exports leg is in considerable jeopardy.

And to be sure, if a sudden shattering of the single currency occurred or a eurozone-born financial panic erupted, it’s likely the UK would be materially affected. But given eurozone politicians’ long-demonstrated resolve to maintain the currency and the ECB’s actions targeted at shoring up the financial system, neither appears a likely outcome in the near future. More likely is either a continuation of weak eurozone growth or possibly a eurozone recession.

Which leads me to a question: Which economy do you have more confidence in, Germany or Greece? Perhaps the answer seems ridiculously obvious. But the broader point behind the question seems less so, at least from my readings of economic and financial news coverage.

If one focused exclusively on aggregate figures—like the fact the eurozone consumes roughly 45% of UK exports, the concern is understandable. But herein lies a point many miss: Stripping away the eurozone-level focus, data show significant variation in UK export share.

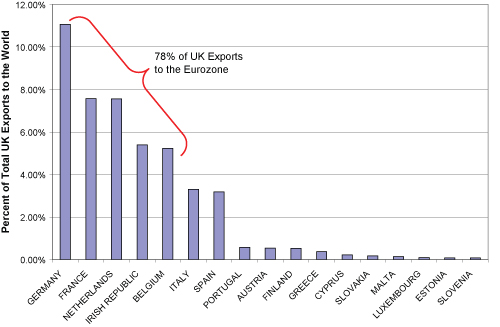

Exhibit 1: Eurozone Nations’ Share of Total UK Exports

Source: UK Office of National Statistics, 1/1/2011 through 10/31/2011.

Of the aggregate eurozone’s large share, over three-quarters of UK exports in 2011 through October were sent to Germany, the Netherlands, France, Ireland and Belgium. Over half to the first three. In fact, Germany alone accounts for a greater share of UK exports than the bottom 12 eurozone nations combined.

While domestic economic data have been quite mixed of late in many eurozone nations, it’s again pertinent to recall the currency bloc isn’t one uniform nation. Swapping individual currencies for a single one doesn’t change all dynamics contributing to economic growth—laws, political considerations, macroeconomic policy, domestic industry, competitiveness and more. (Pretty intuitive. After all, who chose Greece over Germany as a country they have more confidence in?)

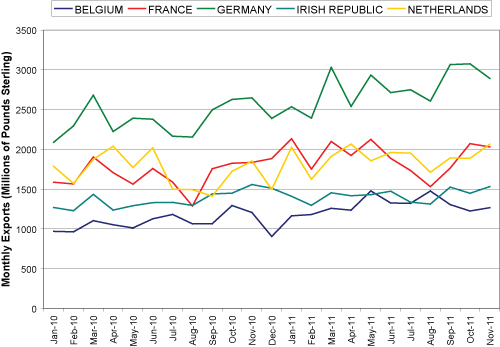

Recent eurozone data—even January’s accelerating, expansionary PMI—illustrate these differences. But should pan-eurozone slowing resume—even contraction occur—a critical point to consider would be the degree to which individual nations are impacted. It’s true some recent data from Germany (et al) haven’t been robust. But they’ve not been Grecian either. And as shown in Exhibit 2, trade with the top five nations, while showing volatility, hasn’t fallen off a cliff.

Exhibit 2: UK Exports to the Top Five Eurozone Partners

Source: UK Office of National Statistics, 1/1/2010 through 11/30/2011.

Some argue the -1.5% dip in November exports from the UK augurs a deeper export downturn ahead, presumably tied to weak eurozone demand. But economic data are often counterintuitive, and that seems at work in November’s report, too—pacing the £395 million monthly dip was a £300 million dip in silver exports to India. (And we’d not get carried away extrapolating that forward—trade is a highly volatile economic metric.) Exports to the eurozone’s 17 nations rose month-over-month.

Assessing the degree to which a eurozone recession could impact the UK through trade requires a more granular view than eurozone-level data permit. Simply, the eurozone doesn’t import anything from the UK. The 17 member nations do—but to widely varying degrees.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics On Fires and GDP2026-07-30

-

Economics Quick Hit: Durably Broad-Based Growth2026-07-29

-

Market Analysis On the Chop in the Oil Market2026-07-29

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today