Personal Wealth Management / Interesting Market History

An Underappreciated Lesson From 1929’s Crash for Investors in 2019

Despite short-run volatility, equity markets are more resilient than most investors seem to think.

Late last month, financial headlines “celebrated” an infamous anniversary: the 90th anniversary of Black Thursday, the 1929 Crash. Some used the date to muse on how markets today compare to those from nearly a century ago —and whether a crash looms. In our view, the better lesson to draw from such a distant milestone: It is a reminder of stocks’ resiliency—and why we think they should likely be a core part of long-term, growth-oriented investors’ financial plans.

Because of its severity and magnitude, the 1929 – 1932 bear looms large in market history—and the October crash seems like an obvious inflection point (though US markets’ actual pre-Great Depression peak came a month earlier). To capture the mood immediately post-Crash, here is a snippet from The New York Times’ coverage:

Wall Street was a street of vanished hopes, of curiously silent apprehension and of a sort of paralyzed hypnosis yesterday. Men and women crowded the brokerage offices, even those who have been long since wiped out, and followed the figures on the tape. Little groups gathered here and there to discuss the falling prices in hushed and awed tones. They were participating in the making of financial history. It was the consensus of bankers and brokers alike that no such scenes ever again will be witnessed by this generation. To most of those who have been in the market it is all the more awe-inspiring because their financial history is limited to bull markets.[i]

But as dramatic as the crash was, many saw it as a fleeting one-off—not the beginning of a horrific bear history now knows it as. Just one month later, The New York Times noted:

The feeling yesterday among bankers, as among other members of the financial community, was one of relief from the strain of the last three weeks. The events of the day, including the announcement from Washington of a tax reduction, the brisk rally in stock prices, the reduction in the local rediscount rate and the further heavy drop in brokers’ loans, all contributed to produce a distinctly optimistic viewpoint.

Sentiment had shown a distinct improvement on Wednesday evening, despite the further decline in stock market prices that day, but it was not until yesterday that bankers were willing definitely to advance the opinion that a turn for the better had arrived.[ii]

The losses during the 1929 – 1932 bear were epic, as the S&P 500 plunged -83.7%, coinciding with the massive economic downturn.[iii] Including reinvested dividends, stocks needed more than 15 years to reach pre-1929 levels—even longer if you exclude dividends. Part of that is the sheer magnitude of the drop, but two wallops also truncated the recovery and started a new bear market. The first: The Fed doubled reserve requirements in 1937, which encouraged banks to slash lending and raise capital—starving the economy of credit. The second was World War II’s storm clouds gathering in 1938 and 1939. The 1929 – 1932 bear’s unique combination of huge magnitude coupled with subsequent double-shocks vault it to the front of investors’ collective psyche as the gold standard of crashes. Yet stocks have endured plenty of other bear markets since then—and none were anywhere near as bad.

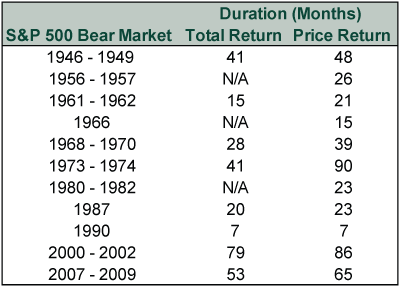

First, consider: That 15-year stretch—more than 185 months—stocks needed to claw back to prior peak levels is the anomaly, not the rule. Here is how long it took the S&P 500 (which we use for its lengthy history) to get back to the prior bull market’s peak following bear markets.[iv]

Exhibit 1: Stocks’ Climb Back to Prior Peaks

Source: Global Financial Data and FactSet, as of 11/7/2019. S&P 500 Index Price Level Index and S&P 500 Total Return Index, 5/29/1946 — 3/14/2013. Note: S&P 500 Total Return data are monthly until 1/2/1988. For the bear markets starting in 1956, 1966 and 1980, the S&P 500 Total Return Index did not breach the -20% threshold commonly demarking a bear market.

Moreover, focusing on bears overlooks the underappreciated power of bull markets. Stocks’ long-term average return is about 10% annually—a number that includes bears.[v] But if you strip out those bears, bull markets’ average annualized return more than doubles to about 21%.[vi] Also, starting in the postwar era, S&P 500 bull markets’ average cumulative return is 149% compared to bear markets’ -34%.[vii] Bulls also tend to last longer, with an average duration of 57 months, eclipsing bear markets’ 16.[viii] We aren’t saying these numbers tell you how future market cycles will look, as past performance isn’t indicative of future returns. Nor are we advocating a pure buy-and-hold approach that makes no attempt to mitigate a bear’s bite—if you know something others don’t that leads you to believe a bear market is highly likely developing, taking defensive action can help. But even if you never do that successfully, history shows stocks find a way to come back from even the most brutal bears.

To reap those gains, though, you must be invested and participate in bull markets. Having the discipline is straightforward in theory but difficult to practice. Exhibit A: investors’ experience during history’s longest bull market—the present. Several corrections (short, sentiment-driven downturns of -10% to -20%)—not to mention myriad smaller pullbacks and day-to-day market volatility—have tested investors’ patience. Besides normal short-term downturns, recent flattish periods stir worries over whether the bull’s days are numbered. Investors must contend with numerous external pressures, too. Headlines constantly lament seemingly endless threats to the bull: slowing economic growth; removal of policymakers’ “stimulus”; topsy-turvy politics; and allegedly crushing debt, to name a few. Nothing about staying invested during a bull market is easy—especially one that is arguably the least-loved in the postwar era.

Ultimately, though, the decision to own stocks is an affirmation of the belief that innovative people—driven by profit motive and encouraged by free markets—will continue to find ways to persevere despite all the obstacles. While another bear will happen—and we think it makes sense to prepare yourself mentally and emotionally now, during a bull—don’t allow that fear deter you from owning stocks today. If you need long-term growth for some or all of your portfolio to increase the chances you reach your investment goals, avoiding stocks during a bull market can be a very costly decision.

[i] Source: “Looking Back at the Crash of ’29: Then, as Now, a New Era,” Staff, The New York Times, published 10/15/1999. Date accessed: 11/5/2019. https://archive.nytimes.com/www.nytimes.com/library/financial/index-1929-crash-2.html

[ii] Source: “Banking Circles See Turn for the Better,” Staff, The New York Times, published 11/15/1929. Date accessed: 11/7/2019.

[iii] Source: Global Financial Data, as of 11/6/2019. S&P 500 Total Return Index, monthly returns, August 1929 – June 1932.

[iv] Source: Ibid.

[v] Source: FactSet, as of 1/10/2019. Annualized S&P 500 Total Return from 12/31/1929 – 12/31/2018.

[vi] Source: FactSet, as of 1/10/2019. Annualized S&P 500 Price Index return from 12/31/1929 – 12/31/2018. Figure does not include returns from current bull market.

[vii] Ibid.

[viii] Ibid.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-17

-

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today