Personal Wealth Management / 2020 Election

And Then There Were Four

A post-Super Tuesday lay of the land.

Super Tuesday is in the books, and it will forever be known as the day an underperforming candidate broke through: Yes, Representative Tulsi Gabbard finally won her first delegate. She remains in the race. Michael Bloomberg, who at last count won 12 yesterday, does not. Senator Elizabeth Warren, who so far can claim 26 of the 1,357 delegates on offer yesterday, is taking time to consider her future, according to her staffers. So while four candidates officially remain in the race as we write, this looks like a two-horse contest between former Vice President Joe Biden and Senator Bernie Sanders. We don’t know who has the inside track. We don’t know whether either will reach the convention with a majority of delegates. We don’t know who the nominee will be. And we certainly don’t know what will happen in November. Neither do markets, which means we may be in for more wobbles as uncertainty ebbs and flows over the next few months. However, once we have a nominee and markets can start handicapping November’s outcome, falling uncertainty should provide stocks a tailwind, resulting in a typically back-end loaded, positive election year.

Like every election year, 2020 has unique quirks and details, but in many ways it is a typical election year. It has started off with disappointing returns and increased volatility amid political uncertainty (with a side of infectious disease). If it continues behaving like a typical election year, we should see returns improve as the race narrows and markets can weigh probabilities instead of fear-inducing policy possibilities. That day may be hard to see now, with theatrics still dominating the headlines, but give it time. Even chaotic races eventually come into focus as the conventions wind down.

At a sociological level, Super Tuesday yielded a number of juicy stories. There was Biden’s back-from-the-dead win in 10 of 14 states, including mighty Texas. There was the “Stop Bernie” weekend dropout wave, in which Pete Buttigieg and Amy Klobuchar quit the race to endorse Biden. There was Bloomberg’s expensive flop, which amounted to an estimated $800 million of privately funded fiscal stimulus for Super Tuesday states. There was Warren placing a distant third in the state she represents in the Senate. There was the underperformance of House primary challengers funded by Alexandria Ocasio-Cortez’s PAC. There was the low turnout among young Sanders supporters which, surprisingly, we haven’t seen anyone tie to the coronavirus. There was the mystifying fact that Gabbard has not yet dropped out. There was the widespread call for do-overs from early voters frustrated over casting their ballot for someone who dropped out at the last minute. These are all fascinating. But we do market commentary, not sociology, so we won’t discuss them.

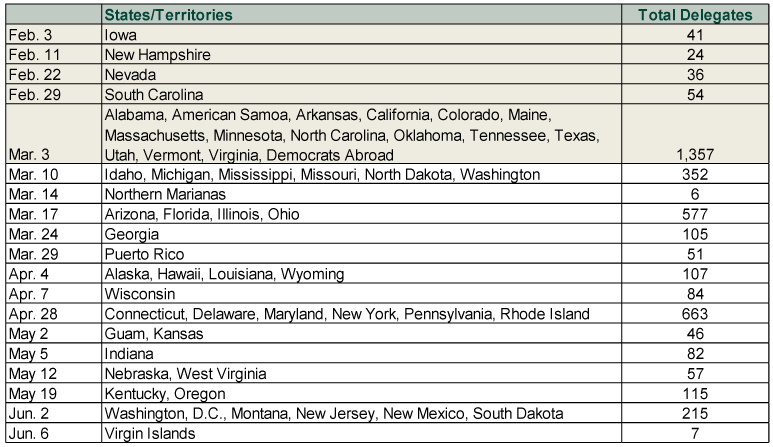

In an ordinary election year, this would be the point in the race where investors could start zeroing in on a likely nominee. But this is not an ordinary election year. Nearly 30 people entered this race at various points—with a high of 25 of them seeking the nomination at a time. Of them, seven have won delegates. The Associated Press estimates candidates not named Bernie or Joe have a combined 145 delegates. That is narrower than the margin between Biden and Sanders, which AP estimates at 65 (553 for Biden, 488 for Sanders) as we write midday Wednesday. The Democratic Party awards all delegates proportionately—no winner-take-all states. Therefore, it remains mathematically possible that neither candidate will reach Milwaukee with the 1,991 delegates required to secure the nomination on the first ballot. As Exhibit 1 shows, the primaries and caucuses completed thus far will decide just 38% of pledged delegates. If Biden and Sanders split the vote from here, we will have a contested convention.

Exhibit 1: Delegates Divided

Source: The New York Times, as of 3/4/2020.

One reason this is so impossible to call: Each candidate’s fortunes depend on the second, third and fourth preferences of all those voters who initially preferred other candidates. Will Buttigieg’s supporters follow his endorsement to Biden? Or will they flip to Sanders, given Buttigieg’s policies were left of Biden’s? Will Warren’s supporters switch to the other candidate on the left edge of the spectrum? Or will they be turned off by the Bernie Bros’ behavior and go for Joe? In addition to about a dozen other permutations of this question, there is also the wild card. Will someone make a gaffe they can’t recover from? What about health concerns?

None of these questions are answerable right now. Forgive the tautology, but we won’t know the winner until we know the winner. In the meantime, the momentum will probably change hands a few more times, which could affect markets. While the coronavirus hogged all the attention as stocks dove last week, Sanders’ ascension was lurking in the background, adding a potential socialist nominee to investors’ list of worries. Stocks improved this week alongside Biden’s fortunes. If we get another Sanders surge, market wobbles wouldn’t surprise. Then again, maybe stocks got it out of their system already—short-term volatility is unpredictable. But being mentally prepared for ups and downs beats the alternative, in our view.

Once we have a presumptive nominee, uncertainty should start easing. November polls will no longer feature hypothetical matchups that voters haven’t given much thought to. State polls will hint at who is resonating the strongest with swing state voters. Congressional races will come into focus, giving investors a sense of how much gridlock they can expect. Perhaps most importantly, campaign rhetoric should moderate as both final challengers start trying to appeal to the majority of the country instead of the party base. Radical proposals should get watered down or fall by the wayside, helping investors get over earlier jitters about a wealth tax, Medicare for All and other contentious policies. All of this should help investor sentiment improve.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

-

Expert Commentary This Week in Review | Energy Markets, Fed Meeting, Earnings Reporting

2026-03-20

2026-03-20 -

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today