Personal Wealth Management / Market Analysis

As Oil Prices Rise, So Do Theories

Oil prices have risen lately, resurrecting some old theories regarding their impact.

Recently, rising oil prices have spawned headlines warning of an impending price shock—or suggesting investors are simply complacent regarding risks posed by higher oil prices.

We’ve previously documented the lack of evidentiary support for the theory high oil prices on their own automatically sap stocks, so we’ll not rehash that here. But some take a slightly different angle on rising oil—claiming consumer spending is negatively affected, thus impacting economic growth. We have myriad quibbles with this demand-side theory. For example, if it’s true rising oil prices directly hammer consumer spending, then shouldn’t falling oil prices buoy sales? But that’s not the historical norm.Oil prices rose higher than current levels in early 2011 and similar fears swirled. Yet retail sales (excluding gasoline station sales) fell in only one month of the year. Which month? May—when oil prices also fell. Now obviously, that's just one year. But the reality is it isn't so unusual to see rising oil prices coupled with economic growth.

An often overlooked point in the frequent media handwringing over rising oil is it’s an economically sensitive substance—like many basic commodities. Increasing demand brought by expanding economies typically does manifest itself in higher prices (to the extent demand growth outpaces supply growth). Consider 2001’s less-than-$20-per-barrel oil—which grew to about $100, all while the economy grew. (Price movement driven in no small measure by Emerging Markets’—particularly Asia’s—sharp consumption growth.) And last year’s macroeconomic fear-driven correction applied to both stocks and oil. Yet today, as data have repeatedly shown global economic growth, both stocks and oil have staged comebacks. Not very surprising, keeping oil’s economic sensitivity in mind.

But some will argue another factor is in play—Iran. Folks postulate if tensions develop into war with Iran, oil prices will spike—a shock to the economy. While it is possible geopolitical concerns of a major, surprising nature could impact both oil and the economy, some perspective is in order.

If you’ve heard of Iran tensions—and most have, considering they’ve been near-endlessly discussed on television—then chances are major oil market participants have, too. These producers, traders and companies consuming vast quantities of oil likely aren’t just sitting on their hands wondering if war will develop. They’ll likely hedge—an action some decry as speculating. But what those speculators are actually doing is moving oil supply from a time of plenty—now—to when it’s feared it won’t be as plentiful. That may explain some of the recent price movement (though discounting the economic aspects would be a mistake). It’s a theory—but not an unreasonable one—that oil markets are fully capable of discounting the risk of war in advance of bombs falling or naval blockades. Exhibits 2 and 3 provide a few historic examples of this.

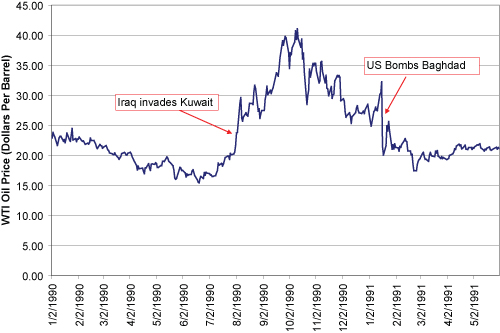

Exhibit 2: West Texas Intermediate (WTI) Crude Prices—1/1/1990 – 6/30/1990

Source: Federal Reserve Bank of St. Louis.

As shown, when Kuwait was invaded and the US became more engaged, oil prices rose—likely in part because of traders discounting threats to Saudi supply, war in general, etc. But oil prices fell sharply at the very time bombs fell on Baghdad. (Also note: The increase in oil prices had little to do with the 1990-1991 US recession—which began before oil prices rose.)

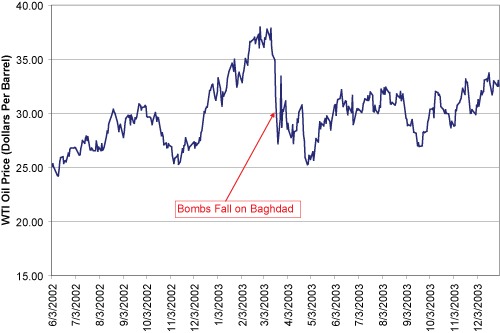

Exhibit 3: West Texas Intermediate (WTI) Crude Prices—6/1/2002 – 12/31/2003

Source: Federal Reserve Bank of St. Louis.

Similarly, 2003’s tensions were well known before war developed, so neither case was very surprising. Thus, when military action occurred, oil prices fell. They didn’t surge, spike or even rise.

Theories abound regarding oil prices—how they happen, why, who’s to blame and what the effect really is. But when you actually break down the historical record, data may tell a different story from what you’re hearing.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Oil prices will be lower in 6 months than when Iran conflict began, Ken Fisher argues2026-03-12

-

Market Analysis Rounding Up Odds and Ends From Global Energy Developments2026-03-11

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

-

Economics Pain at the Pump Won’t Hurt the Global Economy2026-03-10

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today