Personal Wealth Management / Economics

August’s Dog Day PMIs

Global growth may be uneven, but stocks don’t need perfection.

August flash purchasing managers’ indexes (PMIs), released last Friday, showed the developed world largely continued recovering from its lockdown-driven recession. Yet many pundits focused on perceived pockets of slower growth. True, PMIs didn’t improve everywhere, but in our view, that shouldn’t matter much for forward-looking global stocks.

IHS Markit’s flash PMI surveys—preliminary releases based on around 85% – 90% of expected responses—are an early glimpse at each month’s economic activity. PMIs essentially ask firms whether different kinds of business activity—e.g., output, new orders, backlogs and employment—improved or deteriorated during the month. A reading of 50 indicates no change. Above that implies expansion, although PMIs don’t say anything about the amount of change—how much activity rose or fell. They speak only to its breadth—how many firms saw activity grow or shrink in the month.

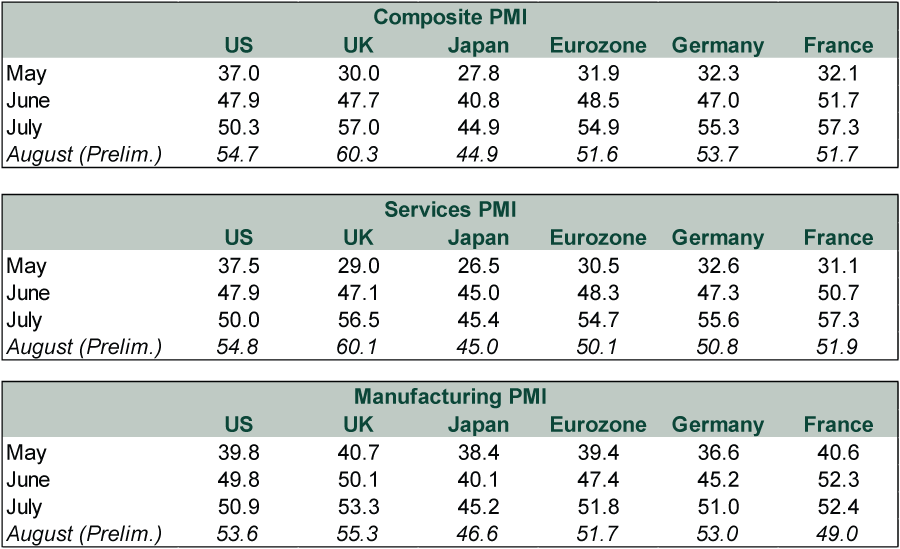

Except for export-dependent Japan, August PMIs show major developed economies continued expanding. Composite PMIs, which combine services and manufacturing, signaled a second straight month of growth in the US, UK and eurozone. (Exhibit 1)

Exhibit 1: Major Economy PMIs

Source: IHS Markit and FactSet, as of 8/21/2020.

Sharp-eyed readers may note UK and German composite PMIs exceed each of their services and manufacturing PMIs. This is because IHS Markit uses only the output subindexes to calculate the composite—a more limited look than headline services and manufacturing PMIs, which incorporate output, new orders, employment and others.

With that quirk in mind, US and UK services PMIs surged this month. This is great news for their economies. Services makes up about 70% of the US economy and 80% for the UK.[i] An increasing majority of services-sector firms reporting growth is good evidence recovery is taking hold. This is especially noteworthy for the UK, considering August is the first full month with the vast majority of personal services back in action post-lockdown. It also indicates new restrictions in the north of England didn’t present massive headwinds. Meanwhile, both countries’ manufacturing PMIs also showed more widespread growth.

In contrast, while all eurozone PMIs except for French manufacturing remained above 50, all but German manufacturing ticked down. These low-50s readings still indicate ongoing expansion, just not as broadly as in July. We won’t argue this indicates everything is rosy, but we also wouldn’t be discouraged—no recovery occurs in a straight line. Plus, in this case, a slower-but-still-expansionary reading could mean most businesses held steady after an initial burst of pent-up demand, which is hardly bad news. Also encouraging? Despite limits on cross-border demand, IHS Markit’s press release noted total new orders increased—good news, as today’s orders are tomorrow’s production, making new orders a PMI’s primary forward-looking component.

Yet the commentary surrounding August’s eurozone PMIs was dour. Headlines used words like “stumble,” “falter” and “losing steam” to describe the recovery. But according to IHS Markit’s press release commentary, the main cause of the headline downticks in services and manufacturing was falling employment—a late-lagging indicator, in our view. Firms typically base personnel decisions on business conditions weeks or months past. When business turns south, they let workers go as a last resort, given the time and costs to train them. Then, when business prospects brighten, firms are often reluctant to hire until it is necessary to meet company objectives. With a laser focus on the bottom line, firms tend to run lean for several quarters following a downturn—hence, why many see recoveries as “jobless.” Yet weak employment figures—in PMIs or official job reports—have never prevented recovery before.

Besides, employment’s detraction from eurozone PMIs wasn’t too surprising given member-states’ extensive use of “short-time work” schemes. Rather than remove workers from payrolls (permanently or temporarily) in a downturn, eurozone firms tend to cut hours and pay for their employees while governments supplement the lost income. As these support programs expire or businesses conclude their staffing too-far exceed actual work requirements, layoffs eventually happen—at a delay from America. We may be witnessing this in the eurozone PMI data. But we think this says little to nothing about where the economy heads from here—it shows you where it was.

Travel restrictions likely also contributed to the eurozone’s downbeat services PMI, underscoring how much economic recovery depends on reopening progress. However, stocks are well aware of this and are likely looking past it. Since stocks see about 3 – 30 months ahead—and toward the far end of that range early in bull markets—they shouldn’t hinge on instantaneous return to normal policy. Simply being able to envision eventual normalcy should suffice, regardless of the path there.

COVID upticks and reopening hiccups or not, don’t lose sight of the bigger, longer-term picture. After Q2’s GDP wipeouts, data show most of the developed world is building back. It is and will be uneven, but what matters more for markets is the general trend and where things are likely to be one, two or three years from now. Wiggles along the way may unnerve sentiment, but that is normal in any new bull market, part of the proverbial wall of worry stocks climb. Many remain on hair-trigger alert for a deep second leg down. But preliminary August PMIs shouldn’t ring any alarm bells. Even if less-broad growth translates to slower growth, that is still growth, which seems fine enough to continue beating dreary expectations. Moreover, slowing activity in non-employment categories seems more tied to fitful reopenings than new closures. A second deep contraction—knocking stocks—would likely require another draconian lockdown. We see no evidence that is about to occur.

While we may not get back to pre-lockdown activity levels as quick as most would like—and investors should expect interruptions along the way—widespread pessimism over overall ok PMI releases shows plenty of room for even modest results to generate positive surprise.

[i] Source: US Bureau of Economic Analysis and UK Office for National Statistics, as of 8/25/2020.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

-

Interesting Market History COVID-Panic’s Lockdown-Low Anniversary2026-03-25

-

Market Analysis The Golden Paradox2026-03-24

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today