Personal Wealth Management / Market Analysis

“Austerity,” Lending and the UK Economy

Spending cuts are often blamed for the UK’s recession, but data suggest regulatory uncertainty plays a much bigger role.

Ever since UK Chancellor of the Exchequer George Osborne launched his deficit reduction program, most observers assume the UK economy’s been mired in austerity—and the IMF, the UK’s Office for Budget Responsibility, the National Institute of Economic and Social Research and even Nobel Prize-winning economists all agree this austerity is responsible for the shallow recession that began in Q4 2011.

Now, austerity seems to mean different things to people—in many nations, sensible supply-side economic reforms, like privatization of state-owned assets and enterprises, are taken for austerity. In the strictest definition though, austerity means a combination of tax increases and spending cuts, bringing both sides of the deficit closer together.

In the UK, the deficit has fallen since 2010, both in absolute terms and relative to GDP, suggesting at least some degree of traditional austerity. And the UK has hiked taxes, which is likely impacting economic growth (after all, the more you tax something, the less you get of it). But much of the commentary I’ve seen assumes sweeping spending cuts as well and suggests recession will deepen unless the government eases up and spends more.

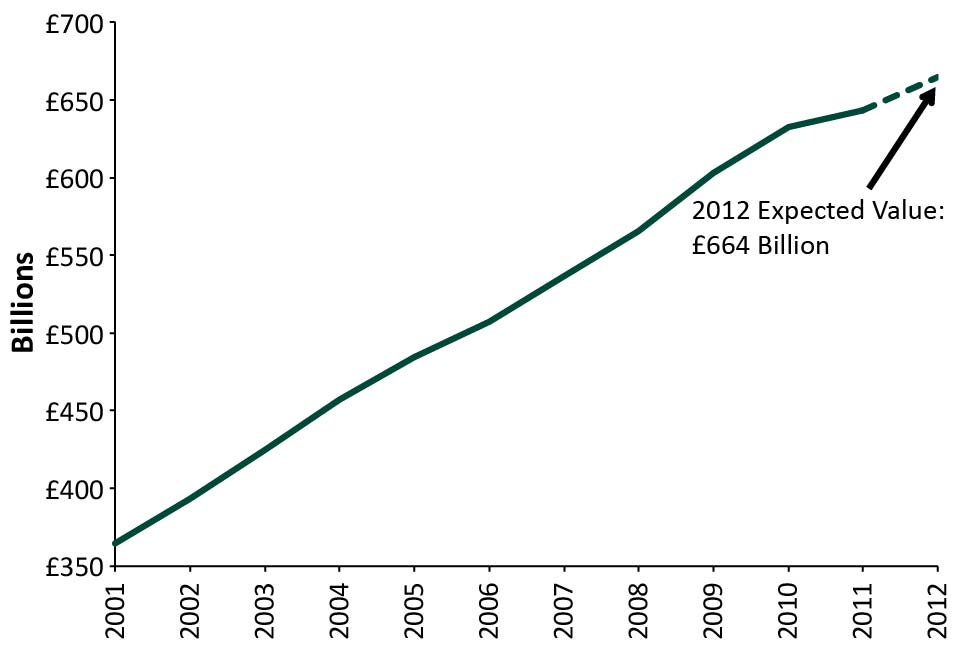

Trouble is, there’s scant evidence of growth-crushing spending cuts—in fact, total spending has risen, as shown in Exhibit 1.

Exhibit 1: UK Government Spending

Source: HM Treasury, as of 10/17/2012.

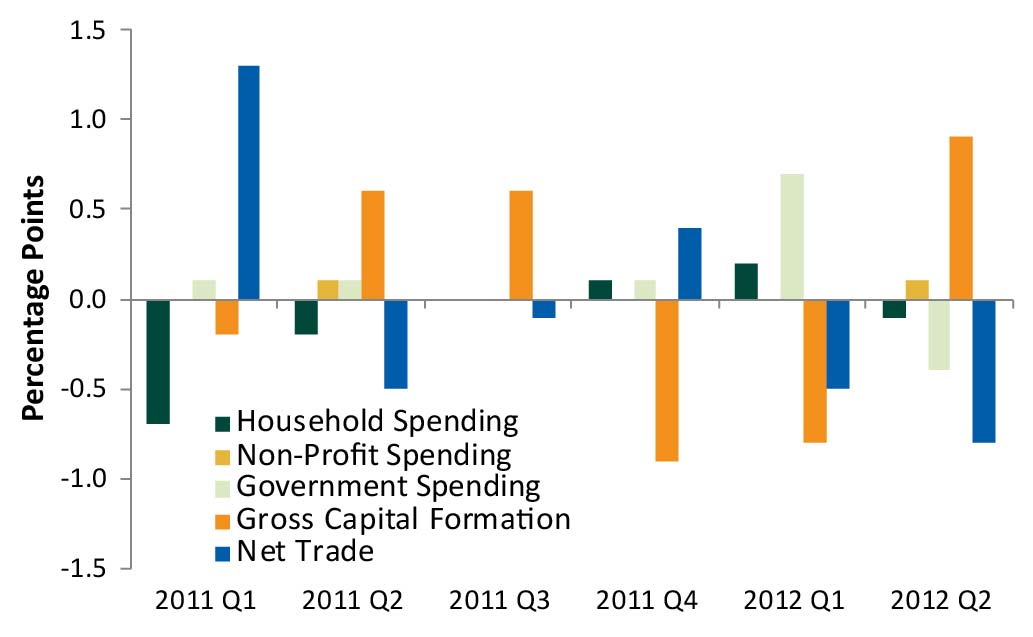

Nor have government components of GDP much detracted from headline growth. Real government consumption has risen in each of the past 15 years (as measured in 2009 GBP).[i] Government consumption did fall a bit in Q2 2012—its first contraction since Q4 2010—but at £84 billion was still the second-highest quarterly spending figure ever.[ii] As shown in Exhibit 2, government spending was a positive contributor to headline growth for the recession’s first two quarters—and over the entire recession, the private sector and trade have been bigger detractors.

Exhibit 2: Contributions to UK GDP Growth

Source: Office for National Statistics.

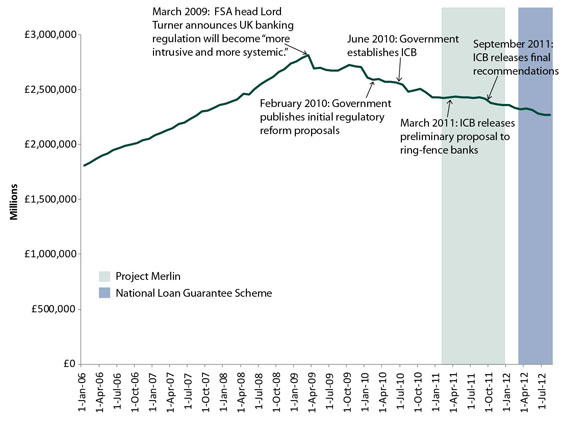

So, why isn’t the private sector growing? As mentioned above, tax hikes likely play a part. But here’s another large reason: Banks aren’t lending much. Broad lending’s fallen since March 2009, and two government programs aimed at boosting it—2011’s Project Merlin and 2012’s National Loan Guarantee Scheme—haven’t helped. Nor has the Bank of England’s quantitative easing.

Regulatory headwinds appear to be the primary culprit. Lending peaked right when Lord Adair Turner—the head of the UK’s financial regulatory, Financial Services Authority (FSA)—published a critique of UK regulation during the global financial crisis. In the report, he concluded existing regulation wasn’t “aggressive enough in demanding adjustments to business models,” and he promised a “more intrusive and more systemic” new approach.[iii]

Since then, UK banking regulation has remained mired in uncertainty. In 2010, Chancellor George Osborne announced FSA will cease to exist in 2013, with three new entities assuming supervisory duties: Prudential Regulatory Authority, which will “promote safety and soundness of financial firms;”[iv] Financial Conduct Authority, which will oversee consumer protection; and the Bank of England’s new Financial Policy Committee, which will regulate all other aspects of financial services. Shortly thereafter, the government established the Independent Commission on Banking (ICB) to recommend policy changes to “promote financial stability.” After spending over a year consulting with banks, regulators, academics and market participants, the ICB recommended several tougher regulations in September 2011—including “ring-fencing” banks’ retail banking operations (a complicated, expensive process) and increasing capital requirements above Basel III international standards.

As shown in Exhibit 3, the murkier the regulatory landscape became, the further lending fell. To be sure, other factors likely played a role—loan growth fell globally in 2008 and early 2009—but UK lending is still falling even as the rest of the world is recovering. (Including the US, where lending continues to rise.)

Exhibit 3: UK Bank Lending

Source: Bank of England. Monthly amounts outstanding of M4 lending excluding securitizations (monetary financial institutions’ sterling net lending excluding securitizations to private sector), seasonally adjusted, 07/31/1982 – 08/31/2012.

When faced with the prospect of significant regulatory changes, banks tend to adopt a “wait and see” mentality—if they expect to need to raise significant capital to offset balance sheet risks in the future, they have incentive not to add risk in the present. Only the most creditworthy borrowers can secure financing, and many UK firms—especially small and medium firms—have been shut out of credit markets as a result. When firms can’t access credit, it’s exceedingly difficult to invest in new equipment, facilities, software, technology and the like—all of which would boost output.

In my view, the best UK stimulus wouldn’t be the Keynesian package the IMF and others argue for—simply easing banks’ regulatory burdens would likely do wonders. While the UK government did water down many of the ICB’s proposals—including the capital requirements—other pressures remain as the new regulatory regime prepares to take over (and threatens to arbitrarily set leverage ratios and mandate banks build counter-cyclical capital buffers). Clarifying these agencies’ powers, easing capital requirements and giving firms more control over business models would enable them to lend much more freely—something the entire economy would benefit from.

[i] Source: “The Turner Review: A Regulatory Response to the Global Banking Crisis;” Lord Adair Turner, Financial Services Authority, March 2009.

[ii] Source: “The Bank of England, Prudential Regulation Authority: Our Approach to Banking Supervision;” The Bank of England, May 2011.

[iii] Source: “Quarterly National Accounts, Q2 2012,” Office for National Statistics.

[iv] Source: “Quarterly National Accounts, Q2 2012,” Office for National Statistics.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Quick Hit: What to Make of Jobs Data’s Persistent Swings2026-04-07

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 30 - April 32026-04-06

-

Expert Commentary US Inflation, Fed Minutes, Consumer Sentiment | 3 Things You Need to Know This Week

2026-04-06

2026-04-06 -

Expert Commentary This Week in Review | Q1 Recap, Earnings Guidance, Elections

2026-04-03

2026-04-03

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today