Personal Wealth Management / Behavioral Finance

Beware Breakevenitis

We figure few investors bought stocks expecting flat returns, but after negativity some nevertheless fall prey to behavioral errors and sell at breakeven.

On the road to your investment goals, looking back at prior levels is no way to formulate a forward-looking strategy. Photo by ZenShui/Eric Audras / Getty Images.

One common, regrettable error many investors make in negative volatility's wake is selling when markets or their portfolios reach breakeven. And it is highly likely many will soon fall prey to what we not-so-affectionately call, "breakevenitis," given the steep rebound thus far from the correction's lowest point seen to date. If your goals or needs require equity-like returns, this is a perilous practice you should strive to avoid.

Behaviorally, humans are conditioned to see selling at breakeven as harmless or even positive-after all, prospect theory (aka, myopic loss aversion) states we are likely to feel the pain of loss more than twice as much as we appreciate an equivalent gain. The fear and pain of a volatile stretch gets seared into your brain, leading you to expect a redux in the near future. So the innately human urge is to breathe a sigh of relief, sell at breakeven and "get off the roller coaster." And you didn't lock in any losses, you were even!

But this is making a forward-looking decision-about where the market will go-exclusively on backward-looking information. It's a recipe for missed opportunity, and in investing, opportunity cost is money lost.

Yes, negativity may resume. That is always a possibility in the short term, and one equity investors must prepare for. There are no short cuts in which you get the upside and avoid negativity-none. And yes, there are even times selling at breakeven has historically been a benefit, but basing any decision about your asset allocation on an index level relative to some point in the past (high-water mark, round number, other arbitrary figure) is not a strategy likely to reap repeated success.

The following Exhibits illustrate how selling at breakeven after many recent periods of significant volatility would have been a costly move indeed, ranging from the Financial Crisis to corrections.

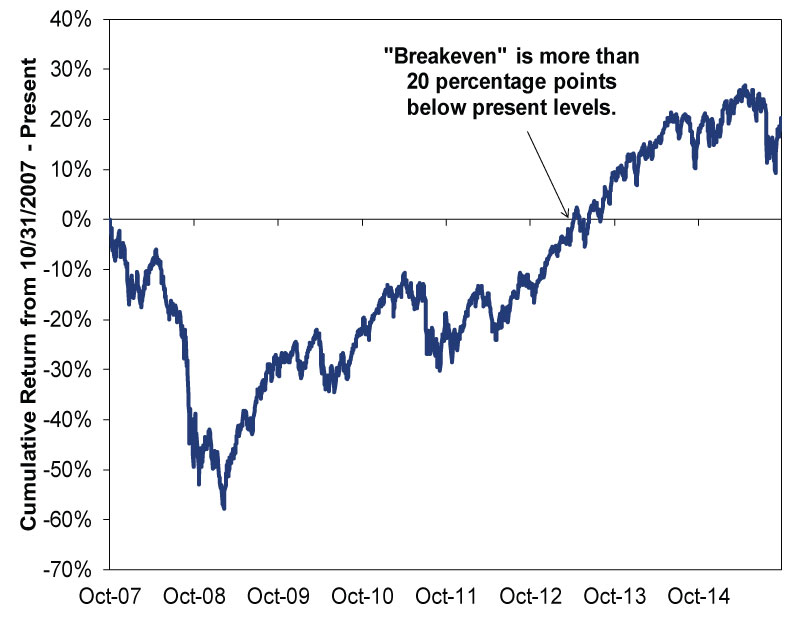

Exhibit 1: Breakevenitis After the Global Financial Crisis

Source: FactSet, as of 10/27/2015. Cumulative MSCI World return with net dividends, 10/31/2007 - 10/26/2015.

That is obviously an extreme example, considering it uses the financial crisis, the biggest bear market in the post-war era. If we look at corrections-short, sharp, sentiment-driven down moves exceeding -10%-selling at breakeven seems just as fruitless, if not more so.

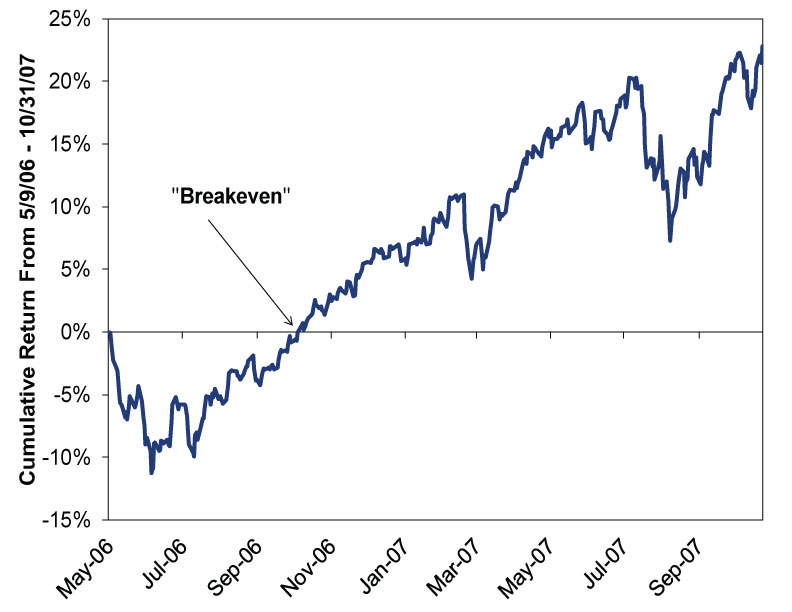

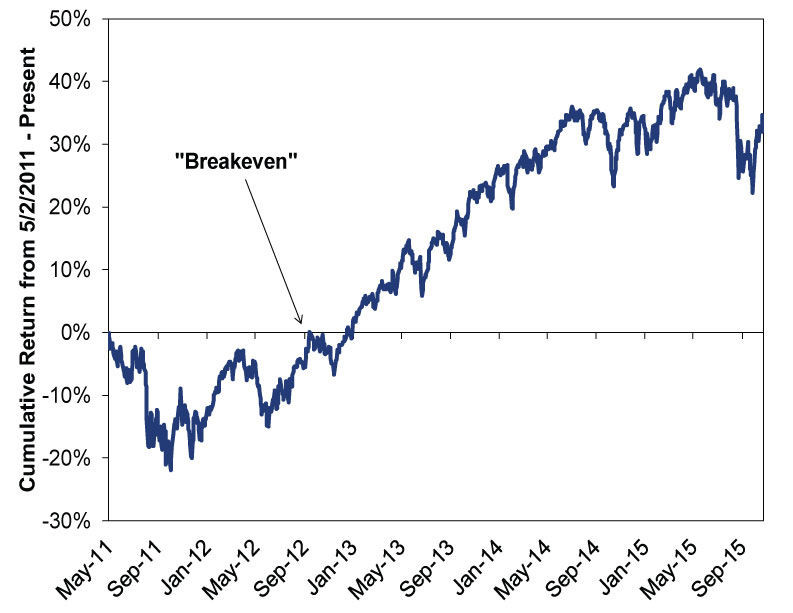

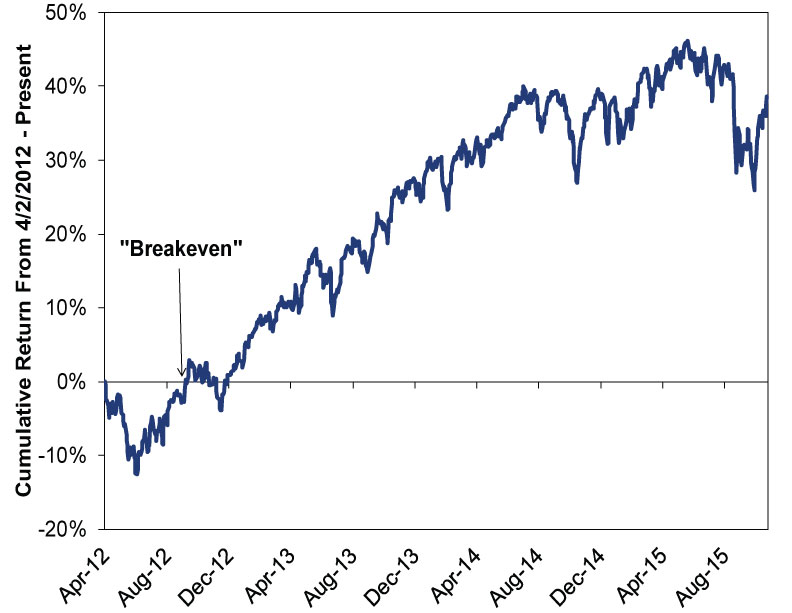

Exhibits 2 - 4 show the effect of selling at breakeven following selected corrections in recent market history.

Exhibit 2: Breakevenitis After 2006's Global Correction

Source: FactSet, as of 10/27/2015. Cumulative MSCI World Index returns with net dividends, 5/9/2006 - 10/26/2015.

Exhibit 3: Breakevenitis After 2011's Global Correction

Source: FactSet, as of 10/27/2015. Cumulative MSCI World Index returns with net dividends, 5/2/2011 - 10/26/2015.

Exhibit 4: Breakevenitis After 2012's Global Correction

Source: FactSet, as of 10/27/2015. Cumulative MSCI World Index returns with net dividends, 4/2/2012 - 10/26/2015.

We sincerely doubt any equity investor bought stocks expecting a return of zero, so it's odd some see this as the time to exit. If you are an investor with longer-term needs and goals commensurate with equity exposure, you should be in equities far more often than not. Deviating from a strategy likely to provide the longer-term returns you need should only be done when you have a unique insight that makes you believe a significant downturn-e.g., bear market-is likely at hand. Selling because you hit breakeven is your brain suffering the lagging effects of volatility's pain.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Rounding Up Odds and Ends From Global Energy Developments2026-03-11

-

Economics Pain at the Pump Won’t Hurt the Global Economy2026-03-10

-

Market Analysis Stablecoins Didn’t Eat the Treasury Bill Market2026-03-10

-

Economics Putting Choppy Labor Data in Proper Perspective2026-03-10

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today