Personal Wealth Management / Market Analysis

Big British Debt Saves the World, and Other Century-Old Stories

The story of three centuries' worth of UK debt shows why today's occasional debt doom-mongering is pretty far-fetched.

Actress Lady Tree poses with a War Loan advert to rally Britain's financial troops in 1917. That bond was redeemed Monday. Photo by Topical Press Agency/Getty Images.

Here is something that ordinarily wouldn't be big news: The UK redeemed about £1.9 billion in bonds Monday. But these weren't just any bonds. They were old. Really old. Issued in 1917 old. Paying them off has next to no impact on UK public finances (or markets)[i], but their legacy does provide a timely lesson for anyone worrying high debt will destroy the US or UK economies over time. Competitive economies can carry high debt loads for very, very long stretches without much (if any) ill effect.

Yes, I say that even though these bonds were redeemed. Officially they were paid off, but in reality they were rolled over-repaid with money raised from another bond issue. The 98-year-old bonds, known officially as the 3½% Conversion Loan, were open-ended, and the Brits have been on a quest to abolish all open-ended debt. So, like the ancient "4% Consol" redeemed in February, they were refinanced with fixed-maturity bonds, which come due over the next few decades. So the debt in question remains on the books, just in different clothes.

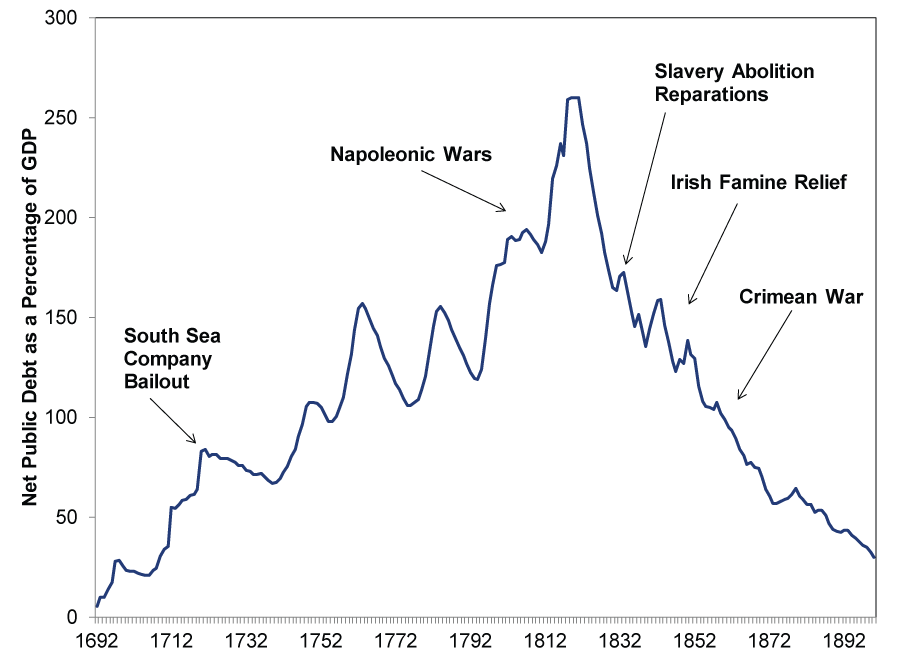

Now, on to the fun stuff. Our tale begins way back in 1720. The British Empire was the world's superpower, dominating other navies and commerce across the seven seas. Its flagship trading companies' stocks were off the charts, making would-be kings of Sir Isaac Newton and other speculators. Everyone wanted a slice of the East India, Mississippi and South Sea Companies-powerful monopolies folks were sure couldn't fail, and they were all-too delighted to blanket the Empire with new shares. The stock-buying frenzy drove a massive supply increase-the world's first IPO mania. No one noticed the South Sea Company was a poorly run shell game without a snowball's chance of turning a profit. Until, that is, management dumped their shares when they realized the game was up. Panic ensued. The government stepped in to prevent a full-on collapse, issuing bonds to fund the bailouts. Consider it an 18th century TARP. They never paid it back. Instead, in 1752, Prime Minister Henry Pelham converted the bonds into open-ended, interest-bearing securities. The consol was born.

Fast forward to 1803. Napoleon was rampaging through Europe and the Middle East. Britain declared war, and the Anglo-Allied armies spent 12 years fighting France's imperial forces across the Continent. War is expensive, so the government tapped its new favorite funding source, the consol.[ii] Charles Grey's government used consol money too, in 1833, to fund £20 million[iii] in reparations under the Slavery Abolition Act.[iv] Consols also funded Irish famine relief in 1847. Another £30-plus million[v] were issued in the mid-1850s to fund the Crimean War, giving new meaning to the Charge of the Light Brigade.[vi] They never paid it off.

But still, the British economy grew leaps and bounds. Britain dominated global trade, and it was the height of the Industrial Revolution. So even though debt kept rising, as a percentage of GDP, it was falling. By the time the 20th century dawned, things looked manageable.

Exhibit 1: UK Net Public Debt as a Percentage of GDP, 1692 - 1900

Source: UKPublicSpending.co.uk and history, as of 3/10/2015.

But then the Serbian nationalists shot the heir to the Austro-Hungarian Empire, Archduke Franz Ferdinand, and all those royal-blooded cousins who'd taken over Europe's empires started fighting each other-World War I. The British Empire was in deep and deep in the red by 1917, having burned through war bonds issued in 1914 and 1916. So they issued war bond number three, now known as the War Loan, which refinanced the 1914 and 1916 issues and raised an additional £845 million. It yielded 5% and carried the promise: "Unlike the soldier, the investor runs no risk."[vii]

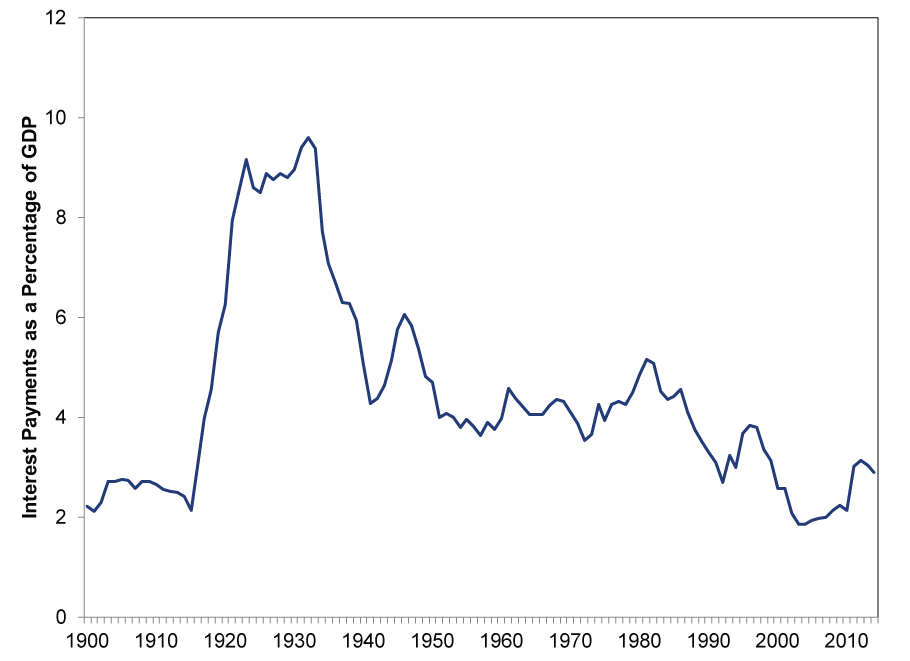

Except by 1932, the world was in the throes of the Great Depression, Britain's debt was reeling at 176% of GDP, and interest payments were nearing 10% of GDP. So then-Chancellor Neville Chamberlain, um, appeased[viii] financial markets by swapping the 5% War Loan for the open-ended 3½% Conversion Loan, hitting investors who'd believed the marketing materials about that sacrosanct 5%. I reckon he got the idea from his predecessor, Winston Churchill, who consolidated all the other debt mentioned here into that 4% Consol in 1927. Not one dime was paid off in the intervening decades, until last month.

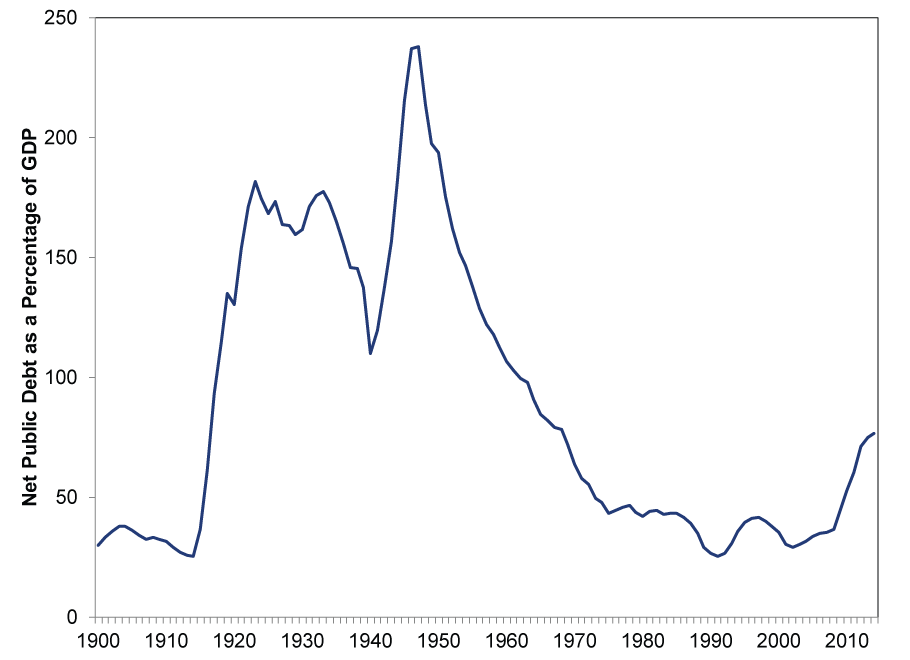

Yet Britain is thriving today! How? Because while total net public debt did this:

Exhibit 2: UK Net Public Debt, 1900 - 2014

Source: UKPublicSpending.co.uk, as of 3/10/2015.

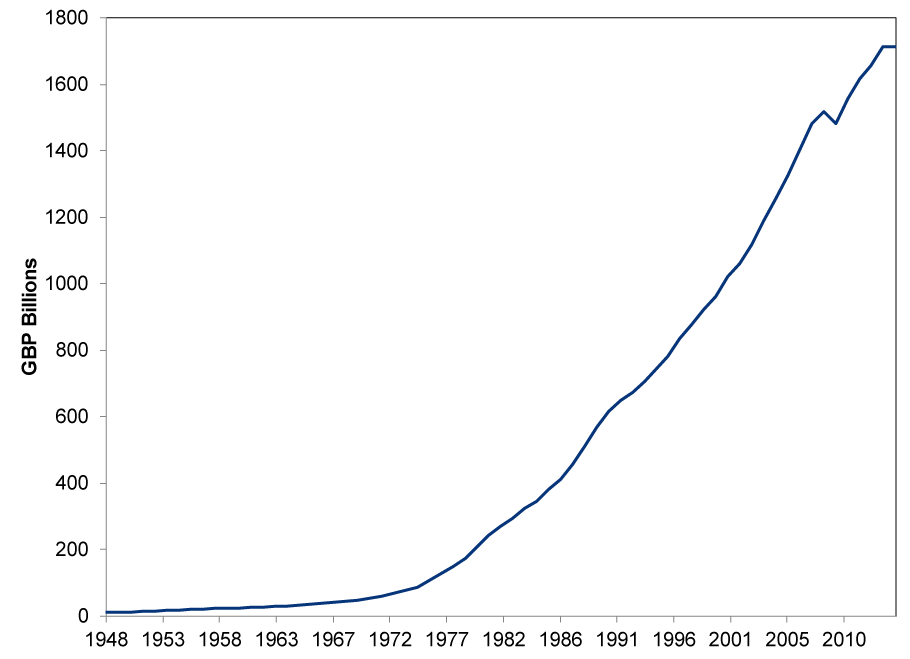

The UK's economy did this:

Exhibit 3: UK Nominal GDP[ix], 1948 - 2014

Source: FactSet, as of 3/10/2015.

So net public debt relative to GDP did this:

Exhibit 4: UK Net Public Debt as a Percentage of GDP, 1900 - 2014

Source: UKPublicSpending.co.uk, as of 3/10/2015.

And interest payments relative to GDP did this:

Exhibit 5: UK Interest Payments as a Percentage of GDP, 1900 - 2014

Source: UKPublicSpending.co.uk, as of 3/10/2015.

Nope, Britain never paid off most of that legacy debt-or debt piled on throughout the 20th century. They just grew out of it, shrinking the overall burden relative to the size of the UK economy. Debt isn't any more of an issue today than it was in 1720, 1752, 1812, 1833, 1855, 1917 or 1932. If anything, it's less burdensome and more affordable, even though in hard currency terms it's at all-time highs! And, with Monday's rollover in the books, UK debt just got about £15 million cheaper annually.[x] If Britain could handle all that and have a dynamite economy and stock markets, so can the US and Britain today. They aren't Greece.

Beat the Crowd, by Ken Fisher with Elisabeth Dellinger, is available for pre-order now. Order your copy today!

[i] The math here is tricky, but it looks like they'll save about £15 million annually on interest payments.

[ii] They also tapped Nathan Rothschild, but that is a story for another day. Or, just read The Rothschilds, by Frederic Morton.

[iii] That would be £1.7 billion today.

[iv] I have no data on whether he also used consols to fund a marketing campaign to name a certain blend of tea after himself. If he did, it was a sunk cost, because Earl Grey isn't trademarked and there is no evidence he ever received royalties.

[v] Over £2.4 billion today.

[vi] Apologies if it's too soon for a Crimean War pun. Also, watch the movie, which actually isn't much about the event but is a classic.

[vii] Securities laws then weren't what they are today. Government bonds, major global conflict or no, are not risk free.

[viii] Again, too soon, sorry.

[ix] Debt is serviced in nominal dollars, so inflation-adjusted GDP isn't appropriate in this context. But, if you're curious, real GDP skyrocketed, too.

[x] Judging from UK Treasury auctions conducted around when the old bonds were redeemed, interest payments will drop from about £66.6 million annually to just over £50 million.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Q2 US GDP’s Stealthy Strength2026-07-31

-

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31 -

Market Analysis Don’t Fret the EU’s Low Summertime Gas Storage Levels2026-07-31

-

Economics On Fires and GDP2026-07-30

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today