Personal Wealth Management / Market Analysis

Brazil’s Impending Impeachment Hangover

Brazilian markets seem at risk of suffering from weak oil prices and political disillusionment.

Brazil has been a bit of a Dickensian tale in recent years. In the last two years, it's been mostly the worst of times: The deepest and longest recession in generations; political scandals, including one that resulted in a sitting president's ouster; high inflation; Ryan Lochte.[i] Given this scenario, one might expect Brazilian stocks to have significantly underperformed the broader MSCI Emerging Markets Index. And for a time, this was true. From mid-September 2014 through late January 2016, the MSCI Brazil underperformed the MSCI Emerging Markets (EM) by more than 30 percentage points.[ii] But, since then, the worst of times has become the best of times for Brazilian stocks, up 87% since January 25 and outperforming EM by a whopping 59 percentage points.[iii] The question, however, is: Is this sustainable? In our view, the answer is no.

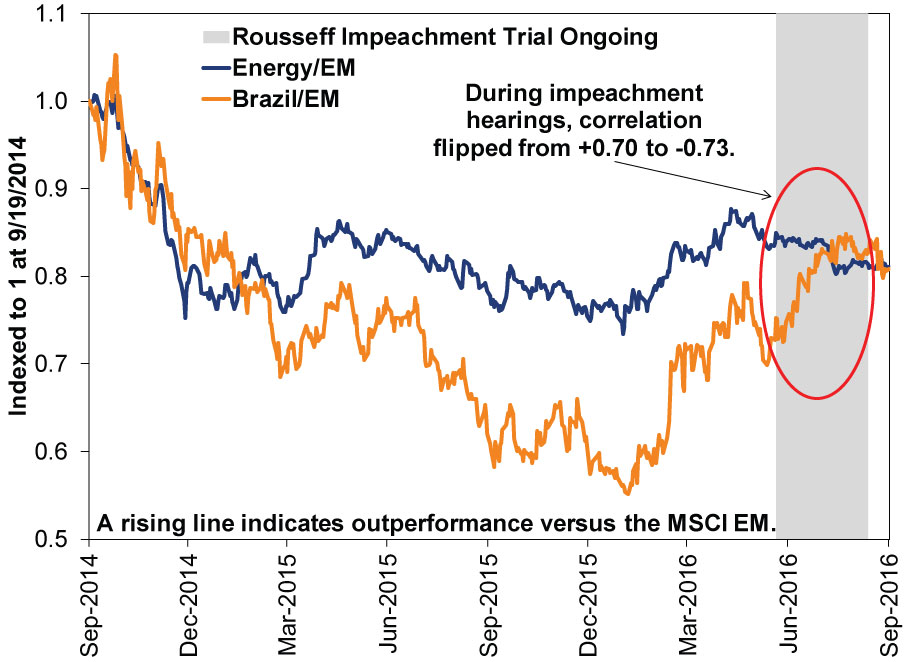

Brazil's economy and stocks were mostly ravaged by the commodity downturn. Brazil's economy relies heavily on commodity production and exports-particularly iron ore, soybeans and oil. All these have seen very weak prices in recent years, weighing on Brazil's economy and markets. This is especially true of Energy-EM Energy stocks and the MSCI Brazil's relative returns have been tightly linked until very recently. The correlation coefficient-a statistical measure of the relationship between two data series ranging from -1 (exact opposites) to 1 (move in lockstep)-was 0.70 for most of the last two years.[iv] As one would assume, when Energy stocks lagged badly due to declining oil prices, Brazil lagged right along with them. However, in January, oil prices touched their low and rallied. Energy stocks-and Brazil-rallied as well.

This is all as one might presume. It's quite unsurprising that a commodity-heavy country's relative performance would show heavy influence from one of the world's primary commodities. However, relative returns sharply diverged starting in early June. During this span, EM Energy stocks (like their developed-world counterparts) floundered rather directionlessly, underperforming broad markets. Brazilian stocks have shot higher. The correlation coefficient flipped from 0.70 to -0.73.[v] What gives?

Exhibit 1: Brazilian Relative Performance Typically Linked to EM Energy

Source: FactSet, as of 9/20/2016. MSCI Brazil, MSCI EM Energy Sector and MSCI EM Indexes, 9/19/2014 - 9/19/2016.

It seems Brazilian investors had an impeachment party. The divergence in relative performance coincides with former President Dilma Rousseff's impeachment trial, which began June 8 and ended with her being removed from office August 31. For much of the last year, investors speculated she would be removed-with many going so far as to consider the development bullish, believing a new president might be better positioned to enact economic reforms they presume would aid the economy. Perhaps reforms (like limiting government spending and reforming government retirement benefits) would help. But new President Michel Temer isn't hugely popular, and his government is already embroiled in continuing corruption investigations. Moreover, the government is fractured by scandal-reforms will be difficult to pass. To us, the recent divergence seems like excessive optimism about reforms' potential. After all, only a small part of Brazil's present predicament can be linked to something the government can materially influence. Global oil and commodities production simply isn't under Temer's purview, to the extent he has one.

Here is the big question: Whatever you think of Temer's ability to change laws, can reforms, if passed, offset Brazil's typical linkage to commodity prices? It's a key question, as commodities markets remain awash in excess supply. Hence, the Energy rally that began in early 2016 has faded since May. Whether or not Temer's government is able to meet reform expectations, Brazil seems likely to face a stiff headwind from weak commodity prices. Now, add to that the very real risk Temer's government underwhelms, and investors' impeachment party could easily bring a horrific hangover.

[i] Sorry, but aren't you required to reference the Olympic swimmer turned dancing star in any article about Brazil these days?

[ii] Source: FactSet, as of 9/21/2016. MSCI Brazil and MSCI EM Indexes with net dividends, 9/19/2014 - 1/25/2016.

[iii] Ibid. 1/25/2016 - 9/19/2016.

[iv] Ibid. Correlation shown is between the return of the MSCI Brazil Index minus MSCI Emerging Markets and the MSCI EM Energy Sector Index minus the MSCI Emerging Markets, 9/19/2014 - 6/8/2016.

[v] Ibid. Correlations shown are between the return of the MSCI Brazil Index minus MSCI Emerging Markets and the MSCI EM Energy Sector Index minus the MSCI Emerging Markets, 9/19/2014 - 6/8/2016 and 6/8/2016 - 8/31/2016.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27 -

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

-

Politics This Week in Gridlock: Europe Edition2026-03-26

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today