Personal Wealth Management / Market Analysis

Brexit: One Year Later

A review of what has come to pass after the UK voted to leave the EU a year ago.

Breaking up is hard to do. Photo by Chris Ratcliffe/Bloomberg via Getty Images.

Do you remember where you were when Britain turned its back on Europe? It was headline writers' time to shine! After "Little England Beat Great Britain" and "opened Pandora's Box," pundits reflected on the "24 Hours in Which the World Has Changed." Some said Brexit was "the biggest blow to a united Europe since the Second World War" and the Continent "may be plunged into the worse crisis in its history." Though a few outlets weren't quite so apoplectic-"Brexit won't be as bad as people think[i]"-many were freaking out over the surprising result and what it meant not just for the UK, but the world. Yet a year after Brexit, the UK is still in the EU. We know, shocker! (Kidding, of course.) With a year now behind us, the present seems like a good time to recap what has-and, perhaps more importantly, hasn't-happened.

After the vote, fear abounded. Stocks' sharp selloff drove bear market dread. The business environment suddenly looked iffy, with uncertainty allegedly icing potential mergers. Others predicted businesses would spend less and inflation would crimp consumers, rendering recession. Across the channel, EU-types feared losing a major trading partner as well as a potential domino effect if increasingly popular anti-EU political parties gained power.

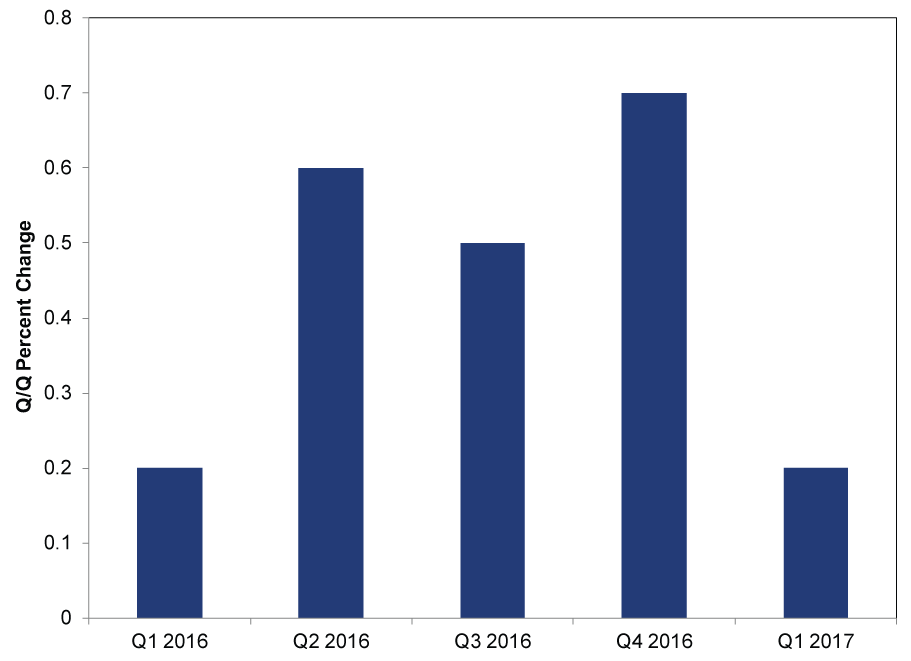

One year later, none of this has happened. The UK economy didn't contract. GDP actually sped in late 2016 before slowing down to start 2017.

Exhibit 1: UK GDP Growth, Quarter-Over-Quarter

Source: FactSet, as of 6/20/2017.

Purchasing Managers' Indexes (PMI)-gauges measuring the breadth of growth-have shown continued expansion in services and manufacturing. July 2016's sub-50 readings reflected a one-time knock to sentiment, but subsequent months prove this was a blip.

Exhibit 2: IHS/CIPS UK Composite and Services PMI Since 2016

Source: FactSet, as of 6/20/2017.

Some cite 2017's weak retail sales and rising inflation as signs Brexit's ill-effects were merely delayed. However, though the pound's post-referendum plunge contributed some to rising inflation,[ii] so did other factors, like swinging energy prices. Though core CPI (which excludes food and energy) is also running hotter, this isn't surprising given fast money supply and loan growth since last summer. Inflation is always and everywhere a monetary phenomenon, and more money coursing through the economy results in rising prices. As for consumption, while household spending notched its slowest growth rate since Q4 2014 in Q1, we aren't ready to call one quarter of data the beginning of a downturn. While retail sales remain choppy in Q2, thus far, they still exceed Q1-volatility is just obscuring the trend. Moreover, always remember stocks are a leading economic indicator. If weak consumption really signaled a UK economy on the brink of recession, it would be bizarre for the MSCI UK to be up 6.5% in GBP year-to-date.[iii] This trails the MSCI World ex. UK's 8.2%, but a rise is a rise.[iv] For those worried stocks are fine solely because the pound's post-vote plunge boosts exporters, note the FTSE 250, which tracks smaller, domestic-focused UK firms, is leading its bigger, more multinational counterpart FTSE 100, 10.4%[v] to 6.6%[vi]-evidence Brexit hasn't decimated more domestically oriented British companies.

Meanwhile, anti-EU politicians whiffed at the ballot box. In December, Austrians chose the pro-EU independent candidate over the far-right Freedom Party's Norbert Hofer. Geert Wilders and his Party for Freedom failed to win Dutch parliamentary elections in March. France's Marine Le Pen and her far-right Front National party flopped in both the presidential and parliamentary elections. Other anti-EU parties-like Germany's AfD and Italy's Five Star Movement-are flagging in the polls and regional elections. So much for the Brexit domino effect.

In our view, this all shows why the vote wasn't reason for long-term investors to alter a carefully constructed financial plan. Most of the near-term impact was sociological, not market-related, because markets ultimately care most about the final arrangement, which was always going to take years to hash out. It took nine months for the UK to formally start the withdrawal process and open a two-year negotiation window. Reaching (or not reaching) an exit agreement might take even longer, depending on how talks and politics evolve. This gives markets plenty of time to price in and digest the actual changes to the UK's relationship with the EU-not just speculation about what might happen. Even today, after PM Theresa May announced her intent to leave the EU's customs union, we know next to nothing-leaving the customs union is basically an administrative step for the UK to make its own trade deals to become a "great global trading nation." Whether this constitutes a "hard" or "soft" Brexit is a matter of semantics. Markets will focus on the final draft of the deal, and how that is ultimately structured is unknowable now.

So while a lot has seemingly changed over the past year, June 23, 2017 looks pretty similar to June 23, 2016: The UK is still part of the EU, the government is gridlocked and the economy's robust services sector is still chugging along. Markets focus mostly on the next 12-18 months, and these fundamentals don't look likely to deteriorate for the foreseeable future. We will continue monitoring the negotiations and developments, but with a year now past, the Brexit episode demonstrates the importance of coolly analyzing major developments and staying disciplined in the face of volatile, uncertain times.

[i] Cheers to the Aussies for always keeping it real.

[ii] We find it odd that the media misses the obvious about the pound. Brexit itself isn't "bad" for currency. Most folks knew Brexit meant a likely rate cut, which, all else equal, drops demand for the pound. Since Brexit, the BoE has indeed cut while the US Fed has hiked three times. Money usually flows to the highest-yielding asset, so the pound's fall wasn't shocking.

[iii] Source: FactSet, as of 6/22/2017. MSCI UK, gross dividend returns in GBP, from 12/30/2016 - 6/21/2017. For comparison's sake, in USD, the MSCI UK (net dividends) returned 9.1%-this is what a US investor would get.

[iv] Ibid. MSCI World ex. UK net dividend returns in GBP, from 12/30/2016 - 6/21/2017. We are sharing this in GBP to compare like with like. In USD, the MSCI World ex. UK (net dividends) returned 10.9%.

[v] Source: FactSet, as of 6/22/2017. FTSE 250 Total Return, gross dividend returns in GBP, from 12/30/2016 - 6/21/2017. In USD and net dividends, the index returned 13.5%.

[vi] Source: FactSet, as of 6/22/2017. FTSE 100 Total Return, gross dividend returns in GBP, from 12/30/2016 - 6/21/2017. In USD and net dividends, the index returned 9.6%.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis CPI Sheds Light on Britain’s Price ‘Cap’ Conundrum2026-05-20

-

Market Analysis The Investment Implications of Record-Low Consumer Sentiment2026-05-19

-

Market Analysis More Positive Surprise in Japan’s Q1 GDP2026-05-19

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—May 11 - May 152026-05-18

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today