Personal Wealth Management / Market Analysis

Buried Growth

Contrary to fears otherwise, the global economy is growing just fine.

Well that didn't take long: Three trading sessions into 2015, some were ready to surmise, "The good times are over." Global bond yields tanked as folks allegedly headed for safe havens. And "from Japan to Germany to Australia," investors are wrestling with the risk of "global deflation." Fears of a weak world are back! But in our view, the latest economic data don't much support these concerns-the world is growing fine.

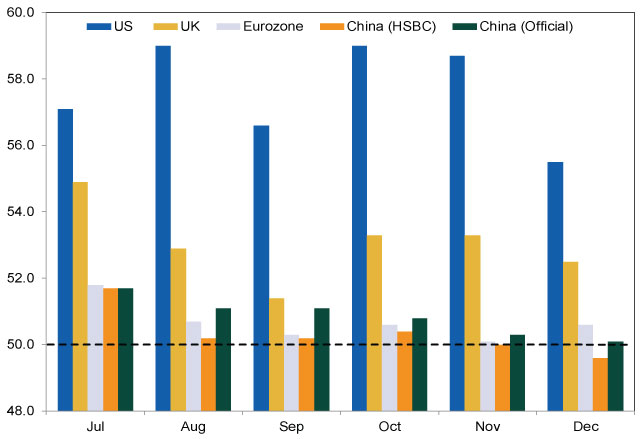

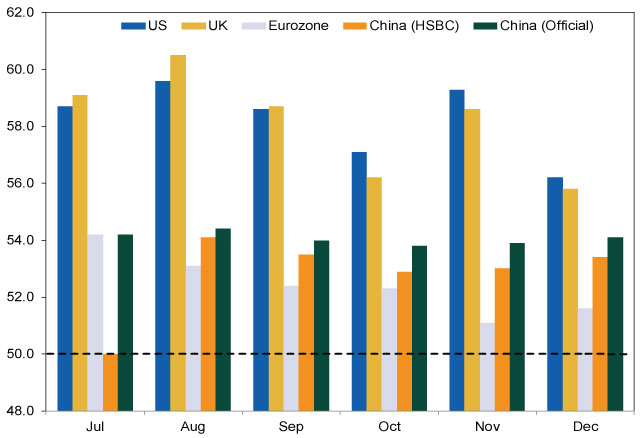

Consider the most recent purchasing managers' indexes (PMI)-monthly surveys that ask thousands of businesses if they saw business activity grow. The reading is the percentage of firms who said, "Yep!" Hence, if readings top 50, more than half of firms probably grew. December PMIs suggest most companies globally said, "yep" (or some similar thing[i]). ISM's US Services and Manufacturing PMIs hit 56.2 and 55.5, respectively, while Markit's UK Services and Manufacturing PMIs closed at a respective 55.8 and 52.5. The much-maligned eurozone's composite PMI hit 51.4, and German, French and Spanish Services PMIs grew too (52.1, 50.6 and 54.3, respectively). The one laggard of the big four: Italy, at 49.4. Contractionary, but only slightly.

Growth wasn't exclusive to the developed world. Though HSBC's China Manufacturing PMI contracted slightly at 49.6, its Services PMI rose to 53.4. (Services firms are the biggest slice of China's economy.) HSBC's PMIs cover only smaller, private firms. The country's official PMIs span small private companies and huge state-owned enterprises, and both were expansionary (Services at 54.1, Manufacturing 50.1). HSBC's India composite PMI rose to 52.9. Oh and to put a nice bow on it all, JP Morgan's Global Manufacturing & Services PMI-which includes 32 countries-hit 52.3.

While one month's data say little, December's PMIs aren't anomalies.

Exhibit 1: 2014 Manufacturing PMIs for the US, UK, Eurozone and China

Source: St. Louis Federal Reserve, Bloomberg, National Bureau of Statistics of China. As of 1/7/2015. 50 is the dividing line at which more or less than half of survey respondents reported growth.

Exhibit 2: 2014 Services PMIs for the US, UK, Eurozone and China

Source: St. Louis Federal Reserve, Bloomberg, National Bureau of Statistics of China. As of 1/7/2015. 50 is the dividing line at which more or less than half of survey respondents reported growth.

Now, that all makes it seem fairly obvious growth continued, but you might struggle to come to that conclusion in reading major media coverage, which overfocused on the fact some PMIs slowed. Consider: "UK Services Grow Least in 19 Months as Economy Loses Steam". Sounds troublesome, especially considering Services is about 80% of UK GDP. Yet, again, the sector expanded-a 55.8 reading is "slower" only relative to the recent past. And before jumping on the "lowest level in 19 months," this arbitrary factoid says more about UK Services' strength over the past two years than it does current weakness. The world wasn't in the throes of a global recession in May 2013-it was expanding, with the UK at the forefront when broader, output-oriented measures like GDP are considered. It was also smack in the middle of a great big bull market year.

Negative interpretations aren't limited to Britain. Take a peek across the English Channel at the eurozone, where the media claimed December's PMI showed the "Euro Zone Economy Ended 2014 in Poor Shape." Or lamented that, "Eurozone Services PMI Disappoints in December." Manufacturing, we are informed, was "near stagnant" in December. Yet December's composite PMI rose from November's 51.1, and three of the region's four biggest economies exceeded 50-indicating a majority of firms grew. These factoids dispute the widely accepted notion a eurozone deflationary depression is underway.

Our advice: Keep it simple and don't overthink any of this. A temporary PMI slowdown (or pop) doesn't really say much-monthly readings always vary, and PMIs are imperfect. They're surveys. The frequency of "yep" doesn't tell you the magnitude of "yep." If 49.4% of firms grow, but they grow a lot, PMI doesn't rise but overall output still could. Occasional PMI slowdowns aren't warning lights. What matters most is that December's readings are broadly consistent with the longer-term trends-expansionary but choppy-which accompanied actual growth. Most are aware of America's strength (Q3 GDP grew at a 5.0% seasonally adjusted annual rate), and perhaps Britain's too (Q3 GDP grew 3.0% annualized[ii]). But few notice the eurozone's six consecutive quarters of (uneven) growth. Or that China's 7%-ish y/y growth adds more activity to the global economy than when a smaller China grew double-digits in the mid-2000s. Or that many Emerging Markets outside China are largely growing too. And that forward-looking economic indicators like the Conference Board's Leading Economic Indexes suggest continued economic growth in much of the world.

To be sure, there are pockets of weakness in the world, like Russia and Japan. But that is a constant. The likelihood a heterogeneous world grows homogenously is pretty much zero. On balance, the global economy is chugging along and growth doesn't seem likely to come screeching to a halt.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] Yesindeedy, yepidoodle, ja, sí, hai, oui, yes siree bob-you get the drift.

[ii] Source: FactSet, UK Q3 2014 real GDP growth, annualized.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

-

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27 -

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today