Personal Wealth Management / Politics

Canadians Pick the Status Quo

Monday’s election brought precious little change, extending gridlock.

Editors’ Note: Our political commentary is intentionally nonpartisan. We favor no politician nor any political party and assesses political developments for their potential economic and market impact.

Well that was anticlimactic. Five weeks after Canadian Prime Minister Justin Trudeau dissolved Parliament and called a snap election in hopes of his Liberal Party winning an outright majority, the results are in: The Liberals remain in power, but they still have a minority government and will have to rely on help—chiefly from the leftist New Democratic Party (NDP)—to get anything done. Moreover, three of Trudeau’s cabinet ministers lost their re-election bids, and many onlookers are grousing about the indecisive campaign, potentially leaving the government with less political capital than they had going in. Most coverage is focusing on the political optics and Canadians’ overall frustration with being asked to vote during the middle of the Delta variant’s surge. For stocks, that is all sociology and beside the point—what matters for returns to an extent, in our view, is that political uncertainty has eased and gridlock persists for the foreseeable future.

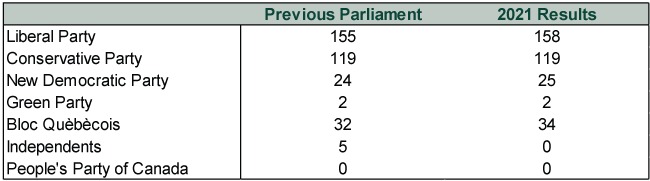

Exhibit 1 shows the latest tally of the results and how they compare to the last parliament. With 98% of votes counted, the Liberals have gained just three seats in the House of Commons, while the Conservatives have no net change. The real losers, we guess, were independents, who had five seats in the previous Parliament and have none now. Close on their heels are Green Party leader Annamie Paul, who came in fourth in her race as her party lost support nationally, and the People’s Party of Canada—a right-leaning party started by former Conservatives frustrated with party leadership—which won zero seats.

Exhibit 1: Canadian Election Results

Source: Elections Canada, as of 9/21/2021. One seat was open in the previous parliament.

Stocks don’t care about personalities—they care about policies and the likelihood of major changes to property rights and other issues that could affect businesses’ ability to make long-term investments and plan for risks. Like the major political parties in other developed nations, Canada’s Liberal and Conservative parties are equally capable of ratcheting up legislative risk. So when Trudeau called the snap election while his party had a six-point lead over the Conservatives, according to the CBC News Poll Tracker, the risk for stocks was a government—any government—winning an outright majority and reducing or ending the gridlock that helped keep legislative risk to Canadian stocks’ low since 2019.

This is the status quo this week’s election extended. It complicates the path forward for many divisive measures, potentially forcing the government to water them down. Perhaps, perhaps, the Liberals can get something like the mooted bank profit surtax approved with the help of the NDP. But that remains to be seen, considering the NDP favors a broader raft of tax hikes than the Liberals.

Of course, politics are only one driver. The election does ease the uncertainty that loomed over Canadian stocks this summer and the outcome may provide some relief to markets. But we think sector and stylistic factors probably matter more—in this case, Canada’s strong tilt toward Energy, Financials and value stocks in general. Canada outperformed the world handily in 2021’s first half, as Energy stocks globally went on a tear, but it has underperformed alongside Energy since June, erasing most of its year-to-date advantage. That seems to us like a decent microcosm of what to expect on the relative return front as this bull market progresses: Canada’s fortunes ebbing and flowing with Energy and value stocks, while Tech and Tech-like companies (of which Canada has relatively few) likely continue to lead overall.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Kevin Warsh and the Magical Delete Button2026-06-17

-

Market Analysis The Politics and Practicalities of the Social Security Trust Fund2026-06-16

-

Market Analysis Gold Fails the Safe Haven Test Again2026-06-16

-

Expert Commentary Ken Fisher on Crypto, Inflation, AI Bubble and Annuities

2026-06-16

2026-06-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today