Personal Wealth Management / Market Analysis

CAPE (Nothing to) Fear

Valuations are telling only at extremes; we aren't there yet.

Well, that didn't take long: Mere months (and only 3.7%)[i] after the S&P 500 finally broke out of a lengthy flat stretch, pundits warn stocks have come too far, too fast, and high P/E ratios signal an overvalued market and unrealistic hopes for 2017 earnings. Many point to the Cyclically Adjusted P/E Ratio (CAPE, or Shiller P/E), which is currently at levels last seen before major crashes, as evidence trouble lurks. Yet, as is typical when valuations hit the headlines, there are several flaws in this reasoning. Some valuations can signal sentiment when they're at extremes-which they aren't today-but overall, they are poor predictors of stock returns. Nothing about today's valuations suggests stocks are overvalued.

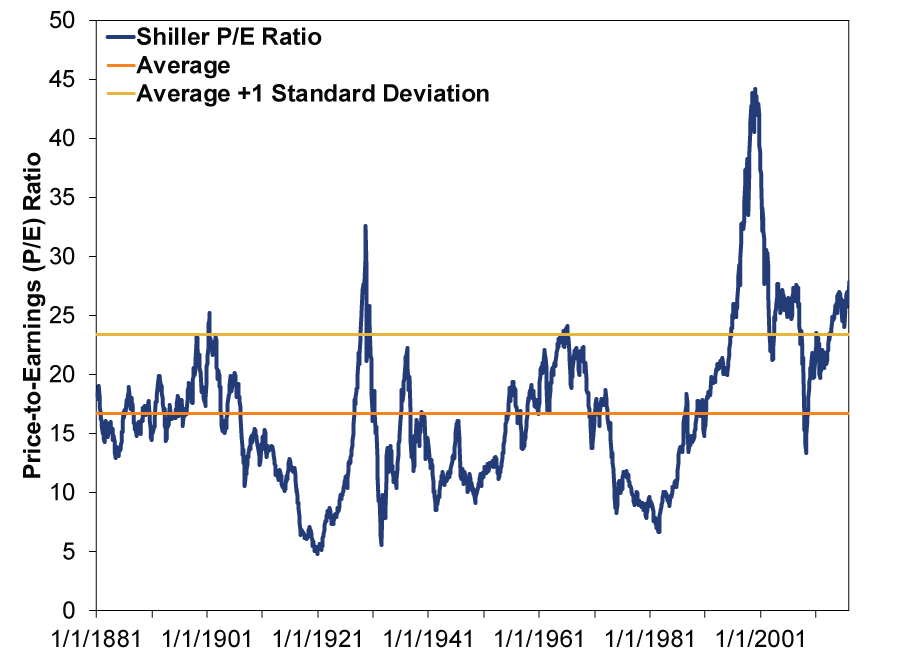

Yes, the CAPE is the highest it has been since 2007, 2000 and 1929, when major bear markets began. But coincidence doesn't make the CAPE a valid timing tool or predictive in any way, shape or form. Conceptually, the CAPE has problems. Its denominator is the 10-year average of bizarrely inflation-adjusted[ii] earnings. That is supposed to adjust for economic cycles, but it doesn't tell you anything about stocks' future earnings streams, which is what you're buying. Never mind the fact it is really, really odd to leave the economic cycle out of your projection for stocks. Moreover, the CAPE doesn't work. Exhibit 1 shows the CAPE, its average (orange line) since 1881 and one standard deviation (yellow line) above the average, which just means 16% of observations lie above it. So although the current reading is among 16% of the most expensive "outliers," it has been there pretty darn frequently in recent years.

Exhibit 1: No CAPEs!

Source: Multpl.com, monthly S&P 500 Shiller P/E Ratios, 1/1/1881 - 1/3/2017.

It isn't as though stocks historically hit the current level and fell off a cliff. Price returns for the S&P 500 average 8.7% annualized when the CAPE is more than one standard deviation above its average.[iii] For the series as a whole since 1881? 4.3%.[iv] the CAPE can look right sometimes, but a broken clock is right twice a day. The vast majority of the time, it's wrong, and following it is detrimental to investors' performance.

Sensibly Constructed Valuation Measures Aren't That Useful Either

Even using (conceptually sound) forward earnings P/Es,[v] which are decent indicators of sentiment, high valuations are no impediment to higher stock prices if economic fundamentals are sound and earnings are trending higher. A high P/E could just as well signal rising investor confidence, a regular feature of maturing bull markets. Indeed, high P/Es often precede positive return years.

It's normal for valuations to expand as bull markets mature and investors gain confidence. We haven't really seen that late-bull multiple expansion yet-and didn't in 2002 - 2007's bull, which died prematurely, walloped by the implementation of FAS 157 and the government's haphazard crisis response.

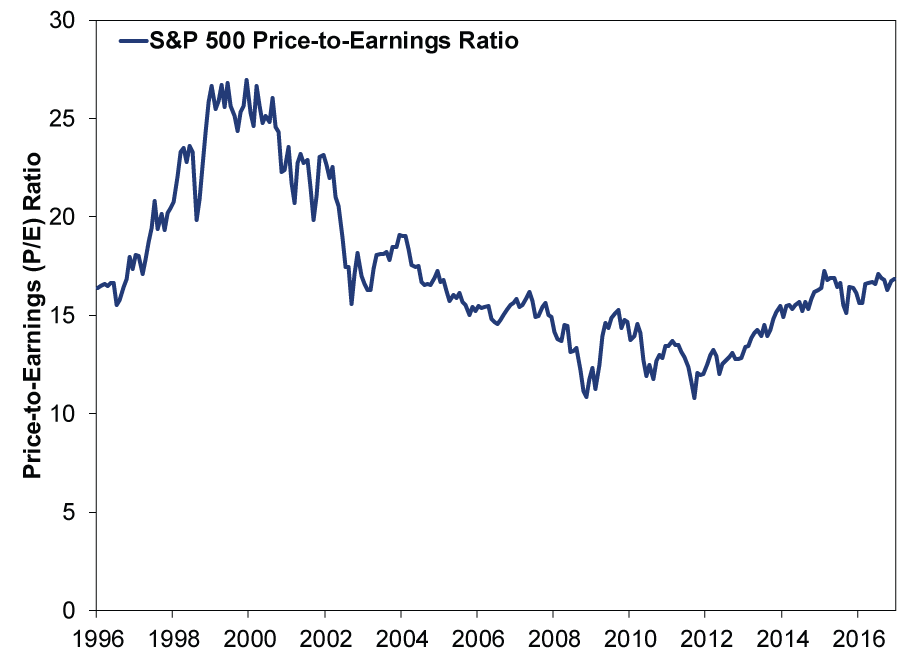

Exhibit 2: P/Es Flat Since 2014

Source: FactSet, as of 1/5/2017.

The S&P 500's current forward P/E is 17.1.[vi] That may be slightly above average, but slightly above average doesn't really matter-mean reversion isn't a force in capital markets. Nor is there one magic P/E level that signals a peaking bull. Multiples got to 25 as the Tech bubble peaked in 2000, while other peaks featured lower P/Es. Levels aren't really telling. It's more a question of whether P/Es suddenly accelerate and spike. There is no spike today. Actually, the S&P 500's forward P/E has been range bound for about two years-consistent with sentiment just sort of grinding along (see Exhibit 2). With folks now slowly becoming more optimistic, it wouldn't shock us if P/Es expanded over the foreseeable future.

Stocks don't care about P/E ratios or any other valuation metric alone. Sentiment matters, but the question is always whether sentiment is detached from reality. To us, growing confidence seems entirely consistent with a growing US and global economy, improving corporate earnings and low legislative risk (thanks to gridlock in the US and most of Western Europe).

Too Far? Not So Fast

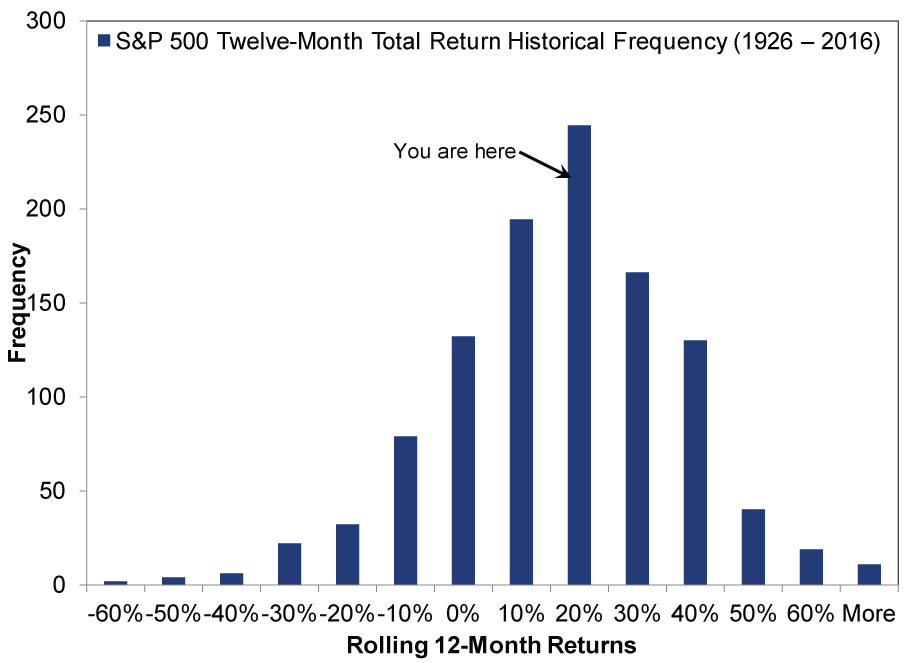

Hence, we wouldn't get too worried over the latest string of all-time highs either. Nor is the latest rally as monstrous as some recent commentary might lead you to believe. Total return for the S&P 500 was 12.0% in 2016, well within history's bell curve (see Exhibit 3).

Exhibit 3: Current Bull Market Defines Normal

Source: Global Financial Data, Inc., S&P 500 total return, 12/31/1925 - 12/31/2016.

Some pundits suggest stocks have risen too fast on expectations Trump will deregulate, cut taxes and spend oodles on infrastructure. If his campaign promises aren't fulfilled, they posit, markets will correct. We take a different view. For one, 2016's results nearly match the average election year since 1928. And that Trump Rally the media is selling amounted to a 4.64% S&P 500 price gain between Election Day and the year's end, 37 trading days.[vii] Since 1928, 26.1% of rolling 37-day periods have exceeded 4.64%.[viii] Those periods include three stretches last year (post-correction low, post-Brexit and post-election). Only one year-long stretch since 1928 lacked a +4.64% 37 day period: 1993. Most years have multiple stretches, like 2016. The Trump Rally is very ordinary.[ix]

We see ample non-Trump explanations for stocks' climb. In our view, markets have rallied the past two months because of falling uncertainty,[x] married with brightening sentiment and strong pre-existing fundamentals. What's more, earnings are rising independently of Trump, and starting to accelerate as Energy's unfavorable comparisons fall out of the calculation. While S&P 500 calendar year earnings are expected to rise only 0.2% in 2016 (with Q4 earnings yet to be reported), excluding Energy that estimate rises to 3.7%.[xi] For 2017, analysts currently expect 11.5% earnings growth (8.2% ex. Energy).[xii] Sure, take forecasts with a grain of salt, but if the direction is anywhere near right, stocks should have a good year no matter what pundits say P/Es signal.

So rather than anticipate weakness when Trump's plans aren't as yuuuuuuuuuuuge as promised, we expect the bull market to continue in part because gridlock quells the fears those pundits overlook, like trade barriers and drug price caps. P/Es are most telling when sentiment is at extremes, and even then, they shouldn't be the sole evidence for a bearish stance. Other sentiment gauges and economic reality are important, too. Right now, if "high P/E" warnings and Trump-phobia are any indication, economic fundamentals remain underappreciated.

[i] From the S&P 500's 2190 summer price high 8/15/2016, breakthrough 11/21/2016 and 2271 close 1/4/2017.

[ii] Like using a continually and variably shrinking yardstick-nominal dollars-to price stocks and then comparing that with earnings priced by a normal non-shrinking yardstick-inflation-adjusted dollars. Sure, they're both measured in "dollars" but you need to know the time of measurement and the inflation rate between the times to make the correct conversion for proper comparison.

[iii] Source: Multpl.com, S&P 500 Prices, 1/1/1881 - 1/3/2017. Price returns used instead of total returns due to the longer dataset.

[iv] FOR THE RECORD: We do not put a lot of stock (heh heh) in returns from 1881 or really any point before 1926. However, the founders of the CAPE (Shiller and the usually forgotten Campbell) went way back. So we did here.

[v] Typically, analyst consensus estimates of 12-month forward earnings.

[vi] Source: FactSet, as of 1/5/2017. S&P 500 12-month forward P/E on 1/4/2017.

[vii] Source: Global Financial Data, Inc., as of 1/5/2017.

[viii] Ibid.

[ix] It is not yuge.

[x] If Clinton had won, markets may very well have been up even more, but we'll never know.

[xi] Source: FactSet Earnings Insight Report for week ending 12/30/2016, as of 01/05/2017.

[xii] Ibid.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today